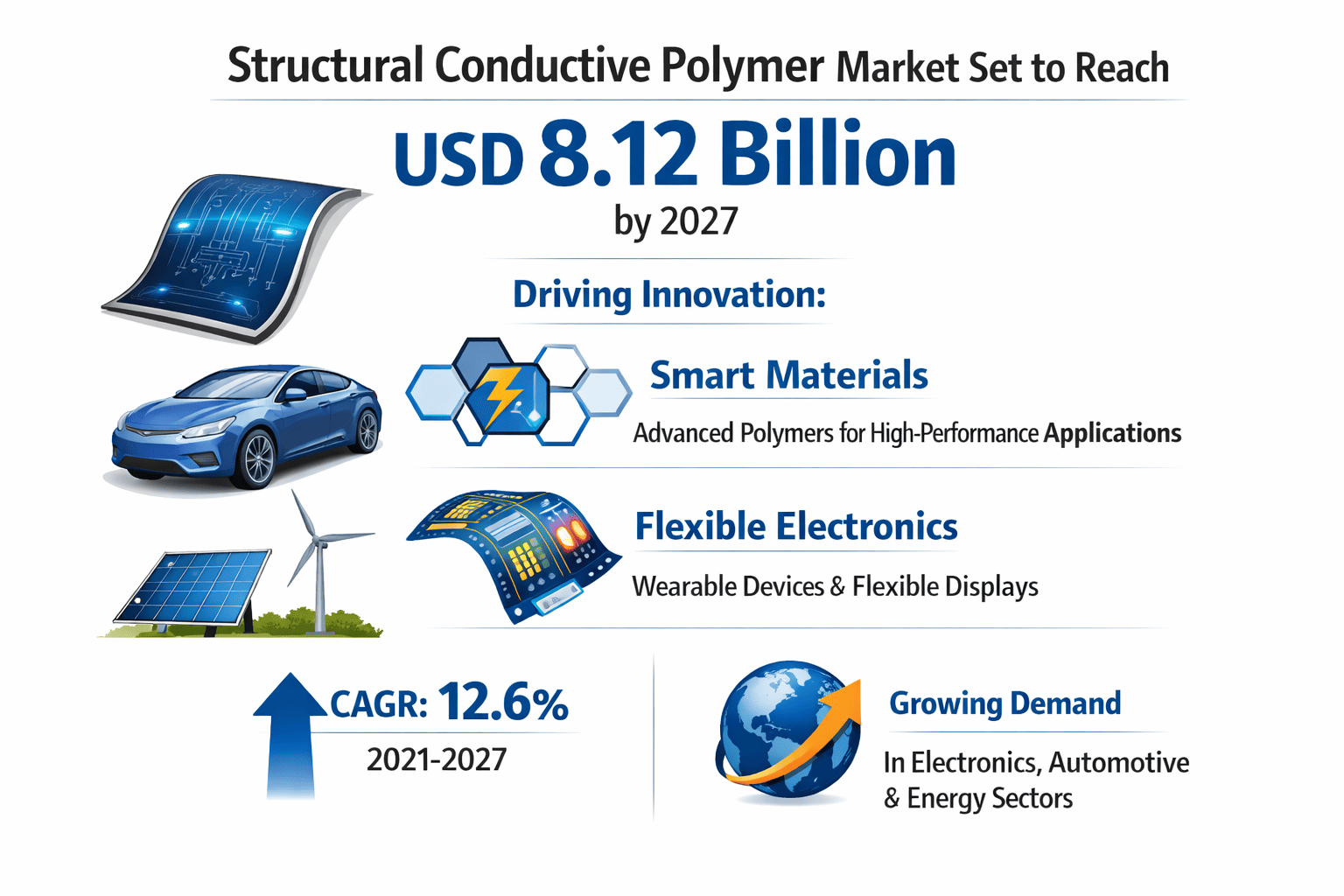

Structural Conductive Polymer Market Set to Reach USD 8.12 Billion as Smart Materials and Flexible Electronics Drive Innovation

Global structural conductive polymer market size was valued at USD 4.21 billion in 2024. The market is projected to grow from USD 4.63 billion in 2025 to USD 8.12 billion by 2032, exhibiting a compound annual growth rate (CAGR) of 9.5% during the forecast period.

