Global VLSFO Market Growing at 5.2% CAGR with Rising Demand from Shipping Industry

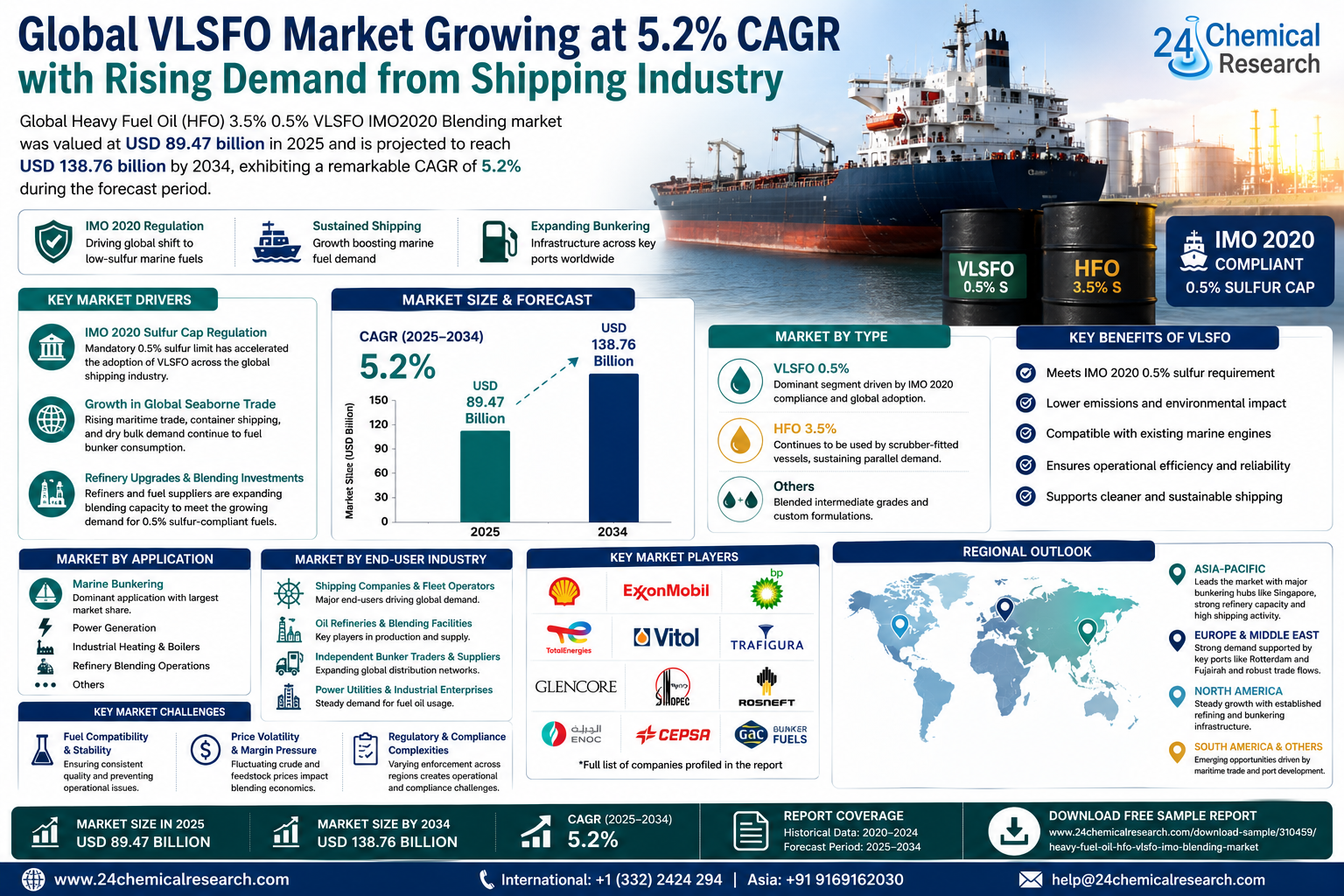

Global Heavy Fuel Oil (HFO) 3.5% 0.5% VLSFO IMO2020 Blending market was valued at USD 89.47 billion in 2025 and is projected to reach USD 138.76 billion by 2034, exhibiting a remarkable CAGR of 5.2% during the forecast period.

Heavy Fuel Oil (HFO) 3.5% refers to high-sulfur residual fuel oil traditionally used in marine vessels and industrial applications, characterized by a sulfur content of up to 3.5% by mass. With the International Maritime Organization's (IMO) 2020 regulation mandating a global sulfur cap of 0.5%, the industry witnessed a structural shift toward Very Low Sulfur Fuel Oil (VLSFO), which blends compliant low-sulfur distillates or residues to meet the 0.5% sulfur threshold. The IMO 2020 blending market encompasses the production, trading, and supply of these compliant fuel formulations across bunkering hubs worldwide.

