Green Hydrogen Production Market Set for Explosive Growth to USD 198.02 Billion by 2034 Driven by Decarbonization and Clean Energy Demand

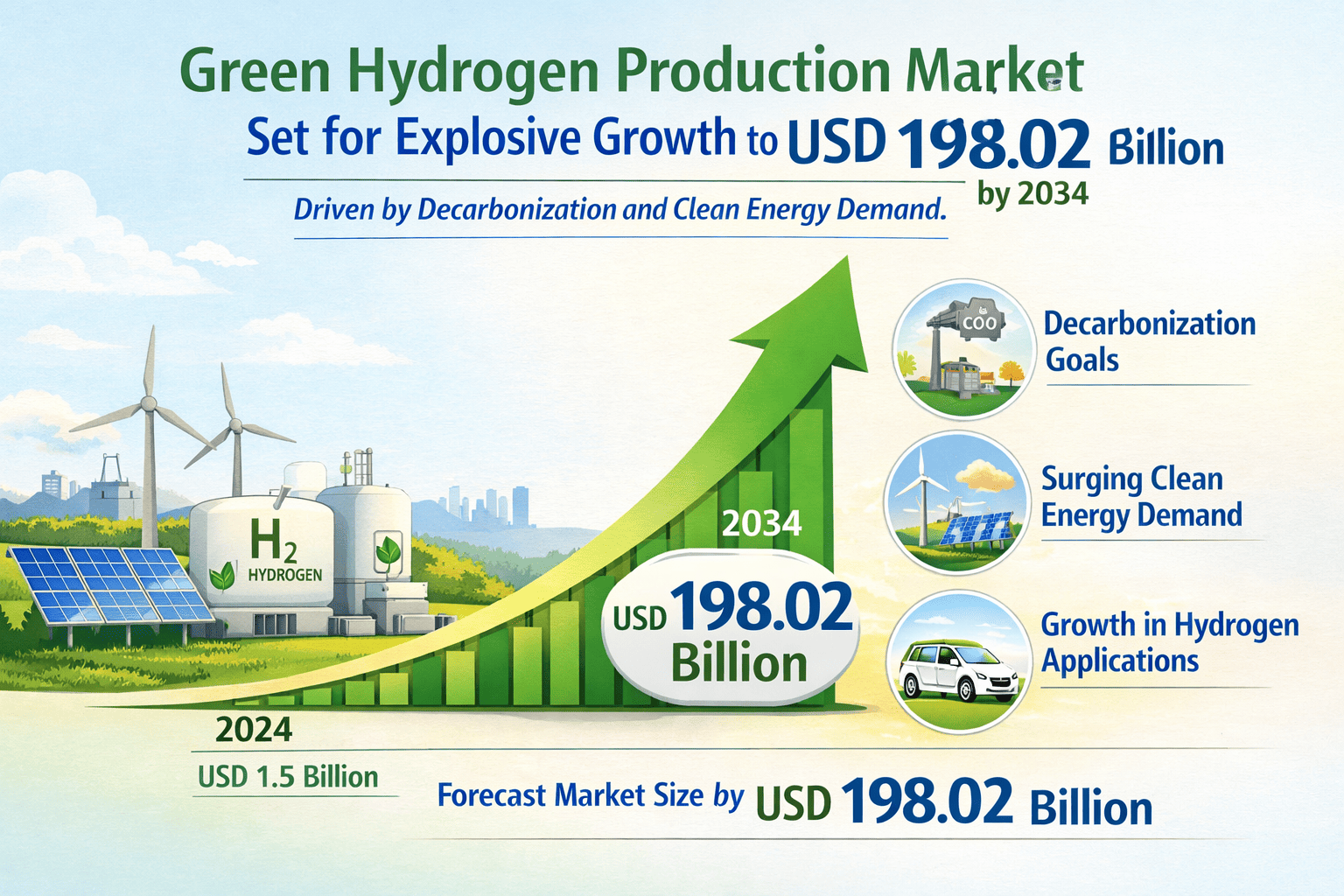

Global Green Hydrogen Production market was valued at USD 8.41 billion in 2025 and is projected to reach USD 198.02 billion by 2034, exhibiting a remarkable CAGR of 58.5% during the forecast period.

