Precision Liquid-Cooled GPU Server Market, Trends, Business Strategies 2026-2034

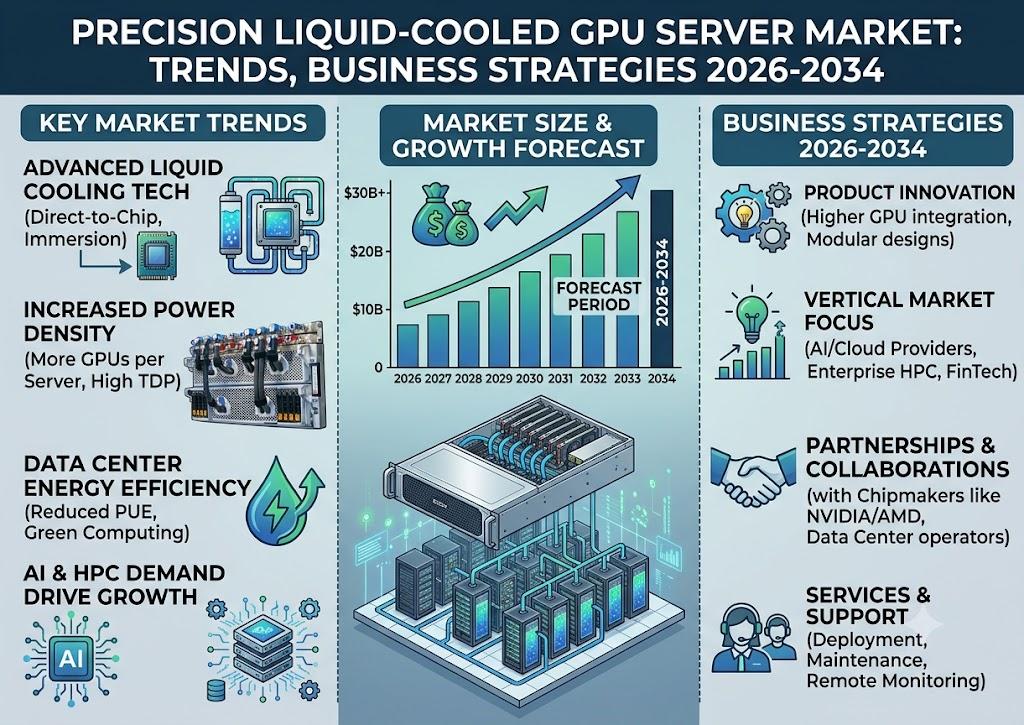

The global Precision Liquid-Cooled GPU Server Market, valued at approximately USD 239 million in 2025, is on a trajectory of significant expansion, projected to reach USD 367 million by 2034. This growth, representing a compound annual growth rate (CAGR) of 6.5%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the pivotal role of precision liquid‑cooling architectures in delivering the thermal stability required for today’s most demanding artificial‑intelligence (AI) and high‑performance‑computing (HPC) workloads.

Precision liquid‑cooled GPU servers combine advanced heat‑extraction technologies with high‑density graphics processing units to maintain GPU junction temperatures within ±0.1 °C under sustained heavy loads. By eliminating the thermal bottlenecks of traditional air‑cooled designs, these systems maximize computational throughput, extend hardware longevity, and reduce total cost of ownership for hyperscale data centers, cloud service providers, and research institutions alike.

Download FREE Sample Report:

Precision Liquid-Cooled GPU Server Market - View in Detailed Research Report

AI‑Driven Data Center Demand

The acceleration of AI model training and inference across a broad spectrum of industries – from autonomous vehicles to drug discovery – is the primary catalyst for market expansion. Large language models (LLMs) now regularly require clusters of eight‑GPU or larger servers operating at sustained 90 % utilization. In such environments, even a modest rise in GPU temperature can trigger throttling, leading to lost compute cycles and increased energy consumption. Precision liquid cooling eliminates this risk by directly channeling heat away from the GPU die via cold plates, immersed fluid loops, or spray‑based systems, thereby maintaining optimal performance while cutting power draw by up to 30 % compared with air‑cooled equivalents.

