Propylene Oxide via HPPO Process Market Strategic Outlook (2026-2034): Green Chemistry Innovation Accelerates Sustainable Polyurethane Feedstock Demand

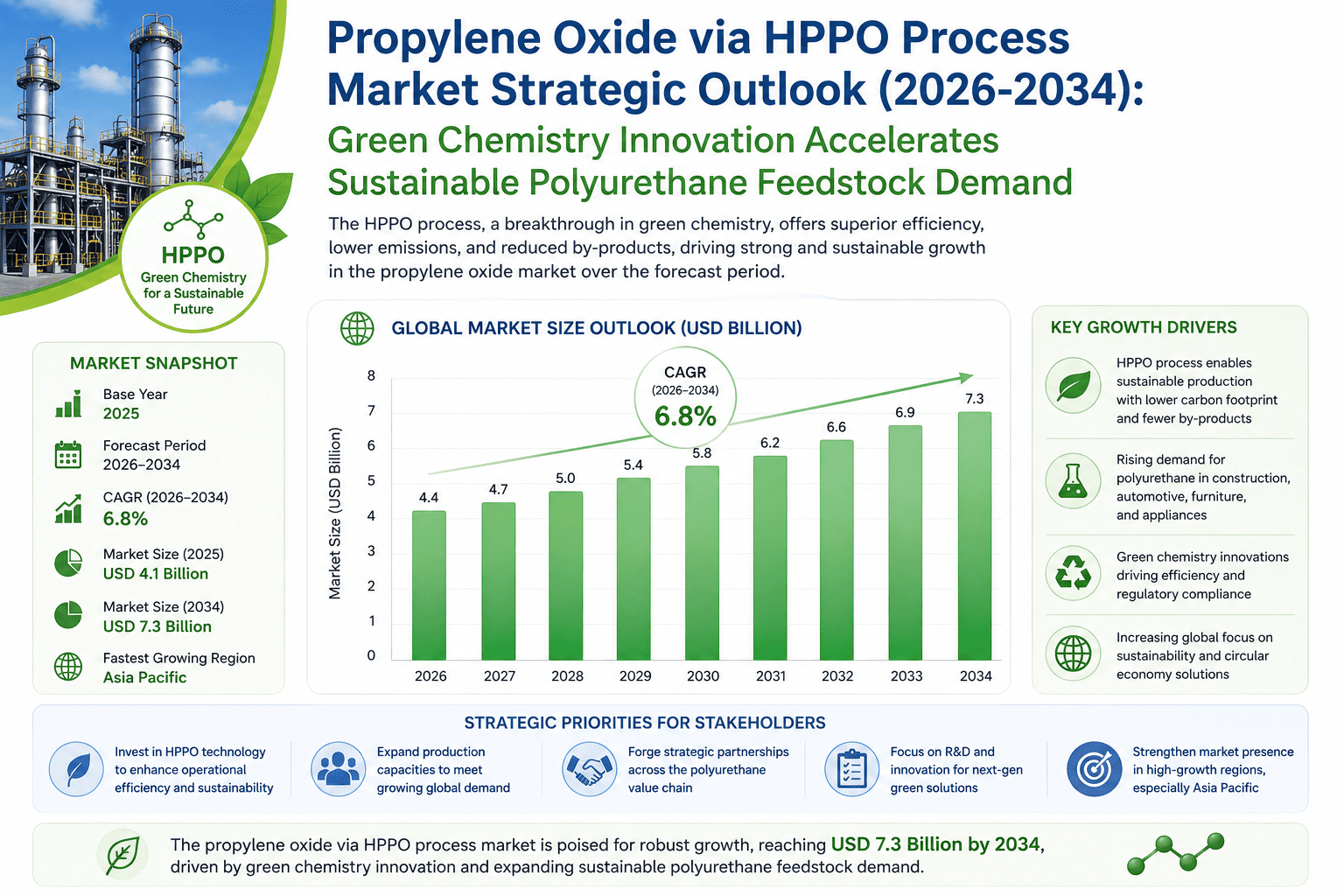

Global Propylene Oxide (PO) via Hydrogen Peroxide (HPPO) Process Market size was valued at USD 6.84 billion in 2025. The market is projected to grow from USD 7.21 billion in 2026 to USD 12.47 billion by 2034, exhibiting a remarkable CAGR of 6.3% during the forecast period.