The market continues to evolve as shipowners, refiners, and fuel suppliers navigate compliance requirements while managing cost efficiency. The adoption of VLSFO has been widespread, with key bunkering ports such as Singapore, Rotterdam, and Fujairah reporting sustained demand for 0.5% sulfur-compliant blends. Furthermore, vessels equipped with exhaust gas cleaning systems (scrubbers) continue to consume HFO 3.5%, sustaining demand for high-sulfur fuel oil in parallel. The interplay between scrubber-fitted fleets and VLSFO demand remains a defining dynamic of this blending market through the forecast period.

Get Full Report Here: https://www.24chemicalresearch.com/reports/310459/heavy-fuel-oil-hfo-vlsfo-imo-blending-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

IMO 2020 Sulfur Cap Regulation as a Fundamental Market Catalyst: The International Maritime Organization's global sulfur cap, which came into force on January 1, 2020, stands as the single most transformative regulatory event in modern marine fuel history. By mandating a reduction in marine fuel sulfur content from 3.5% to 0.5% outside Emission Control Areas (ECAs), IMO 2020 fundamentally restructured global bunker fuel demand patterns and accelerated the adoption of Very Low Sulfur Fuel Oil (VLSFO). Refiners and blenders rapidly repositioned their operations to supply compliant fuels, creating an entirely new blending market centered on achieving the 0.5% sulfur specification at competitive cost points.

-

Growth in Global Seaborne Trade Sustaining Bunker Fuel Volumes: Global seaborne trade volumes have continued to underpin robust demand for marine fuels, including both traditional High Sulfur Fuel Oil (HSFO at 3.5%) consumed by vessels fitted with exhaust gas cleaning systems (scrubbers) and VLSFO consumed by compliant vessels. Expanding container shipping routes, growing dry bulk commodity flows tied to infrastructure development in emerging economies, and rising liquefied natural gas (LNG) trade have all contributed to sustained blending activity. Furthermore, the continued build-out of scrubber-fitted fleets has preserved a meaningful market for high-sulfur residual fuel alongside VLSFO.

-

Refinery Upgrades and Blending Infrastructure Investments: Refinery configuration upgrades and investments in secondary processing units such as vacuum distillation, visbreakers, and solvent deasphalting have expanded the pool of available blend components. Major bunkering ports including Singapore, Rotterdam, Fujairah, and Houston have seen significant investment in blending and storage infrastructure to handle the complexity of multi-component VLSFO formulations, making this a competitively attractive market segment for integrated oil companies and independent operators.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310459/heavy-fuel-oil-hfo-vlsfo-imo-blending-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

Fuel Compatibility and Stability Issues in VLSFO Blending Operations: One of the most significant technical challenges confronting the VLSFO blending market is ensuring fuel stability and compatibility. VLSFO is typically produced by blending residual fuel oil components with distillate cutter stocks or low-sulfur residues. Incompatibility between VLSFO parcels from different suppliers has caused documented operational problems aboard vessels, including filter clogging, fuel pump failures, and loss of propulsion. This challenge imposes significant testing and quality assurance costs on blenders.

-

Price Volatility and Margin Compression: The economics of VLSFO blending are highly sensitive to the spread between distillate and residual fuel prices. When crude oil prices are volatile, blending margins can compress rapidly, challenging the profitability of independent blenders operating on thin margins. The HSFO–VLSFO price differential has narrowed as supply chains adjusted, affecting the premium value achievable on compliant VLSFO blends.

Critical Market Challenges Requiring Innovation

The transition from laboratory success to industrial-scale manufacturing presents its own set of challenges. Maintaining material consistency and ensuring dispersion stability in industrial formulations remains difficult, leading to issues such as asphaltene precipitation and sludge formation. These technical hurdles necessitate continued investments in quality control and testing protocols. Additionally, the market contends with regulatory enforcement disparities across jurisdictions, creating an uneven competitive landscape where compliant blenders bear full compliance costs while facing competition from less regulated operators.

Furthermore, the immature aspects of certain supply chains and volatility in feedstock availability create economic uncertainty for potential large-scale end-users. The need for sophisticated blending infrastructure at major hubs adds complexity and cost to operations.

Vast Market Opportunities on the Horizon

-

Expansion of Bunkering Infrastructure in Emerging Port Hubs: Rapid growth in maritime trade volumes through emerging bunkering centers in Southeast Asia, the Middle East, and East Africa is creating substantial commercial opportunities for VLSFO and HSFO blenders. Ports such as Port Klang, Tanjung Pelepas, Sohar, and Djibouti are actively developing bunker fuel storage and blending capacity. Independent blenders and trading companies that can secure reliable low-sulfur blend component supply chains in these emerging hubs stand to capture attractive margins.

