Silicon-Infiltrated Silicon Carbide Market Accelerates with Semiconductor and EV Demand, Reaching USD 807 Million by 2034

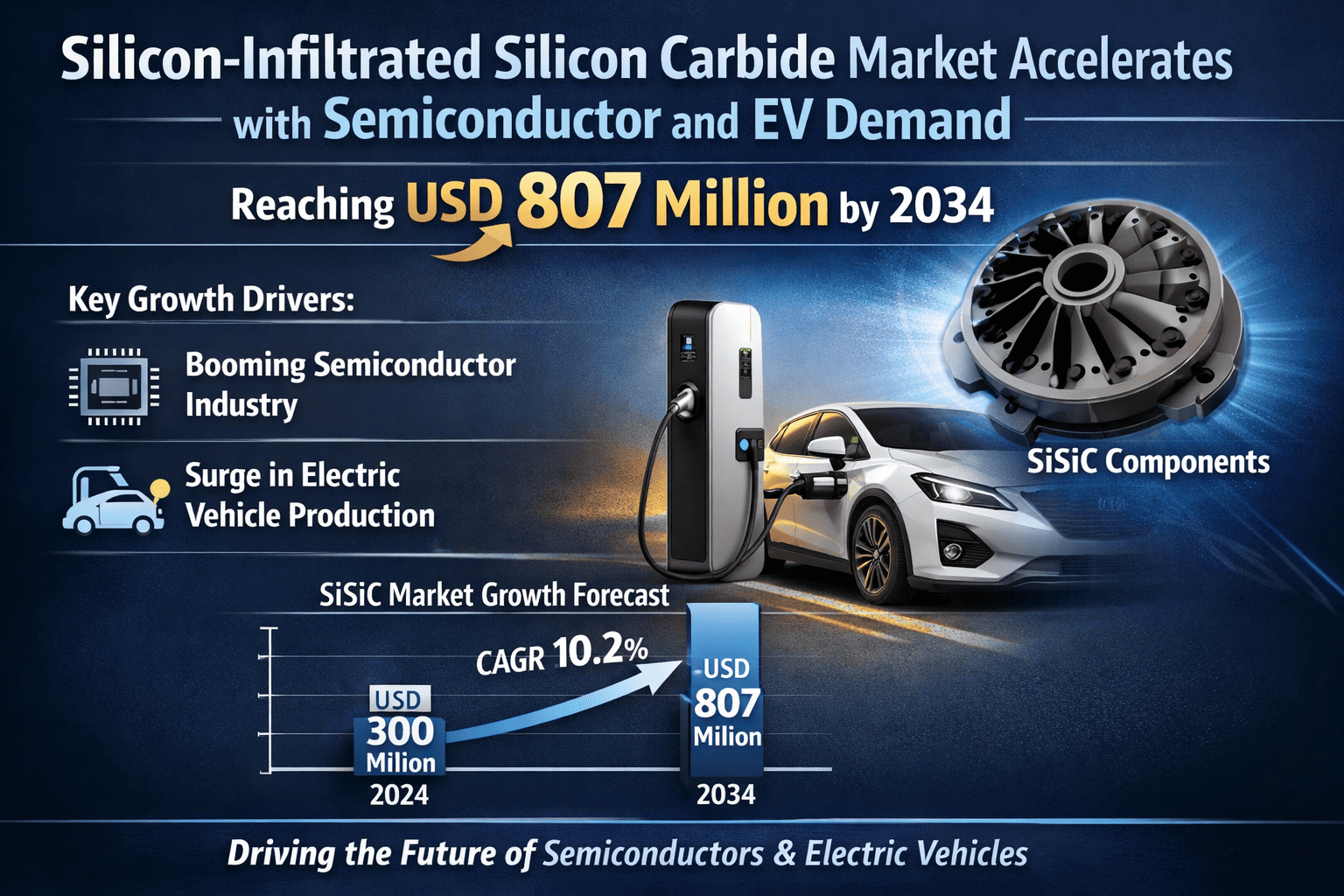

Global Silicon-Infiltrated Silicon Carbide (SiSiC) market was valued at USD 504 million in 2025 and is projected to grow from USD 539 million in 2026 to USD 807 million by 2034, exhibiting a steady CAGR of 7.0% during the forecast period.