HPPO process is an advanced, cleaner route for manufacturing propylene oxide, utilizing hydrogen peroxide and propylene as primary feedstocks in the presence of a titanium silicalite (TS-1) catalyst. Unlike conventional chlorohydrin or styrene monomer co-production methods, the HPPO process generates water as its primary by-product, significantly reducing waste streams and environmental impact. Propylene oxide produced via this route serves as a critical intermediate chemical, widely used in the production of polyether polyols, propylene glycols, and propylene glycol ethers, which in turn find extensive application across polyurethane foams, coatings, surfactants, and pharmaceuticals. The market is gaining considerable momentum, driven by tightening environmental regulations worldwide and a broader industry shift toward sustainable and green chemistry production pathways. Furthermore, the robust demand for polyurethane foam from the construction, automotive, and furniture sectors continues to underpin consumption of propylene oxide at a global scale. Key industry participants such as BASF SE, Evonik Industries AG, and Dow Inc. have been at the forefront of HPPO technology development and commercial-scale deployment, reinforcing the technology's competitive positioning within the broader propylene oxide manufacturing landscape.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308788/propylene-oxide-via-hydrogen-peroxide-process-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Rising Global Demand for Polyurethane Foam and Downstream PO Applications: The global propylene oxide market has witnessed sustained demand growth, driven primarily by the polyurethane sector, which accounts for the majority of PO consumption worldwide. Polyurethane foams—used extensively in furniture, automotive seating, construction insulation, and packaging—rely on PO-derived polyols as a key feedstock. As urbanization accelerates across Asia-Pacific and construction activity expands in emerging economies, the downstream pull for PO continues to intensify. The HPPO process, which produces PO using hydrogen peroxide and a titanium silicalite catalyst without generating co-products such as styrene or chlorinated waste streams, has gained strategic importance as producers seek cleaner and more flexible production routes. The global polyurethane market was valued at approximately USD 74 billion in 2025, with PO as a critical upstream feedstock maintaining strong co-movement in demand trajectories.

-

Environmental and Regulatory Advantages Over Conventional PO Production Routes: Compared to the chlorohydrin process and the PO/SM (styrene monomer) co-production route, the HPPO process generates significantly less wastewater and eliminates chlorinated byproducts, making it increasingly attractive in jurisdictions tightening industrial effluent regulations. The process generates water as its primary byproduct, dramatically reducing the environmental footprint per tonne of PO produced. In the European Union, where REACH regulations and industrial emissions directives are enforced rigorously, several major chemical producers have favored HPPO-based capacity expansions. This regulatory tailwind has accelerated technology licensing and greenfield project activity, particularly among producers seeking to align with long-term sustainability commitments. The HPPO process consumes approximately 35% less energy and generates up to 80% less wastewater compared to the chlorohydrin route, making it one of the most environmentally favorable PO production technologies currently deployed at commercial scale.

-

Accelerating Electric Vehicle Production Driving Polyol and PO Demand: The acceleration of electric vehicle (EV) production globally is reshaping PO demand, as EV platforms integrate lightweight polyurethane components for battery enclosures and structural foam applications. Global EV sales surpassed 17 million units in 2024, a trend expected to further intensify polyol and PO consumption through 2034. Automotive interior components—including seat cushions, headliners, dashboards, and door panels—rely heavily on PO-derived flexible foams and polyols. As the automotive sector transitions toward lighter-weight, energy-efficient materials to extend EV range, HPPO-derived PO is positioned as a preferred upstream feedstock given its cleaner production profile and consistent quality attributes that downstream polyol manufacturers increasingly specify in their procurement criteria.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308788/propylene-oxide-via-hydrogen-peroxide-process-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

High Capital Intensity and Complexity of HPPO Process Integration: Despite its environmental advantages, the HPPO process requires substantial upfront capital investment. The need for integrated hydrogen peroxide production or reliable long-term supply agreements, combined with the specialized titanium silicalite (TS-1) catalyst systems and high-pressure reactor configurations, places the HPPO route beyond the financial and technical reach of smaller or regional chemical producers. Project costs for world-scale HPPO plants have historically ranged into the hundreds of millions of dollars, creating a significant barrier to entry and limiting the competitive landscape to a handful of large integrated chemical companies with access to technology licenses from developers such as BASF-Dow and Evonik-Uhde (now thyssenkrupp Uhde).