Semiconductor Industry Expansion: The Core Growth Engine

Semiconductor manufacturers continue to push the envelope on GPU performance, packing more transistors into smaller footprints and raising the thermal design power (TDP) of each die. The global semiconductor fabrication market is projected to exceed $120 billion annually, creating a direct demand for ancillary thermal‑management solutions. NVIDIA, AMD, and Intel, as the three dominant GPU and accelerator vendors, are actively collaborating with server OEMs to integrate liquid‑cooling interfaces at the silicon level, further entrenching the need for precision cooling across the ecosystem.

“The convergence of ever‑higher GPU densities and the global shift toward AI‑centric workloads has transformed precision liquid cooling from a niche technology into a strategic commodity,” the report states. “Regions with concentrated semiconductor fabs and AI research hubs, particularly North America and Asia‑Pacific, are experiencing the most rapid adoption curves.”

Read Full Report: https://semiconductorinsight.com/report/precision-liquid-cooled-gpu-server-market/

Market Segmentation: Technology and End‑User Focus

The report provides a granular segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Type

- Cold Plate Liquid Cooling

- Immersed Liquid Cooling

- Spray Liquid Cooling

By Application

- Electricity

- Telecommunications

- Finance

- Government

By End User

- Hyperscale Data Centers

- Cloud Service Providers

- Enterprise Data Centers

- Research & Academic Institutions

By GPU Configuration

- 4‑GPU Servers

- 8‑GPU Servers

- 16‑GPU & Above Servers

By Deployment Mode

- On‑Premises Deployment

- Colocation Deployment

- Edge Deployment

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=117516

Competitive Landscape: Key Players and Strategic Focus

COMPETITIVE LANDSCAPE

Key Industry Players

Precision Liquid-Cooled GPU Server Market - Competitive Intelligence & Leading Manufacturer Profiles

The global Precision Liquid-Cooled GPU Server market, valued at approximately USD 239 million in 2025 and projected to reach USD 367 million by 2034 at a CAGR of 6.5%, is characterized by an intensely competitive landscape dominated by a blend of semiconductor giants, server OEMs, and specialized thermal management innovators. NVIDIA commands a pivotal position in this ecosystem, leveraging its GPU architecture leadership to influence the design and deployment of liquid‑cooled server configurations optimized for AI, high‑performance computing, and data‑center workloads. Intel and AMD further anchor the competitive field through their processor and accelerator portfolios, enabling precision liquid‑cooled 8‑GPU server configurations that maximize thermal efficiency and computational throughput for enterprise‑grade AI applications across finance, government, telecommunications, and energy sectors. The top five global players collectively accounted for a significant share of total market revenue in 2025, underscoring the consolidated nature of this high‑growth segment.

Beyond the dominant semiconductor and server infrastructure players, the Precision Liquid-Cooled GPU Server market features a robust set of niche and regionally significant competitors. Inspur Information has emerged as a formidable force in the Asia‑Pacific region, particularly in China, offering purpose‑built liquid‑cooled GPU server platforms targeting hyperscale data centers and national AI infrastructure programs. Zhongke Shuguang (Sugon) also maintains a strong domestic presence in China, delivering indigenously developed liquid‑cooled HPC and AI servers aligned with national technology initiatives. Iceotope Technologies distinguishes itself through its precision immersion and chassis‑level liquid cooling innovations, catering to next‑generation edge and enterprise deployments. Meanwhile, Qualcomm and ARM contribute to the competitive dynamics through their energy‑efficient processor architectures increasingly adopted within alternative GPU server configurations. The market's segmentation across Cold Plate Liquid Cooling, Immersed Liquid Cooling, and Spray Liquid Cooling technologies further fuels competitive differentiation, as manufacturers race to optimize thermal performance, total cost of ownership, and deployment flexibility across global data‑center environments.

