Aerial Common Sensor Market, Trends, Business Strategies 2026-2034

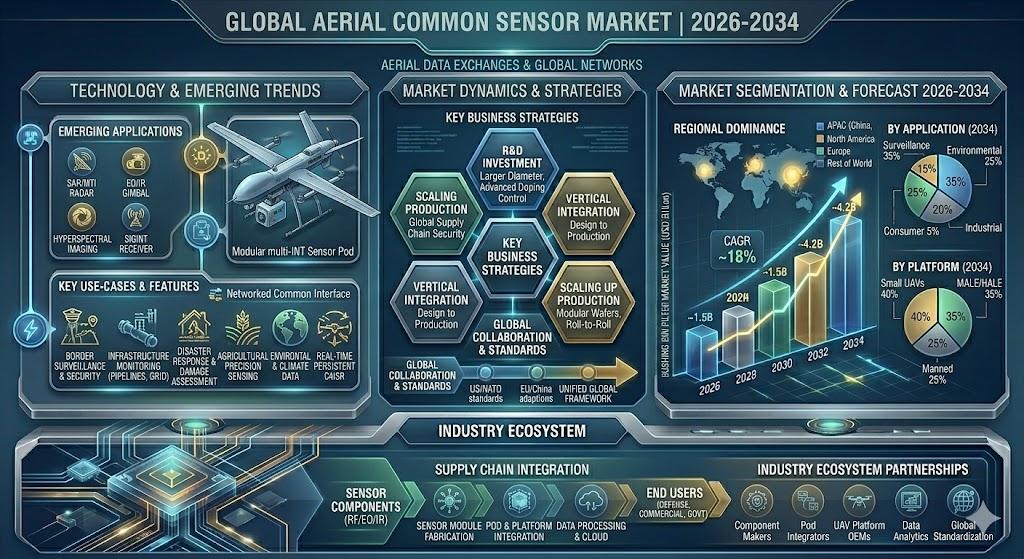

The global Aerial Common Sensor Market, valued at approximately USD 777 million in 2025, is on a trajectory of significant expansion, projected to reach USD 1,420 million by 2034. This growth, representing a compound annual growth rate (CAGR) of 9.2%, is detailed in a comprehensive new report published by Semiconductor Insight. The study highlights the critical role of these advanced multi-function sensor systems in delivering integrated intelligence, surveillance, and reconnaissance (ISR) capabilities across modern airborne platforms.

Aerial Common Sensor (ACS) systems integrate multiple sensor modalities including signals intelligence (SIGINT), imagery intelligence (IMINT), and electronic warfare capabilities into unified payloads. These systems are becoming indispensable for enhancing situational awareness, supporting mission planning, and enabling real-time decision-making in contested environments while minimizing platform integration complexity.

Download FREE Sample Report:

Aerial Common Sensor Market - View in Detailed Research Report

Rising Demand for Airborne ISR Capabilities: The Primary Growth Engine

The report identifies the increasing emphasis on intelligence, surveillance, and reconnaissance capabilities as the paramount driver for Aerial Common Sensor demand. Modern military operations require persistent, multi-domain awareness that single-sensor solutions cannot adequately provide. The integration of advanced ACS systems across fighter aircraft, helicopters, transport platforms, and unmanned aerial vehicles directly supports this strategic imperative.

"The growing complexity of geopolitical environments and the proliferation of advanced threats have accelerated investment in airborne sensor technologies capable of delivering fused, actionable intelligence," the report states. North America, led by the United States, remains the largest regional market, supported by sustained defense budgets and long-term platform modernization programs. Global military modernization initiatives and the expanding role of unmanned systems continue to drive substantial demand for these sophisticated sensor solutions.

Read Full Report: https://semiconductorinsight.com/report/aerial-common-sensor-market/

Market Segmentation: SIGINT and Multi-Sensor Fusion Lead Industry Direction

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

Segment Analysis:

|

Segment Category |

Sub-Segments |

Key Insights |

|

By Type |

|

SIGINT Sensor holds a leading position within the Aerial Common Sensor market by type, driven by the increasing strategic importance of electronic intelligence gathering in modern defense operations.

|

|

By Application |

|

Fighter Aircraft represents the dominant application segment in the Aerial Common Sensor market, owing to the critical need for real-time intelligence, surveillance, and reconnaissance capabilities integrated directly into combat platforms.

|

|

By End User |

|

Defense & Military constitutes the predominant end-user segment for Aerial Common Sensor systems, reflecting the platform's foundational design purpose of supporting armed forces with superior situational awareness in contested environments.

|

|

By Platform |

|

Unmanned Aerial Vehicles (UAVs) are establishing themselves as the fastest-growing platform segment within the Aerial Common Sensor market, fundamentally transforming how ISR missions are conceived, planned, and executed by defense and security organizations globally.