-

Competition from Established PO/SM and Chlorohydrin Production Infrastructure: A substantial portion of global PO capacity remains tied to the PO/SM co-production route, particularly in the United States and Europe, where large integrated petrochemical complexes have been operating for decades with capital costs largely amortized. Producers operating these facilities benefit from the additional revenue stream generated by styrene monomer, which can subsidize PO production economics even during periods of PO price softness. This economic structure makes it difficult for standalone HPPO-based producers to consistently undercut incumbent pricing, particularly when styrene markets are strong. The entrenched infrastructure and long asset lifetimes of existing PO/SM plants represent a meaningful structural restraint on the pace of HPPO market share gains.

Critical Market Challenges Requiring Innovation

The transition toward large-scale HPPO adoption presents its own set of operational and economic challenges that the industry continues to navigate. The TS-1 catalyst used in the HPPO process is subject to deactivation over time, requiring periodic regeneration or replacement cycles that introduce operational downtime and add to lifecycle costs. Managing catalyst performance at commercial scale demands sophisticated process control capabilities and operator expertise that may not be uniformly available across all geographies. In markets where technical workforce depth is limited, sustaining optimal HPPO plant performance can be challenging, and suboptimal catalyst management can erode the process efficiency advantages that justify the higher initial capital commitment.

Furthermore, the HPPO process is directly exposed to hydrogen peroxide price fluctuations, which are in turn influenced by anthraquinone oxidation (AO) process economics, energy prices, and regional supply-demand imbalances. During periods of tight H₂O₂ supply or energy cost spikes, HPPO producers face margin compression that can make the route less competitive relative to PO/SM co-production, where the economics are partially buffered by styrene monomer revenues. Producers without backward integration into H₂O₂ supply are particularly vulnerable to these dynamics, underscoring the strategic importance of co-located hydrogen peroxide and propylene oxide production in optimizing the overall economics of the HPPO route.

Vast Market Opportunities on the Horizon

-

Capacity Expansion in Asia-Pacific Driven by Polyurethane Demand Growth: Asia-Pacific, and China in particular, represents the most dynamic growth frontier for HPPO-based PO production. China's domestic polyurethane industry—serving construction, appliance, automotive, and footwear sectors—has driven aggressive investment in PO capacity, and the HPPO process has been selected for several significant projects given its reduced environmental compliance burden relative to the chlorohydrin route. As Chinese environmental enforcement intensifies under ongoing industrial pollution control campaigns, HPPO's cleaner process profile positions it favorably for future project approvals. Additional capacity additions are anticipated in South Korea, India, and Southeast Asia as regional polyurethane consumption continues to outpace legacy production capacity.

-

Integration with Green Hydrogen Peroxide and Sustainability-Linked Value Chains: The emergence of green hydrogen and renewable-powered hydrogen peroxide production presents a long-term opportunity to further reduce the carbon footprint of HPPO-derived PO. Chemical producers pursuing Scope 3 emissions reductions and sustainability-linked financing are increasingly evaluating the potential to source H₂O₂ from electrolysis-based or renewable-energy-driven AO processes. While commercial-scale green H₂O₂ supply chains remain nascent, early-mover investments in this space could enable HPPO producers to differentiate their PO as a low-carbon feedstock for polyurethane and propylene glycol manufacturers, unlocking premium pricing potential and alignment with the sustainability procurement criteria increasingly applied by major consumer goods and automotive OEM customers.