Green hydrogen, produced by splitting water into hydrogen and oxygen using renewable electricity, represents the most promising pathway to decarbonize heavy industry and transportation sectors. Unlike conventional hydrogen production methods that rely on fossil fuels, green hydrogen generates zero carbon emissions at the point of production. This clean energy carrier is rapidly transitioning from pilot projects to large-scale commercial deployments, driven by global climate commitments and technological advancements.

Get Full Report Here: https://www.24chemicalresearch.com/reports/306178/green-hydrogen-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Global Decarbonization Imperative: The unprecedented global push toward net-zero emissions, reinforced by the Paris Agreement and national climate policies, is the primary catalyst for green hydrogen adoption. Governments worldwide are implementing ambitious hydrogen strategies backed by substantial funding, such as the European Union's Hydrogen Strategy and the US Inflation Reduction Act, which provides tax credits up to $3 per kilogram of green hydrogen produced. This policy support creates a stable investment environment and accelerates project development across the value chain.

-

Falling Renewable Energy Costs: The dramatic reduction in renewable electricity costs, particularly from solar and wind power, has significantly improved the economics of green hydrogen production. Solar photovoltaic costs have decreased by approximately 85% over the past decade, while wind power costs have dropped by about 55%. This cost reduction directly impacts the largest operational expense in electrolysis, making green hydrogen increasingly competitive with fossil fuel-based alternatives and driving wider adoption across multiple sectors.

-

Energy Security and Industrial Demand: Growing emphasis on energy independence is prompting nations to develop domestic green hydrogen capabilities, reducing reliance on imported fossil fuels. Simultaneously, hard-to-abate industrial sectors such as steel manufacturing, chemical production, and heavy transportation are actively seeking green hydrogen solutions to meet their decarbonization targets. This convergence of energy security concerns and industrial demand creates a robust, multi-faceted growth foundation for the market.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/306178/green-hydrogen-market

Significant Market Restraints Challenging Adoption

Despite its immense potential, the market faces substantial hurdles that must be overcome to achieve widespread commercialization.

-

High Production and Infrastructure Costs: The capital expenditure required for large-scale electrolyzer facilities remains substantial, with current system costs ranging between $700-$1,400 per kW depending on technology and scale. Additionally, the development of dedicated hydrogen transportation and storage infrastructure requires massive investment, creating a significant financial barrier. These high costs currently position green hydrogen at a price disadvantage compared to conventional hydrogen production methods, necessitating continued technological innovation and scale economies.

-

Regulatory and Certification Challenges: The absence of globally harmonized standards for defining and certifying 'green' hydrogen creates market uncertainty and potential for greenwashing. Varying certification requirements across regions complicate international trade and project financing. Furthermore, the permitting process for large-scale hydrogen projects can be lengthy and complex, particularly for projects involving new pipeline infrastructure or offshore wind integration, potentially delaying market expansion.

Critical Market Challenges Requiring Innovation

The transition from demonstration projects to gigawatt-scale commercialization presents several technical and logistical challenges that require innovative solutions.

Scaling electrolyzer manufacturing to meet projected demand represents a significant challenge, with current global manufacturing capacity needing to expand more than tenfold by 2030. Supply chain constraints for critical materials, particularly iridium for PEM electrolyzers and rare earth elements for certain renewable components, could potentially bottleneck growth if not addressed through material innovation and recycling initiatives.

Additionally, integrating intermittent renewable energy sources with electrolysis operations requires sophisticated energy management systems and potentially large-scale energy storage solutions. The variability of solar and wind power necessitates either grid connectivity, which may involve additional costs and complexities, or complementary storage technologies to ensure consistent hydrogen production, adding another layer of technical challenge to project development.

Vast Market Opportunities on the Horizon

-

Industrial Decarbonization Leadership: Green hydrogen offers the most viable pathway to decarbonize fundamental industrial processes that are otherwise difficult to electrify. In steel manufacturing, hydrogen-based direct reduction technology can potentially reduce emissions by 95% compared to conventional blast furnace methods. Similarly, the fertilizer industry can transition from natural gas-based ammonia production to green ammonia, creating massive demand potential while significantly reducing the carbon footprint of global food production systems.

-

Energy Storage and Grid Services: Green hydrogen provides a unique solution for long-duration energy storage, addressing the critical challenge of seasonal renewable energy variability. Excess renewable electricity can be converted to hydrogen during periods of high generation and stored for weeks or months, then reconverted to electricity or used as clean fuel during periods of low renewable output. This capability becomes increasingly valuable as renewable penetration grows, offering grid stability services that battery storage cannot economically provide over extended durations.