-

Bio-Blended VLSFO and Transitional Low-Carbon Marine Fuel Development: The growing pressure on shipping companies to reduce their carbon intensity under frameworks such as the IMO's Carbon Intensity Indicator (CII) regulation and the EU Emissions Trading System is opening opportunities for bio-blended VLSFO products. By incorporating biogenic components into VLSFO blends, blenders can offer shipowners a cost-effective pathway to improve compliance without requiring vessel modifications. This represents a relatively capital-efficient diversification avenue for established VLSFO blenders.

-

Strategic Partnerships as a Catalyst: The market is witnessing increased collaboration between material producers, refiners, traders, and end-users to co-develop application-specific solutions. These alliances are crucial for addressing technical challenges, optimizing blend formulations, and securing long-term supply agreements, effectively supporting commercialization efforts and reducing time-to-market.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into High Sulfur Fuel Oil (HSFO) 3.5%, Very Low Sulfur Fuel Oil (VLSFO) 0.5%, and others. Very Low Sulfur Fuel Oil (VLSFO) 0.5% currently leads the market, favored for its regulatory compliance and widespread adoption across global shipping routes. The HSFO 3.5% segment remains relevant for vessels equipped with scrubbers, providing a parallel stream in the blending ecosystem. Blended intermediate grades continue to play a supporting role for operators seeking balanced cost and compliance solutions.

By Application:

Application segments include Marine Bunkering, Power Generation, Industrial Heating and Boilers, Refinery Blending Operations, and others. The Marine Bunkering segment currently dominates, driven by the massive scale of international shipping and the direct impact of IMO 2020 regulations on ocean-going vessels. However, the Refinery Blending Operations and Industrial segments are expected to exhibit steady relevance in the coming years as supply chains optimize and secondary uses evolve.

By End-User Industry:

The end-user landscape includes Shipping Companies and Fleet Operators, Oil Refineries and Blending Facilities, Independent Bunker Traders and Suppliers, and Power Utilities and Industrial Enterprises. The Shipping Companies and Fleet Operators industry accounts for the major share, leveraging both HSFO and VLSFO blends according to their chosen compliance strategies. The Oil Refineries and Independent Traders sectors are rapidly emerging as key participants, reflecting the trends in fuel production optimization and global distribution networks.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310459/heavy-fuel-oil-hfo-vlsfo-imo-blending-market

Competitive Landscape:

The global Heavy Fuel Oil HFO 3.5% 0.5% VLSFO IMO2020 Blending market is semi-consolidated and characterized by intense competition and rapid innovation. The top three companies—Shell plc, ExxonMobil Corporation, and BP plc—collectively command a significant share of the market. Their dominance is underpinned by extensive refining capabilities, advanced blending expertise, and established global distribution networks across major bunkering hubs.

List of Key Heavy Fuel Oil HFO 3.5% 0.5% VLSFO IMO2020 Blending Companies Profiled:

-

Shell plc (United Kingdom / Netherlands)

-

ExxonMobil Corporation (United States)

-

BP plc (United Kingdom)

-

TotalEnergies SE (France)

-

Vitol Group (Netherlands / Switzerland)

-

Trafigura Group (Singapore / Switzerland)

-

Glencore plc (Switzerland)

-

Sinopec Fuel Oil Sales Co., Ltd. (China)

-

Rosneft Oil Company (Russia)

-

Emirates National Oil Company (ENOC) (United Arab Emirates)

-

CEPSA (Spain)

-

GAC Bunker Fuels Ltd. (United Arab Emirates)

The competitive strategy is overwhelmingly focused on R&D to enhance blend quality and stability, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new formulations, thereby securing future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Is the undisputed leader in the global market. This dominance is fueled by the concentration of major bunkering hubs like Singapore, strong refinery capacity in China and South Korea, and robust demand from extensive shipping fleets operating across key trade routes. Singapore serves as the primary engine of growth in the region.

-

Europe & Middle East: Together, they form a powerful secondary bloc. Europe's strength is driven by established ports such as Rotterdam and stringent regulatory enforcement, while the Middle East benefits from Fujairah's strategic position and abundant residual fuel supply from regional refineries. Both areas support significant blending activity and global trade flows.

-

North America, South America, and Other Regions: These regions represent important markets with steady demand. While currently varying in scale, they present significant long-term growth opportunities driven by increasing maritime trade, port infrastructure development, and ongoing compliance with international fuel standards.

Get Full Report Here: https://www.24chemicalresearch.com/reports/310459/heavy-fuel-oil-hfo-vlsfo-imo-blending-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310459/heavy-fuel-oil-hfo-vlsfo-imo-blending-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/