-

Propylene Glycol Specialty Applications Creating High-Margin Growth Avenues: Propylene glycol (PG), a key PO derivative, serves pharmaceutical, food-grade, cosmetics, and de-icing fluid markets—all of which carry premium pricing and stringent purity requirements that favor HPPO-route PO due to its lower impurity profile. Demand for USP-grade propylene glycol is expanding, particularly in nutraceuticals and personal care, where formulation cleanliness is a regulatory and commercial priority. These low-volume but high-margin specialty derivative applications enhance overall market value and provide demand resilience even during commodity cycle downturns, making them an increasingly important growth avenue for HPPO producers seeking to diversify beyond standard polyether polyol feedstock markets.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Liquid Propylene Oxide, Purified/High-Purity Propylene Oxide, and Industrial Grade Propylene Oxide. High-Purity Propylene Oxide commands a dominant position within this segment, driven by the inherent cleanliness and selectivity of the HPPO process, which produces minimal chlorinated or sulfonated by-products compared to conventional chlorohydrin or styrene monomer co-production routes. This purity advantage makes HPPO-derived propylene oxide particularly attractive for downstream manufacturers who require consistent feedstock quality. Industrial grade variants continue to serve large-volume commodity applications where specification flexibility is tolerated, while liquid-phase delivery remains the predominant commercial form given propylene oxide's physical characteristics and established logistics infrastructure across major chemical-producing regions.

By Application:

Application segments include Polyether Polyols, Propylene Glycols, Propylene Glycol Ethers, and Others. The Polyether Polyols segment currently dominates, underpinned by the expansive and continuously growing global polyurethane foam industry. HPPO-derived PO is particularly favored in this application owing to the absence of co-products that could introduce impurities into the polyol synthesis chain, ensuring superior and consistent foam performance in furniture, automotive seating, and insulation applications. Propylene glycols constitute another high-value application, finding broad use in food-grade, pharmaceutical, and personal care formulations where the lower contamination profile of HPPO-origin PO provides a meaningful quality assurance advantage. Propylene glycol ethers further serve as critical solvents in paints, coatings, and cleaning products, while other niche applications continue to emerge as manufacturers explore the versatility of propylene oxide across specialty chemical synthesis.

By End-User Industry:

The end-user landscape includes Polyurethane Manufacturers, Pharmaceutical and Personal Care Industry, and Automotive and Construction sectors. Polyurethane Manufacturers are the dominant end-user base for propylene oxide across global markets, and their preference for HPPO-process material continues to strengthen as sustainability commitments and product quality benchmarks rise throughout the value chain. The pharmaceutical and personal care industry represents a high-growth and premium end-user segment due to the strict purity and traceability standards governing raw materials, where the clean production profile of HPPO technology offers a clear competitive advantage. Meanwhile, automotive and construction sectors drive considerable volume demand through their extensive use of polyurethane foams, coatings, sealants, and adhesives, with both industries undergoing significant transitions toward lighter-weight, energy-efficient, and sustainably sourced materials.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308788/propylene-oxide-via-hydrogen-peroxide-process-market

Competitive Landscape:

The global Propylene Oxide via Hydrogen Peroxide (HPPO) process market is characterized by a high degree of technological concentration, with a small number of large integrated chemical manufacturers dominating commercial-scale production. BASF SE and Evonik Industries AG jointly developed and commercialized one of the first large-scale HPPO plants in Antwerp, Belgium, in 2008, in collaboration with Dow Chemical (now Dow Inc.), establishing the process as a viable industrial route at world scale. Separately, Wanhua Chemical Group and Huntsman Corporation co-developed and operated an HPPO-based PO facility in China, further validating the technology's scalability. These leading players benefit from proprietary catalyst technology, integrated hydrogen peroxide supply chains, and substantial capital investment that create significant barriers to entry. The HPPO process is distinguished from conventional chlorohydrin and co-oxidation routes by its cleaner production profile, generating water as its primary by-product, which has driven investment from major producers seeking environmentally sustainable manufacturing pathways.