These firms are accelerating product roadmaps that incorporate IoT‑enabled thermal analytics, AI‑driven predictive maintenance, and modular liquid‑cooling kits designed for rapid retro‑fit in existing rack environments. Geographic expansion into high‑growth regions such as Southeast Asia and the Middle East is also a common strategic thrust.

Emerging Opportunities in Edge AI and Renewable Energy Computing

Beyond traditional data‑center demand, the report highlights emerging opportunities in edge AI, autonomous systems, and renewable‑energy‑focused data‑processing clusters. Edge deployments require compact, vibration‑tolerant cooling solutions that can operate in harsh environments without sacrificing thermal performance. Precision liquid cooling, especially spray‑based designs, is uniquely positioned to meet those constraints, fostering a nascent but rapidly scaling market segment.

In parallel, the surge in renewable‑energy forecasting and smart‑grid analytics is driving new workloads that rely on GPU‑accelerated simulations. These workloads generate sustained high‑heat fluxes, making liquid‑cooling a prerequisite for maintaining model accuracy and computational efficiency.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Precision Liquid‑Cooled GPU Server markets from 2025–2034. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Segment Analysis

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

Cold Plate Liquid Cooling holds the leading position in the Precision Liquid‑Cooled GPU Server market owing to its mature engineering design and broad compatibility with existing data‑center infrastructure.

|

| By Application |

|

Telecommunications emerges as the leading application segment, driven by the rapid expansion of AI‑driven network optimization, edge intelligence, and next‑generation wireless infrastructure globally.

|

| By End User |

|

Hyperscale Data Centers dominate the end‑user landscape for Precision Liquid‑Cooled GPU Servers, as these facilities operate at extreme compute densities that render traditional air‑cooled architectures operationally inefficient and economically unsustainable.

|

| By GPU Configuration |

|

8‑GPU Servers represent the leading configuration segment, widely recognized as the industry benchmark for balancing computational throughput, thermal management complexity, and rack‑space efficiency in AI‑intensive deployments.

|

| By Deployment Mode |

|

On‑Premises Deployment leads the deployment mode segment, as large enterprises, government bodies, and research organizations prioritize direct control over their GPU server infrastructure for data sovereignty, security compliance, and workload customization purposes.

|

Regional Analysis: Precision Liquid‑Cooled GPU Server Market

Regional Analysis: Precision Liquid‑Cooled GPU Server Market

North America's precision liquid‑cooled GPU server market is propelled by surging investment in artificial intelligence infrastructure and high‑performance computing facilities. Leading technology corporations are constructing dedicated AI campuses where GPU‑intensive workloads necessitate sophisticated liquid cooling architectures. This wave of buildout is setting new benchmarks for thermal efficiency and compute density across the region.

Regulatory pressure and corporate sustainability commitments are compelling North American data center operators to transition from traditional air‑cooled systems to precision liquid‑cooled GPU server solutions. Green data center certifications and power usage effectiveness targets are creating strong business cases for liquid cooling adoption, particularly among enterprises seeking to reduce their operational carbon footprints without sacrificing computational performance.

The presence of globally dominant hyperscalers and cloud service providers has made North America a critical testing ground for next‑generation precision liquid‑cooled GPU server deployments. These organizations are pioneering custom liquid cooling form factors, collaborating closely with hardware manufacturers to develop proprietary solutions that maximize GPU utilization and minimize energy waste at unprecedented scale.

North America's robust network of original equipment manufacturers, thermal solution specialists, and system integrators provides a decisive competitive advantage. This ecosystem accelerates the commercialization of innovative precision liquid‑cooled GPU server technologies, enabling rapid customization and deployment across diverse verticals including financial services, healthcare AI, autonomous vehicle development, and national security applications.

