Consumer Electronics Printed Circuit Board Market, Emerging Trends, Technological Advancements, and Business Strategies 2025-2032

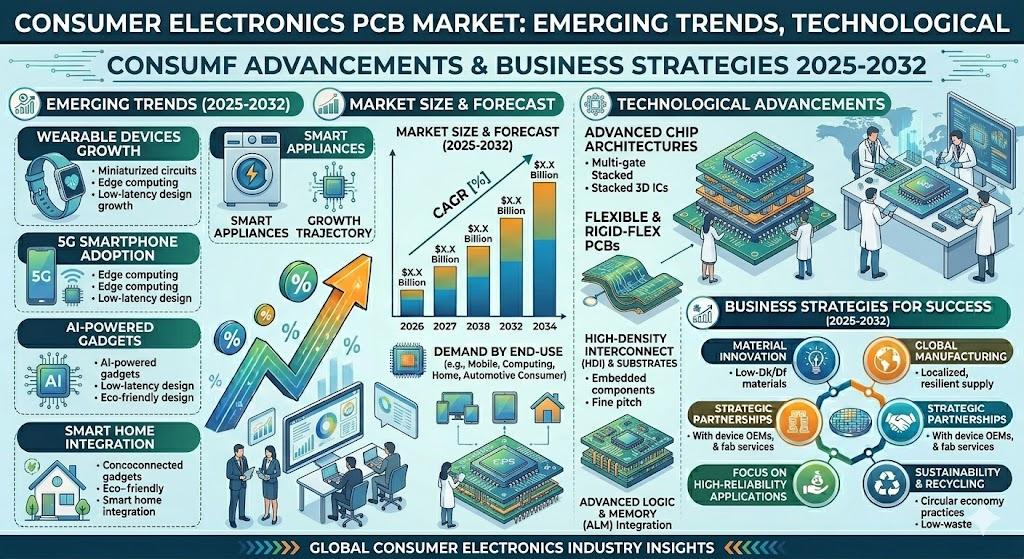

Consumer Electronics Printed Circuit Board (PCB) Market, valued at a robust figure in 2024, is poised for decisive expansion, with industry analysts forecasting continued acceleration through 2032. This momentum is driven by the relentless miniaturization of consumer devices, the surge in wearable technology adoption, and the escalating demand for high‑performance, multi‑layer boards in IoT and 5G‑enabled products. The latest report from Semiconductor Insight provides a granular view of the forces reshaping the PCB landscape and outlines the strategic pathways that leading manufacturers are pursuing to capture emerging growth.

Printed circuit boards are the foundational platform for virtually every electronic device, from earbuds and smart watches to tablets and home appliances. As consumer expectations shift toward thinner form factors, longer battery life, and richer functionality, PCB manufacturers are compelled to deliver ever‑higher density interconnects, flexible substrates, and resilient materials-all while navigating tighter environmental regulations and supply‑chain volatility.

Download FREE Sample Report:

Consumer Electronics Printed Circuit Board Market - View in Detailed Research Report

Key Growth Drivers

The report identifies several intertwined catalysts fueling market expansion. First, the proliferation of wearable devices-estimated to exceed 1.5 billion units worldwide by 2025-demands ultra‑thin, flexible PCBs that can conform to curved surfaces without compromising signal integrity. Second, the rapid rollout of 5G networks is stimulating demand for high‑frequency, low‑loss substrates, especially in antenna modules and RF front‑end components. Third, the rise of smart home ecosystems and connected appliances is driving a surge in multi‑layer board orders as manufacturers embed more sensors and communication modules into a single footprint.

Geographically, the Asia‑Pacific region remains the pre‑eminent hub for PCB fabrication, contributing over 70 % of global output. The concentration of electronics assembly plants in China, Taiwan, and South Korea equips the region with unparalleled scale advantages, while cost‑competitive labor and mature supply chains keep unit costs low. Concurrently, North America’s share of high‑value, high‑density board production is expanding, propelled by strong R&D pipelines in Silicon Valley and strategic investments in advanced manufacturing capabilities.

In parallel, regulatory pressures are reshaping material selection. Stringent RoHS and REACH directives are accelerating the shift toward halogen‑free and lead‑free laminates, prompting manufacturers to prioritize FR‑4 variants and explore emerging polyimide and rigid‑flex solutions that meet both performance and compliance criteria.

Competitive Landscape

Key Industry Players

Market Leaders Accelerate Product Innovation to Capture Growth in Evolving PCB Sector

The global Consumer Electronics Printed Circuit Board (PCB) market exhibits a fragmented competitive landscape, with established multinational corporations competing alongside agile regional players. Leading companies like AT&S and Sumitomo Electric Industries dominate the market through their technological expertise in high‑density interconnect (HDI) PCBs and flexible circuits, which are increasingly demanded for compact wearable devices and advanced tablets. These players collectively accounted for approximately 28% of the global PCB revenue in 2024.

Asian manufacturers such as Unimicron Technology Corporation and Shenzhen Kinwong Electronic are expanding their influence through cost‑competitive mass production capabilities. Their growth is further propelled by the concentration of electronics manufacturing in China and Southeast Asia, where approximately 68% of global consumer electronics are assembled.