Beyond the pioneering first movers, a second tier of chemical producers has entered or expanded in the HPPO-based PO space, particularly in Asia-Pacific, where demand for polyurethane intermediates continues to grow rapidly. Wanhua Chemical has significantly scaled its HPPO capacity domestically and remains one of the most aggressive investors in this technology. SKC Co., Ltd. of South Korea has also operated HPPO-based PO production, leveraging a joint venture structure. Additionally, Sinopec has pursued HPPO technology development as part of China's broader push to modernize PO production with lower environmental impact. The competitive landscape continues to evolve as regional producers in China and South Korea seek licensing arrangements or indigenous process development to reduce reliance on imported technology, potentially reshaping the global market structure over the medium term. The competitive strategy across the industry is overwhelmingly focused on catalyst optimization, hydrogen peroxide supply chain integration, and forming strategic partnerships with downstream end-users to secure long-term offtake agreements.

List of Key Propylene Oxide (HPPO Process) Companies Profiled:

-

BASF SE (Germany)

-

Dow Inc. (United States)

-

Evonik Industries AG (Germany)

-

Wanhua Chemical Group Co., Ltd. (China)

-

Huntsman Corporation (United States)

-

SKC Co., Ltd. (South Korea)

-

China Petrochemical Corporation (Sinopec) (China)

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Stands as the dominant region in the Propylene Oxide via HPPO Process market, driven by its expansive chemical manufacturing base, rapidly growing end-use industries, and strong government support for cleaner production technologies. China, in particular, has aggressively pursued the HPPO route as part of its broader strategy to reduce environmental impact in chemical production, given the process's lower co-product generation compared to conventional chlorohydrin and styrene monomer/propylene oxide (SMPO) methods. South Korea and Japan contribute through advanced process engineering capabilities and technology licensing partnerships. Growing investments in petrochemical infrastructure across Southeast Asian economies such as Thailand and Malaysia are further strengthening the region's market position. The combination of cost competitiveness, scale of production, and evolving regulatory frameworks favoring greener chemistry continues to cement Asia-Pacific's leading role in this market.

-

Europe: Holds a significant position in the global HPPO process market, largely due to the region's pioneering role in developing and commercializing the technology. Companies headquartered in Germany and other Western European nations were among the first to scale up HPPO-based propylene oxide production, establishing a strong foundation of technical expertise and process know-how. The region's strict environmental regulations, particularly those governing hazardous chemical emissions and wastewater discharge, have long incentivized adoption of cleaner production routes such as HPPO. Demand from the polyurethane, surfactant, and pharmaceutical industries remains stable, underpinning consistent market activity. While capacity growth is more measured compared to Asia-Pacific, Europe maintains relevance through technological leadership, licensing activities, and high-value specialty applications of propylene oxide derivatives.

-

North America: Represents a mature but strategically important market for propylene oxide produced via the HPPO process. The United States hosts some of the world's largest propylene oxide consumers, particularly in the polyurethane and propylene glycol sectors serving automotive, construction, and food-grade applications. While the SMPO and chlorohydrin routes have historically dominated North American production, environmental pressures and operational cost considerations are gradually shifting interest toward HPPO technology for new capacity projects. Regulatory frameworks around chemical safety and environmental protection continue to create a favorable backdrop for cleaner production investments. Canada and Mexico are emerging as secondary contributors as North American companies explore regional integration and supply chain optimization strategies.

-

Middle East & Africa and South America: These regions represent the emerging frontier of the HPPO process market. The Middle East, particularly GCC nations such as Saudi Arabia and the UAE, is investing in downstream chemical diversification to move beyond crude oil and basic petrochemical exports toward higher-value specialty chemicals including propylene oxide. The availability of cost-competitive propylene feedstock from regional crackers provides a viable economic foundation for HPPO-based projects. South America, with Brazil as the primary driver, generates moderate demand for propylene oxide and its downstream derivatives, though economic volatility and infrastructure limitations have slowed the pace of domestic HPPO capacity buildout. Both regions present significant long-term growth opportunities driven by increasing industrialization and a growing chemical sector reform agenda.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308788/propylene-oxide-via-hydrogen-peroxide-process-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308788/propylene-oxide-via-hydrogen-peroxide-process-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/