Silicon-Infiltrated Silicon Carbide is an advanced ceramic composite material engineered through the infiltration of molten silicon into a porous silicon carbide preform. This sophisticated manufacturing process yields a dense, near-net-shape material distinguished by its exceptional combination of high thermal conductivity, outstanding mechanical strength, superior corrosion resistance, and remarkable thermal shock resistance. These properties, rarely found together in a single material, have elevated SiSiC from a niche specialty ceramic to an indispensable enabler of precision in industries where conventional materials simply cannot perform. Its applications span semiconductor fabrication equipment, high-precision machine tool structures, mirror substrates for advanced optical systems, and an expanding range of industrial components exposed to some of the most extreme operating environments on the planet.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307057/siliconinfiltrated-silicon-carbide-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that are only beginning to be explored by leading industry participants.

Powerful Market Drivers Propelling Expansion

-

Surging Demand from Semiconductor Manufacturing Equipment: The semiconductor industry's relentless push toward miniaturization and the fabrication of next-generation chips represents the single most powerful growth vector for the SiSiC market. As chip manufacturers invest heavily in advanced process nodes, the equipment used in wafer handling, etching, chemical vapor deposition, and lithography must meet ever-stricter standards for dimensional stability, thermal management, and plasma resistance. SiSiC meets all of these requirements simultaneously. Its near-zero porosity prevents particle contamination in ultra-clean fab environments, while its thermal conductivity and low coefficient of thermal expansion ensure that critical components maintain their precise geometries even under intense thermal cycling. With the global semiconductor equipment market itself expanding at a healthy pace, the pull-through demand for high-performance SiSiC components is both immediate and durable.

-

Expanding Footprint in Renewable Energy and Electric Vehicles: The global energy transition is opening significant new avenues for SiSiC adoption. In photovoltaic manufacturing, the equipment used to produce solar cells demands materials that can endure high-temperature processing environments without dimensional drift, making SiSiC an ideal structural material for diffusion furnace components and susceptors. Simultaneously, the electric vehicle revolution is driving interest in SiSiC for power electronics applications, where the material's thermal management properties enable more efficient and compact inverter designs. Major automotive OEMs have reported meaningful efficiency improvements in power modules incorporating advanced silicon carbide-based solutions, reflecting the broader industry trend toward materials that support higher power density with lower thermal resistance. This convergence of clean energy and electromobility trends creates a genuinely broad and growing addressable market for SiSiC producers.

-

Advancements in Precision Engineering and Optical Systems: The aerospace, defense, and scientific instrumentation sectors are increasingly specifying SiSiC for mirror substrates, telescope structures, and precision positioning stages. The material's extraordinarily high specific stiffness - a ratio of elastic modulus to density that surpasses most competing materials - combined with its low and predictable thermal expansion makes it uniquely suited for applications where nanometer-level dimensional stability is non-negotiable. Space telescope mirror blanks and airborne reconnaissance system structures fabricated from SiSiC offer weight savings alongside the thermal stability required to maintain optical alignment across the wide temperature swings encountered in operational environments. As global investments in defense modernization, satellite infrastructure, and scientific research continue to grow, this premium application segment provides a steady and high-value demand base for the market.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307057/siliconinfiltrated-silicon-carbide-market

Significant Market Restraints Challenging Adoption

Despite the compelling performance advantages SiSiC offers across multiple high-value industries, the market faces genuine structural hurdles that must be addressed for the material to realize its full commercial potential.

-

High Production Costs and Demanding Manufacturing Processes: The reaction sintering and silicon infiltration process that gives SiSiC its superior properties is inherently complex and capital-intensive. Achieving consistent silicon infiltration throughout large or geometrically complex preforms requires precise control of furnace temperatures, atmosphere, and infiltration kinetics. Production costs for high-quality SiSiC components are approximately 30-40% higher than those for standard silicon carbide products, and the gap widens further when compared to more conventional structural materials like steel or aluminum. For cost-sensitive applications, this pricing premium remains a meaningful deterrent to adoption. Furthermore, production yields averaging 70-75% across most manufacturers mean that a significant proportion of raw material and processing effort does not translate to sellable product, further burdening the cost structure.

-

Competition from Alternative Advanced Materials: While SiSiC holds a clear performance edge in the most demanding applications, it faces determined competition from other advanced ceramics and composite materials in adjacent application spaces. Aluminum nitride ceramics, for instance, offer competitive thermal conductivity for certain thermal management applications at a lower cost point, making them attractive where the full performance envelope of SiSiC is not strictly required. Sintered silicon carbide, alumina, and various metal matrix composites each carve out segments of the broader advanced materials market. For SiSiC producers, this means that market development requires not just excellent product quality but also a compelling, well-communicated value proposition that justifies the premium over these alternatives in the eyes of procurement engineers and specification committees.