-

Emerging Export Markets and Hydrogen Hubs: Regions with exceptional renewable resources are positioning themselves as future green hydrogen exporters, particularly to energy-intensive economies with limited renewable potential. Countries in the Middle East, North Africa, and South America are developing large-scale projects aimed at exporting green hydrogen or its derivatives like ammonia to European and Asian markets. Simultaneously, regional hydrogen hubs are emerging where co-located renewable generation, production facilities, and offtakers create integrated ecosystems that optimize costs and accelerate adoption.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Technology:

The market is segmented primarily into Alkaline Electrolyzers, Proton Exchange Membrane (PEM) Electrolyzers, and Solid Oxide Electrolyzers. Alkaline Electrolyzers currently dominate the market, favored for their technological maturity, reliability, and lower capital costs, making them suitable for large-scale, continuous industrial applications. PEM electrolyzers are gaining significant traction due to their operational flexibility and ability to handle variable renewable power inputs effectively.

By Application:

Application segments include Transportation, Power Generation, Industrial Feedstock, and Others. The Industrial Feedstock segment currently represents the largest application, driven by the urgent need to decarbonize existing hydrogen consumption in refining and chemical production. However, the Transportation segment is expected to exhibit the highest growth rate as hydrogen fuel cell vehicles gain adoption in heavy-duty trucking, shipping, and eventually aviation applications.

By End-User Industry:

The end-user landscape encompasses Chemicals, Refining, Transportation, Power Generation, and Others. The Chemicals industry accounts for the major share, particularly for ammonia and methanol production. The Transportation and Power Generation sectors are rapidly emerging as key growth end-users, reflecting broader electrification and decarbonization trends across the global economy.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/306178/green-hydrogen-market

Competitive Landscape:

The global Green Hydrogen Production market is characterized by the participation of diverse players including established industrial gas companies, energy majors, specialized technology providers, and increasingly, renewable energy developers. The market structure is evolving rapidly as traditional energy companies pivot toward clean energy and new entrants bring innovative technologies to market.

List of Key Green Hydrogen Production Companies Profiled:

-

Air Products (USA)

-

Linde plc (UK/Ireland)

-

Siemens Energy (Germany)

-

ITM Power (UK)

-

Air Liquide (France)

-

Nel ASA (Norway)

-

Shell plc (Netherlands/UK)

-

ENGIE (France)

-

Bloom Energy (USA)

-

FuelCell Energy (USA)

-

China State Shipbuilding Corporation (China)

-

Sinopec (China)

Competitive strategies are predominantly focused on technological innovation to improve electrolyzer efficiency and reduce costs, alongside forming strategic partnerships across the value chain. Companies are increasingly engaging in vertical integration, combining renewable energy development with hydrogen production and offtake agreements to create economically viable projects. The race to demonstrate megawatt and gigawatt-scale projects is intensifying, with successful demonstration serving as a key competitive differentiator.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Europe: Is the current leader in green hydrogen development, driven by ambitious policy frameworks including the EU Hydrogen Strategy and substantial funding mechanisms. The region benefits from strong cross-border collaboration, advanced infrastructure planning, and significant industrial demand for decarbonization. Germany, France, and the Netherlands are particularly active, with numerous large-scale projects underway and a well-developed regulatory environment supporting market growth.

-

Asia-Pacific: Represents both a massive future demand center and increasingly a production hub, particularly in China, Japan, and South Korea. China's leadership in electrolyzer manufacturing and renewable energy deployment positions it as a critical player in reducing global costs. Japan and South Korea have developed comprehensive hydrogen strategies focused on both domestic production and import partnerships to meet their substantial energy needs and decarbonization goals.

-

North America: Is experiencing rapid market growth accelerated by the Inflation Reduction Act's generous tax incentives. The United States possesses abundant renewable resources and industrial demand, creating favorable conditions for large-scale project development. Canada is also emerging as a significant player, leveraging its clean electricity grid and strategic positioning for export opportunities to both Asia and Europe.

Get Full Report Here: https://www.24chemicalresearch.com/reports/306178/green-hydrogen-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/306178/green-hydrogen-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/