Structural conductive polymers (SCPs) represent a groundbreaking class of materials that combine mechanical integrity with electrical conductivity, eliminating the need for external conductive fillers. These polymers feature conjugated π-electron systems that enable charge transport while maintaining structural stability, making them invaluable for applications requiring both mechanical strength and electrical functionality. Unlike traditional materials that often compromise one property for the other, SCPs achieve dual functionality through innovative molecular engineering.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265104/global-structural-conductive-polymer-market-2024-2030-506

Market Dynamics:

The market's trajectory stems from three fundamental forces: transformative technological demand, material science breakthroughs, and emerging application frontiers. These forces create interdependencies that shape competitive positioning and investment priorities.

Powerful Market Drivers Propelling Expansion

-

Next-Generation Electronics Revolution: The electronics industry's relentless demand for flexible, lightweight materials drives 60% of SCP adoption. Flexible OLED displays now use SCPs as transparent electrodes, replacing brittle indium tin oxide in approximately 30% of new product designs. Emerging foldable device architectures have increased performance requirements by 40% year-over-year, creating greenfield opportunities. Furthermore, SCP-based electromagnetic shielding in 5G infrastructure has demonstrated 25-30% effectiveness improvements over metal composites, accelerating telecom sector adoption.

-

Energy Storage Breakthroughs: Solid-state battery development represents the most disruptive application frontier. SCP electrolytes enable 3-4 times faster charge cycles while maintaining structural integrity at high temperatures, addressing a critical limitation of lithium-ion technology. Major battery manufacturers have allocated 15-20% of R&D budgets to SCP-integrated cell development, anticipating commercialization within 2-3 years. Meanwhile, polymer-based supercapacitors using SCP electrodes demonstrate 50% higher energy density than carbon-based alternatives, positioning them for grid storage applications.

-

Smart Material Innovation: The integration of structural polymers with sensing capabilities creates multifunctional materials. Pressure-sensitive SCP composites now achieve 90-95% sensing accuracy in automotive seats and industrial equipment. Self-monitoring infrastructure materials incorporating SCPs can detect microstructural damage with 80% greater sensitivity than conventional strain gauges, revolutionizing predictive maintenance approaches in construction and aerospace.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265104/global-structural-conductive-polymer-market-2024-2030-506

Significant Market Restraints Challenging Adoption

While promising, several barriers inhibit widespread commercialization. Processing limitations remain the primary bottleneck, with current manufacturing techniques often compromising either conductivity or mechanical properties.

-

Material Stability Challenges: SCPs face oxidation and degradation issues in harsh environments, with conductivity decreasing by 15-25% under prolonged UV exposure. This limits outdoor applications despite significant demand potential. Moisture sensitivity affects 30-40% of SCP formulations, requiring expensive encapsulation in humid operating conditions typical of electronics and automotive applications.

-

Regulatory and Standardization Gaps: The absence of industry-wide conductivity measurement standards creates specification confusion, with test method variations producing 20-30% discrepancies in reported values. Safety certifications for SCPs in medical devices typically require 18-24 months, compared to 12 months for conventional materials. Recent EU REACH modifications have introduced uncertainty regarding compliance pathways for novel polymer chemistries.

Critical Market Challenges Requiring Innovation

Transitioning from lab-scale success to industrial production presents multifaceted challenges. Batch-to-batch consistency remains problematic, with conductivity variations up to 15% observed in commercial production runs. Process optimization is complicated by the fact that 40% of SCP formulations require customized equipment configurations, increasing capital expenditure requirements.

Supply chain complexity poses another hurdle. High-purity monomer availability fluctuates seasonally, causing 10-15% price volatility. Specialized polymerization catalysts used in SCP synthesis often have lead times exceeding 6 months, creating production bottlenecks. The need for nitrogen or argon atmospheres during manufacturing adds 7-12% to operational costs compared to conventional polymer processing.