|

|

By Technology |

|

Multi-Sensor Fusion Systems represent the most strategically important technology segment in the Aerial Common Sensor market, reflecting a broader industry shift away from single-modality sensors toward integrated, data-fused ISR architectures capable of providing comprehensive battlefield awareness.

|

Get Full Report Here:

Aerial Common Sensor Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

Competitive Landscape: Key Players and Strategic Focus

COMPETITIVE LANDSCAPE

Key Industry Players

Global Aerial Common Sensor Market: Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

The global Aerial Common Sensor (ACS) market is characterized by the strong dominance of a handful of large-scale defense and aerospace conglomerates, with Lockheed Martin and Raytheon Technologies commanding significant revenue shares among the top five players, who collectively accounted for a substantial portion of global market revenue in 2025. Valued at approximately USD 777 million in 2025 and projected to reach USD 1,420 million by 2034 at a CAGR of 9.2%, the market reflects robust demand driven by rising military modernization programs, growing investments in airborne ISR (Intelligence, Surveillance, and Reconnaissance) platforms, and the increasing integration of SIGINT and IMINT sensor technologies across fighter aircraft, helicopters, transport aircraft, and unmanned aerial platforms. North America, led by the United States, remains the largest regional market, with these prime contractors benefiting from long-standing defense procurement relationships and deep integration across military supply chains. Companies such as Honeywell International, Thales Group, and Safran SA further reinforce the competitive intensity through continuous R&D investment, advanced sensor fusion capabilities, and strategic partnerships with military agencies worldwide.

Beyond the market leaders, several niche yet significant players are shaping the ACS competitive landscape through specialization and technological differentiation. General Atomics has established a strong foothold through its expertise in unmanned aerial systems, making it a key platform provider for sensor integration. L3 Harris Technologies Inc. brings advanced signals intelligence and electronic warfare capabilities that closely align with the SIGINT sensor segment's growth trajectory. Curtiss-Wright Corporation and Ametek Inc. contribute ruggedized electronics and embedded computing solutions critical to mission-grade airborne sensor systems, while Meggitt PLC delivers sensing and monitoring technologies suited for demanding aerospace environments. AgEagle Aerial Systems represents the growing role of smaller, commercially oriented UAV-focused companies entering the ISR space. Together, these players compete across product innovation, platform compatibility, cost-efficiency, and responsiveness to evolving defense procurement requirements across North America, Europe, Asia-Pacific, and the Middle East and Africa regions.

List of Key Aerial Common Sensor Companies Profiled

-

Honeywell International

-

Safran SA

-

General Atomics

-

Curtiss-Wright Corporation

-

Ametek Inc.

-

Meggitt PLC

-

AgEagle Aerial Systems

These companies are focusing on technological advancements, such as enhanced sensor fusion algorithms, modular payload designs, and expanded integration with unmanned platforms to capitalize on emerging opportunities in the global defense sector.

Regional Analysis: Aerial Common Sensor Market

Regional Analysis: Aerial Common Sensor Market

North America

North America continues to assert its dominance in the global Aerial Common Sensor market, driven by sustained defense modernization programs, robust military budgets, and a deeply embedded culture of technological innovation. The United States, in particular, functions as the primary engine of demand, with its armed forces consistently prioritizing intelligence, surveillance, and reconnaissance (ISR) capabilities that rely heavily on advanced aerial sensor systems. The country's defense procurement frameworks actively support the development and integration of multi-mission sensor platforms capable of operating across diverse threat environments. Canada contributes meaningfully to the regional landscape through its participation in joint defense initiatives and interoperability commitments under NATO frameworks. The presence of leading aerospace and defense contractors across the region ensures that research, development, and production capabilities for the Aerial Common Sensor market remain highly concentrated and competitive. Additionally, significant investments in unmanned aerial vehicle (UAV) programs and next-generation airborne reconnaissance platforms are reinforcing North America's leadership position. The region benefits from a well-established regulatory environment, strong intellectual property protections, and close collaboration between government agencies and private defense contractors, all of which collectively accelerate market maturation and innovation cycles within the Aerial Common Sensor industry.

Defense Procurement & Budget Strength

North America's Aerial Common Sensor market benefits immensely from one of the world's largest defense budgets. Consistent government allocations toward airborne intelligence and surveillance modernization ensure sustained demand. Multi-year procurement contracts between defense agencies and industry leaders provide market stability and encourage long-term investment in next-generation aerial sensor architectures, keeping the region at the forefront of global capability development.