Critical Market Challenges Requiring Innovation

Beyond the structural restraints, the SiSiC market contends with a set of operational and supply chain challenges that require sustained technical and commercial innovation to overcome. Achieving consistent material quality, particularly in terms of residual free silicon content and microstructural homogeneity, across production runs of large components is a persistent technical challenge. Variations in these parameters can affect the final mechanical and thermal properties of components, creating quality assurance burdens for both producers and their customers in high-specification industries.

Supply chain resilience also presents a genuine concern. The specialized raw materials required for SiSiC production - particularly high-purity silicon carbide powder and electronic-grade silicon - are sourced from a relatively limited number of suppliers globally. During periods of peak demand, lead times for these critical inputs can extend significantly, constraining producers' ability to respond to customer requirements quickly. This dependency creates a layer of economic and operational uncertainty that the industry is actively working to mitigate through supplier diversification and longer-term procurement agreements.

Vast Market Opportunities on the Horizon

-

5G Infrastructure and Next-Generation Communications: The ongoing global rollout of 5G networks and the early-stage development of next-generation communication infrastructure present a meaningful emerging opportunity for SiSiC. RF power amplifiers and base station components operating at high power densities generate substantial heat that must be managed efficiently to maintain signal integrity and equipment longevity. SiSiC's combination of high thermal conductivity and excellent dimensional stability under thermal load makes it a strong candidate material for heat spreaders and structural components in these systems. As network equipment providers push the boundaries of power density in pursuit of higher data throughput, the performance requirements will increasingly favor advanced ceramic solutions over conventional metallic alternatives.

-

Advanced Manufacturing and Automation Systems: The broader global trend toward factory automation, precision robotics, and advanced machine tool technology is creating growing demand for structural materials that can deliver superior stiffness and thermal stability in high-speed, high-precision production environments. Machine tool tables, linear guides, and structural frames fabricated from SiSiC offer a combination of high specific stiffness and thermal neutrality that enables manufacturers to achieve tighter machining tolerances and better surface finishes, directly translating to higher-quality finished products. As manufacturers in Asia, Europe, and North America invest in upgrading their production capabilities, the business case for SiSiC structural components in precision machinery becomes increasingly compelling.

-

Strategic Industry Partnerships Accelerating Commercialization: One of the more encouraging recent trends in the SiSiC market has been the formation of strategic collaborations between material producers and major end-user industries. These partnerships, designed to co-develop application-specific component solutions, are proving effective at accelerating the qualification and adoption of SiSiC in new applications. By working closely with semiconductor equipment manufacturers, photovoltaic system integrators, and aerospace prime contractors, SiSiC producers can tailor material compositions and component geometries to specific performance requirements while simultaneously building the customer confidence and long-term supply relationships that underpin sustainable commercial growth.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The SiSiC market is segmented into Powder and Blocky form factors. Blocky SiSiC currently leads the market as the primary starting material for machining complex, high-precision finished components. Producers of semiconductor equipment components, machine tool structures, and mirror substrates overwhelmingly prefer the blocky form because its structural integrity and compositional consistency are essential for achieving the tight dimensional tolerances that end-use applications demand. Powder forms, while representing a smaller share, serve important niche roles in specialized manufacturing processes and composite material formulations where the precise blending of SiSiC with other materials is required.

By Application:

Application segments within the SiSiC market include Machine Tool Tables, Mirror Substrates, Precision Devices, and others. The Precision Device segment is a highly significant and rapidly growing area, driven by the material's exceptional dimensional stability and thermal neutrality. Components for semiconductor manufacturing equipment, high-precision scientific instrumentation, and advanced positioning systems - all of which demand minimal thermal expansion and superior wear resistance over long service lives - are placing SiSiC at the center of precision engineering. Machine Tool Tables represent a well-established, steady demand segment, while Mirror Substrates for space and defense optical systems, though smaller in volume, command premium pricing and represent a technically demanding application where SiSiC faces limited credible competition.