Meanwhile, European and American players like Wurth Elektronik and Amphenol are differentiating through specialized PCB solutions for premium appliances and mission‑critical computer components. These companies are investing heavily in Industry 4.0 automation and sustainable manufacturing processes to maintain margins while meeting stringent environmental regulations.

Recent developments indicate an industry shift toward organic substrate PCBs and embedded component technologies, with multiple players announcing R&D partnerships during 2023‑2024. Nippon Mektron's recent collaboration with a major semiconductor firm to develop chip‑embedded PCBs exemplifies this trend toward higher integration.

These companies are focusing on technological advancements such as integration of IoT‑enabled predictive maintenance, high‑frequency substrate engineering, and geographic expansion into high‑growth regions like India and Southeast Asia to capture emerging opportunities.

Segment Analysis:

By Type

Multi‑Layer Printed Circuit Board Segment Dominates Due to Increasing Demand for High‑Performance Electronics

The market is segmented based on type into:

-

Single Layer Printed Circuit Board

-

Double Layer Printed Circuit Board

-

Multi‑Layer Printed Circuit Board

By Application

Computers and Tablets Segment Leads Owing to Expanding Digitalization Trends

The market is segmented based on application into:

-

Ear Buds

-

Dishwashers

-

Radios

-

Tablets

-

Computers

-

Wearable Devices

By Material

FR‑4 Segment Holds Major Share for Its Excellent Mechanical and Electrical Properties

The market is segmented based on material into:

-

FR‑4

-

Polyimide

-

Rigid‑Flex

-

Others

By End User

OEMs Lead in Market Adoption for Direct Manufacturing Requirements

The market is segmented based on end user into:

-

Original Equipment Manufacturers (OEMs)

-

Contract Manufacturers

-

Electric Component Suppliers

Regional Analysis: Consumer Electronics Printed Circuit Board Market

North America

The North American market is driven by strong demand for high‑performance multi‑layer PCBs in advanced consumer electronics such as wearables, IoT devices, and 5G‑enabled products. The U.S., accounting for over 65% of the regional market share, leads in innovation with companies like **Amphenol** and **Summit Interconnect** focusing on miniaturization and flexible PCB solutions. However, supply chain disruptions and rising material costs pose challenges, reflecting broader industry trends. Sustainability initiatives are gaining traction, with manufacturers exploring halogen‑free and lead‑free PCB materials to comply with **EPA and RoHS regulations**.

Europe

Europe’s market emphasizes **eco‑friendly PCB manufacturing**, aligning with the **EU Circular Economy Action Plan**. Germany and France dominate, leveraging their automotive and industrial electronics sectors to drive demand for **high‑reliability PCBs**. The region shows increasing adoption of **HDI (High‑Density Interconnect) boards** for compact devices, though growth is tempered by energy cost volatility and reliance on Asian suppliers for raw materials. Companies like **AT&S** and **Würth Elektronik** are investing in automation to offset labor costs, while **REACH compliance** remains a critical factor for PCB material selection.

Asia‑Pacific

As the **largest PCB production hub globally**, the Asia‑Pacific region (led by China, Japan, and South Korea) contributes **over 70% of global PCB output**. China’s **Shenzhen cluster** (home to **Shengyi Technology** and **Kinwong Electronic**) thrives on cost‑efficient mass production, while Japan excels in high‑end substrates for electronics giants like Sony and Panasonic. India emerges as a growth hotspot, with PCB demand rising **12% annually** due to smartphone and appliance manufacturing. However, overcapacity in China and trade tensions create pricing pressures, pushing suppliers to diversify into **automotive and medical electronics** segments.

South America

The region remains a niche market, with Brazil accounting for **50% of regional PCB demand**-primarily for **single‑layer and double‑layer boards** in consumer appliances. Limited local manufacturing forces reliance on imports, though tariffs on Chinese PCBs have spurred partnerships with **Mexican and U.S. suppliers**. Economic instability and currency fluctuations hinder investment in advanced PCB technologies, but the **gaming console and audio equipment markets** offer incremental growth opportunities.

Middle East & Africa

This emerging market focuses on **basic PCB applications** (radios, dishwashers) due to lower electronics penetration. The UAE and Turkey are key import hubs, with **15‑20% annual growth** in PCB demand linked to smart home device adoption. Lack of local fabrication units and dependence on Asian imports constrain market expansion, though **Saudi Arabia’s Vision 2030** is attracting PCB suppliers for regional electronics assembly. Low‑cost labor could eventually position North Africa as a PCB assembly destination, pending infrastructure improvements.

Emerging Opportunities

Beyond traditional consumer electronics, the report highlights several high‑growth verticals. The electric vehicle (EV) market’s shift toward in‑vehicle entertainment and infotainment systems is creating demand for lightweight, high‑frequency PCBs that can withstand automotive thermal cycles. Similarly, renewable‑energy equipment-particularly solar inverters and battery‑management systems-requires robust boards with excellent thermal performance. Industry 4.0 adoption is accelerating, with smart PCB factories leveraging AI‑driven yield optimization and digital twins to reduce defects by up to 30%.

Report Scope and Availability

The market research report delivers a comprehensive analysis of the global and regional Consumer Electronics PCB markets from 2025‑2032. It offers detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics, empowering decision‑makers to formulate data‑driven strategies.

Get Full Report Here:

Consumer Electronics Printed Circuit Board Market, Emerging Trends, Technological Advancements, and Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us