Europe

Europe represents a strategically significant region in the global precision liquid‑cooled GPU server market, characterized by strong regulatory frameworks and a growing commitment to digital sovereignty. The European Union's ambitious programs around AI competitiveness, including investments in pan‑European supercomputing infrastructure, are creating substantial demand for energy‑efficient GPU server thermal management solutions. Countries such as Germany, France, the Netherlands, and the Nordic states are at the forefront of this expansion, with the latter leveraging naturally cooler climates to optimize liquid cooling system efficiency. Stringent data privacy regulations are simultaneously driving the development of localized, sovereign cloud infrastructure that requires advanced GPU server solutions. European enterprises are increasingly prioritizing Total Cost of Ownership and environmental compliance, making precision liquid cooling an attractive proposition. The region's focus on green computing aligns seamlessly with the inherent energy efficiency advantages of liquid‑cooled GPU server architectures, positioning Europe as a high‑value growth market through the forecast period.

Asia‑Pacific

Asia‑Pacific is emerging as one of the fastest‑evolving markets for precision liquid‑cooled GPU servers, fueled by an extraordinary pace of digital transformation across China, Japan, South Korea, India, and Southeast Asia. China's national AI development strategy and the proliferation of domestic cloud giants are generating massive demand for high‑density GPU computing infrastructure, with liquid cooling becoming a necessity rather than an option. Japan and South Korea bring deeply rooted semiconductor expertise and a culture of technological precision, both of which are accelerating the localization and refinement of liquid‑cooled GPU server solutions. India is experiencing a rapid influx of hyperscale data center investments, driven by expanding digital services and government‑led AI initiatives. The diversity of use cases across the region - from manufacturing automation to financial analytics and consumer AI - ensures that Asia‑Pacific will remain a critical engine of growth for the precision liquid‑cooled GPU server market well into the 2030s.

South America

South America occupies an emerging position in the global precision liquid‑cooled GPU server market, with Brazil serving as the primary demand hub. The country's expanding cloud infrastructure sector, coupled with growing interest in AI‑powered applications across agribusiness, banking, and e‑commerce, is gradually driving awareness of advanced GPU server thermal management requirements. While the region has historically trailed in data‑center maturity, strategic investments by international cloud providers are establishing world‑class facilities that increasingly incorporate liquid cooling technologies. Chile and Colombia are also gaining attention as promising data‑center destinations due to their favorable geopolitical stability and renewable energy access. Market growth across South America is expected to gain momentum as digital literacy improves, regulatory environments mature, and local enterprises begin recognizing the long‑term operational and sustainability benefits offered by precision liquid‑cooled GPU server solutions within their computing strategies.

Middle East & Africa

The Middle East and Africa region is at an early but accelerating stage of engagement with the precision liquid‑cooled GPU server market. Gulf Cooperation Council nations - particularly the United Arab Emirates and Saudi Arabia - are channeling significant sovereign wealth into smart city initiatives, national AI strategies, and large‑scale data‑center construction projects that increasingly demand high‑performance, thermally efficient GPU infrastructure. The region's extreme ambient temperatures make precision liquid cooling not merely advantageous but operationally essential, creating a compelling natural driver for adoption. Africa, led by South Africa, Nigeria, and Kenya, is witnessing an expanding data‑center investment wave as mobile‑first digital economies grow rapidly. While challenges related to skilled workforce availability and infrastructure readiness persist, international partnerships and technology transfer agreements are helping bridge gaps. Over the forecast period, the Middle East and Africa are positioned to transition from nascent adopters to meaningful contributors in the global precision liquid‑cooled GPU server market landscape.

Get Full Report Here:

Precision Liquid‑Cooled GPU Server Market, Trends, Business Strategies 2026‑2034 - View in Detailed Research Report

click here to visit more insightful Reports

https://semiconductorinsight.com/report/global-noncontact-level-sensors-market/embed/

https://semiconductorinsight.com/blog/tag/future-of-the-printed-circuit-board-market-growth/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us