Technological Innovation Ecosystem

The region hosts a dense ecosystem of aerospace primes, specialized sensor manufacturers, and defense-focused research institutions. This interconnected network accelerates the pace of innovation in the Aerial Common Sensor market, enabling rapid prototyping, testing, and deployment of advanced multi-spectral and signals intelligence sensor payloads integrated onto both manned and unmanned aerial platforms across various operational environments.

UAV & Unmanned Platform Integration

North America leads globally in the development and deployment of unmanned aerial systems configured with common sensor suites. The growing preference for persistent, low-risk ISR missions is driving the integration of Aerial Common Sensor technologies onto medium and high-altitude long-endurance UAV platforms. This trend reflects a broader operational shift toward remotely piloted intelligence gathering across contested and denied airspace environments.

Allied Cooperation & Export Potential

Strong bilateral and multilateral defense relationships enable North American Aerial Common Sensor market participants to expand their reach through foreign military sales and cooperative development agreements. NATO interoperability standards and Five Eyes intelligence-sharing frameworks create additional demand for compatible aerial sensor solutions, expanding the addressable market well beyond domestic borders and reinforcing the region's strategic influence in global defense technology ecosystems.

Europe

Europe represents a strategically significant and rapidly evolving segment of the Aerial Common Sensor market. The region's market dynamics are shaped by collective NATO commitments, national defense modernization programs, and a growing emphasis on European strategic autonomy in defense capabilities. Countries such as the United Kingdom, France, Germany, and Italy are key contributors, investing in indigenous aerial surveillance technologies while also participating in collaborative multinational programs. The resurgence of geopolitical tensions on the European continent has accelerated procurement timelines and broadened the scope of airborne reconnaissance requirements. European defense agencies are increasingly prioritizing sensor fusion, interoperability, and open-architecture platforms that can adapt to evolving threat environments. The presence of established aerospace conglomerates and a strong industrial base ensures that Europe remains a competitive and innovative force within the global Aerial Common Sensor market through the forecast period.

Asia-Pacific

The Asia-Pacific region is emerging as one of the most dynamic growth frontiers in the Aerial Common Sensor market, underpinned by rising defense expenditures, territorial disputes, and rapid modernization of air force capabilities across multiple nations. Countries including China, India, Japan, South Korea, and Australia are making substantial investments in airborne intelligence and surveillance platforms to address complex regional security challenges. India's push for defense indigenization and Japan's evolving security posture are particularly noteworthy drivers. The region's diverse threat landscape, spanning maritime domain awareness to counter-insurgency operations, creates multifaceted demand for versatile aerial sensor solutions. Growing domestic defense industrial bases in several Asia-Pacific nations are also reducing reliance on imports, fostering local capability development in the Aerial Common Sensor market and positioning the region as a long-term structural growth driver globally.

South America

South America occupies a developing but increasingly relevant position within the global Aerial Common Sensor market. Regional demand is primarily driven by border surveillance requirements, counter-narcotics operations, and the need to monitor vast and geographically challenging territories. Brazil, as the region's largest defense spender, plays a central role in shaping procurement trends, with ongoing investments in airborne surveillance and reconnaissance platforms. Other nations including Colombia and Peru are also expanding their aerial ISR capabilities to address internal security challenges. Budget constraints and competing national priorities can moderate growth, yet growing concerns over border security and the proliferation of non-state actor threats are gradually expanding the addressable market. International defense partnerships and foreign military assistance programs also introduce advanced Aerial Common Sensor technologies into the South American operational environment.

Middle East & Africa

The Middle East and Africa region presents a compelling mix of near-term demand intensity and long-term market potential for the Aerial Common Sensor market. The Middle East, driven by nations such as Saudi Arabia, the United Arab Emirates, and Israel, maintains some of the highest per-capita defense spending globally, with significant allocations directed toward airborne ISR and electronic warfare capabilities. Israel, in particular, stands out as both a major consumer and a sophisticated exporter of aerial sensor technologies. Ongoing regional conflicts and the persistent threat of asymmetric warfare sustain demand for advanced reconnaissance and surveillance systems. In Sub-Saharan Africa, the Aerial Common Sensor market is at a nascent stage, with growth linked to peacekeeping missions, counter-terrorism operations, and increasing external defense assistance programs that are gradually introducing modern aerial surveillance platforms to the continent.

Emerging Opportunities in Unmanned Systems and Multi-Domain Operations

Beyond traditional drivers, the report outlines significant emerging opportunities. The rapid expansion of unmanned aerial vehicle programs and the shift toward multi-domain operations present new growth avenues, requiring highly integrated and modular sensor solutions. Furthermore, the integration of artificial intelligence and machine learning for automated target recognition and data processing represents a major trend that is expected to enhance operational effectiveness and reduce analyst workload.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Aerial Common Sensor markets from 2025–2034. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/aerial-common-sensor-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=141881

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us