By End-User Industry:

The end-user landscape for SiSiC spans Semiconductor Manufacturing, Advanced Machinery and Automation, and Aerospace and Defense. Semiconductor Manufacturing stands as the most critical and dynamic end-user segment, generating relentless demand for high-purity, dimensionally stable components that can survive the plasma-rich, thermally intense environments of modern fabrication processes. The ongoing global push to expand semiconductor production capacity, accelerated by supply chain resilience initiatives in the United States, Europe, and Asia, is creating a sustained uplift in demand for the precision ceramic components that make advanced chip fabrication possible. Advanced Machinery and Automation represents a broader and more volume-driven segment, while Aerospace and Defense provides a premium, specification-driven market where SiSiC's unique properties command substantial value.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307057/siliconinfiltrated-silicon-carbide-market

Competitive Landscape:

The global Silicon-Infiltrated Silicon Carbide market features a concentrated competitive structure, with established producers from Japan, Germany, and the United States commanding the high-performance, high-value segments of the industry. TOTO Ltd. (Japan) and CeramTec GmbH (Germany) currently represent the market's leading positions, backed by decades of accumulated expertise in advanced ceramic engineering, proprietary reaction sintering processes, and deeply embedded relationships with semiconductor and aerospace end-users. Their dominance is sustained by extensive intellectual property portfolios, rigorous quality management systems, and production capabilities that consistently meet the most demanding material specifications. At the same time, emerging producers from China, supported by government industrial policy and a rapidly modernizing domestic manufacturing base, are increasingly competitive in mid-tier applications and are actively working to close the technical gap in higher-specification product categories.

List of Key Silicon-Infiltrated Silicon Carbide Companies Profiled:

-

TOTO Ltd. (Japan)

-

CeramTec GmbH (Germany)

-

Kyocera Corporation (Japan)

-

CoorsTek Inc. (USA)

-

Saint-Gobain Group (France)

-

Schunk Carbon Technology (Germany)

-

Morgan Advanced Materials (UK)

-

Entegris Inc. (USA)

-

Japan Fine Ceramics Co. (Japan)

-

Carborundum Universal Limited (India)

The competitive strategy across the SiSiC landscape is overwhelmingly centered on sustained R&D investment to refine material purity, reduce residual free silicon content, and improve manufacturing yields, alongside the cultivation of deep, long-term collaborative relationships with key end-user industries. Producers who can demonstrate consistent material performance at scale and offer application engineering support to their customers are best positioned to capture the growing value that this market is generating.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia (Japan & China): Asia is the undisputed epicenter of the global SiSiC market, combining Japan's world-class technological leadership with China's formidable and rapidly growing industrial scale. Japan's contribution is anchored by globally recognized producers like TOTO and Kyocera, whose precision reaction sintering expertise sets the international benchmark for material quality in the most demanding applications. China, meanwhile, is experiencing rapid market expansion fueled by national policies promoting high-tech manufacturing self-sufficiency and the explosive growth of domestic semiconductor, photovoltaic, and new energy vehicle industries. Together, these two markets define the pace and direction of global SiSiC industry development, making Asia the primary engine of both supply and demand growth.

-

Europe: Europe represents a mature, well-established market for Silicon-Infiltrated Silicon Carbide, underpinned by a strong industrial tradition in precision engineering, machine tool manufacturing, and high-performance automotive and aerospace production. Germany, France, and the Benelux region are home to several of the world's leading SiSiC producers and a dense concentration of high-specification end-users. European demand is characterized by an emphasis on quality, long component service life, and materials that support energy efficiency and sustainability goals - all attributes that play to SiSiC's strengths. While the region faces competitive pricing pressure from Asian producers in volume-driven application segments, it retains a strong position in premium and technically complex applications where material certification and supplier reliability are paramount.

-

North America: The North American market, centered on the United States, is technology-driven and closely tied to the fortunes of the domestic semiconductor equipment, aerospace, and defense industries. Substantial government investment in domestic semiconductor manufacturing capacity, accelerated by supply chain resilience legislation, is creating a growing and sustained demand for the high-performance ceramic components that advanced fabrication equipment requires. While North America does not host the same concentration of SiSiC producers as Asia or Europe, specialized ceramic suppliers and strong R&D-oriented end-users create a healthy market dynamic. The region's focus on next-generation aerospace and defense systems further supports premium demand for SiSiC in optical and structural applications.

-

South America and Middle East & Africa: These regions currently represent smaller segments of the global SiSiC market, with demand driven primarily by industrial activity in mining, heavy machinery, and oil and gas - sectors where the material's corrosion resistance and mechanical durability are valued. Growth in these markets is gradual and closely tied to broader industrial development trajectories. For global SiSiC producers, South America and MEA represent longer-term opportunities rather than near-term volume drivers, with market penetration largely dependent on import relationships with established suppliers from Asia, Europe, and North America.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307057/siliconinfiltrated-silicon-carbide-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307057/siliconinfiltrated-silicon-carbide-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/