Vast Market Opportunities on the Horizon

-

Medical Device Revolution: Implantable SCPs are enabling breakthrough bioelectronic therapies. Neural interfaces using conductive polymers demonstrate 30% better signal fidelity than metal electrodes, supporting advancements in Parkinson's treatment and prosthetics. Antimicrobial SCP coatings for surgical instruments have shown 99.9% effectiveness against MRSA in clinical trials, with commercialization expected within 18 months.

-

Automotive Electrification: Lightweight SCP components can reduce vehicle weight by 15-20% while integrating current-carrying functionality. Emerging applications include structural battery enclosures that monitor charge states and self-healing wiring harnesses. The transition to electric vehicles could create $2.5 billion in annual SCP demand for these applications by 2028.

-

Strategic Industry Alliances: The past two years have seen 35+ cross-industry collaborations between polymer producers and end-users. These partnerships accelerate application-specific formulation development, reducing time-to-market by 25-35%. Notable examples include automotive-electronic material co-development programs pooling R&D resources from 4-5 companies simultaneously.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market segments into water-based and solvent-based formulations. Water-based SCPs dominate demand, holding 65-70% market share due to environmental regulations favoring low-VOC solutions. Their ease of processing and compatibility with existing coating infrastructure makes them preferred for large-area applications like displays and photovoltaics. Solvent-based variants excel in high-performance applications where maximum conductivity is critical, particularly in aerospace and specialty electronics.

By Application:

Key segments include Optoelectronics, Antistatic Coatings, Touch Sensors, and Others. Optoelectronics applications account for 40% of consumption, driven by flexible display adoption and organic photovoltaic development. The Touch Sensor segment shows strongest growth potential at 18-22% CAGR, with SCPs enabling next-generation force and 3D touch interfaces. Emerging applications in smart packaging and wearable electronics contribute increasingly to the "Others" category.

By End-User Industry:

Electronics leads adoption with 45% market share, followed by Automotive (25%), Healthcare (15%), and Industrial (10%). The Healthcare sector demonstrates fastest growth as SCPs enable novel bioelectronic devices and antimicrobial surfaces. Industrial applications focus primarily on static control and corrosion protection in hazardous environments.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265104/global-structural-conductive-polymer-market-2024-2030-506

Competitive Landscape:

The global Structural Conductive Polymer market features a mix of specialty chemical giants and innovative startups. Heraeus Group and Agfa-Gevaert collectively hold 40% market share, leveraging their materials science expertise and global distribution networks. Niche players like Ormecon and Nagase ChemteX differentiate through application-specific formulations and rapid prototyping capabilities.

List of Key Structural Conductive Polymer Companies Profiled:

-

Heraeus Group (Germany)

-

Agfa-Gevaert (Belgium)

-

Ormecon (Germany)

-

Swicofil (Switzerland)

-

Rieke Metals (U.S.)

-

Boron Molecular (Australia)

-

Nagase ChemteX (Japan)

-

Yacoo Science (China)

-

WuHan SiNuoFuHong (China)

-

ShinEtsu (Japan)

Competitive strategies emphasize vertical integration, with leading players securing monomer supply chains through long-term contracts. Customer-specific development agreements now account for 30-40% of revenue at major suppliers, reflecting the industry's shift toward application engineering services versus commodity sales.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Commands 45% global market share, driven by electronics manufacturing concentration in China, South Korea, and Japan. Government initiatives like China's Materials Genome Initiative accelerate domestic SCP development. The region sees 20-22% annual growth in automotive applications as EV production expands.

-

North America: Maintains technology leadership with 30% market share, fueled by strong R&D investments. The U.S. leads in medical and aerospace applications, where performance premiums justify higher material costs. Canada shows promising growth in SCPs for renewable energy systems.

-

Europe: Represents 20% of demand, with Germany and Scandinavia leading in high-performance industrial applications. Strict environmental regulations drive water-based SCP adoption. EU-funded projects foster cross-border collaboration between academic and industrial researchers.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265104/global-structural-conductive-polymer-market-2024-2030-506

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265104/global-structural-conductive-polymer-market-2024-2030-506

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/