Internet Access Gateway Market, Trends, Business Strategies 2026-2034

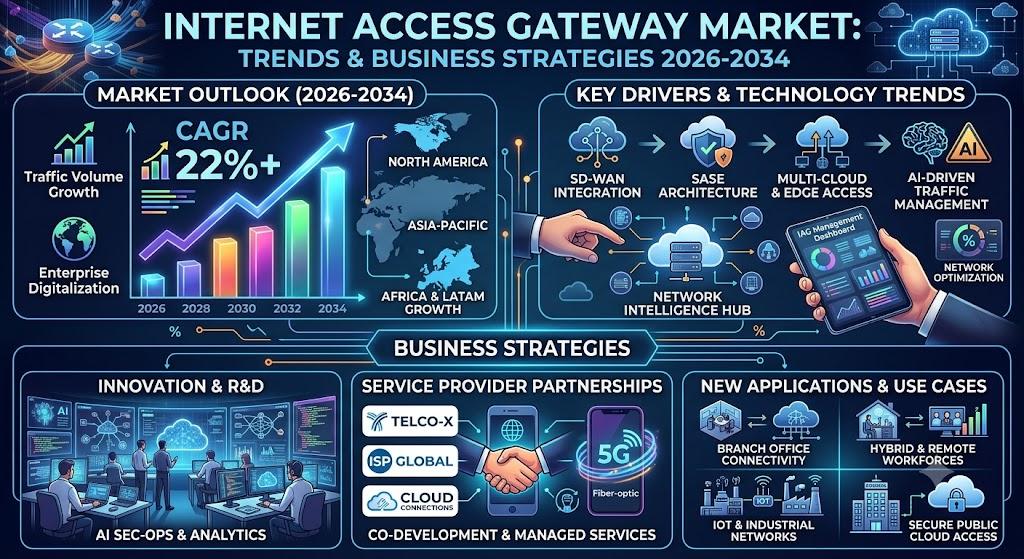

The global Internet Access Gateway Market, valued at a robust US$ 3,762 million in 2025, is on a trajectory of significant expansion, projected to reach US$ 5,793 million by 2034. This growth, representing a compound annual growth rate (CAGR) of 6.5%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the pivotal role of Internet Access Gateways (IAG) in enabling secure, reliable, and high‑performance connectivity for enterprises navigating the twin imperatives of digital transformation and escalating cyber‑threats.

Internet Access Gateways serve as the frontline defence for organisations that require unified control of inbound and outbound internet traffic, granular policy enforcement, and seamless integration with cloud‑based security services. By consolidating routing, firewall, and threat‑inspection functions into a single appliance-or a cloud‑delivered service-gateways minimise complexity, reduce latency, and improve overall network resilience. Their ability to blend traditional network security with modern zero‑trust principles makes them indispensable across a wide spectrum of verticals, from finance and healthcare to industrial automation.

Download FREE Sample Report:

Internet Access Gateway Market - View in Detailed Research Report

Digital‑First Enterprise Evolution: The Core Growth Engine

Several macro‑level forces are converging to accelerate demand for robust IAG solutions. The worldwide rollout of 5G and the maturation of LTE networks are expanding the pool of high‑speed cellular connections, prompting organisations-especially those with remote sites, oil‑field operations, or mobile workforces-to adopt Cellular Access Gateways for reliable back‑haul. Simultaneously, the rapid shift toward hybrid and multi‑cloud environments is driving enterprises to adopt Secure Access Service Edge (SASE) architectures, in which cloud‑native Internet Access Gateways provide the necessary policy enforcement at the edge. The rise of remote‑work models, spurred by the pandemic and now institutionalised as a strategic asset, further pushes organisations to secure internet traffic that traverses a distributed workforce, making cloud‑based gateway deployments a preferred choice.

Regulatory pressure adds another layer of urgency. Financial services, healthcare, and government entities are subject to increasingly strict data‑privacy and cybersecurity mandates (e.g., PCI‑DSS, HIPAA, CMMC). IAG platforms that embed advanced URL filtering, SSL/TLS inspection, and data‑loss‑prevention (DLP) capabilities enable these sectors to meet compliance requirements while maintaining business agility.

In addition, the explosion of Internet of Things (IoT) devices in manufacturing, logistics, and smart‑city applications creates unprecedented connectivity requirements. Gateways that can handle massive numbers of simultaneous connections, perform deep packet inspection at line rate, and support edge‑compute workloads are becoming baseline expectations for modern networks.

Read Full Report: https://semiconductorinsight.com/report/internet-access-gateway-market/

Market Segmentation: Types, Applications, and Deployment Modes

The report provides a granular segmentation analysis, illustrating how distinct sub‑segments contribute to overall market dynamics.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cellular Access Gateway is emerging as the dominant type in the Internet Access Gateway market, driven by the rapid global rollout of 4G LTE and 5G networks that demand robust and reliable cellular connectivity infrastructure.

|

| By Application |

|

Large Companies represent the leading application segment in the Internet Access Gateway market, as enterprise‑scale organizations face growing demands for centralized internet traffic management, advanced threat protection, and policy‑based access control across geographically dispersed networks.

|

| By End User |

|

BFSI stands out as the dominant end‑user vertical in the Internet Access Gateway market, given the sector's stringent regulatory compliance requirements, critical need for data privacy, and high vulnerability to cyber threats that necessitate robust internet access governance.

|

| By Deployment Mode |

|

Cloud‑Based Deployment is rapidly becoming the preferred mode of deployment for Internet Access Gateways, as organisations seek scalable, centrally managed, and cost‑effective alternatives to traditional hardware‑dependent gateway architectures.

|

| By Component |

|

Hardware remains the foundational and leading component segment within the Internet Access Gateway market, as purpose‑built physical appliances continue to deliver the high throughput, deterministic performance, and rugged reliability demanded by enterprise and industrial deployments.

|

COMPETITIVE LANDSCAPE

Key Industry Players

Internet Access Gateway Market - Competitive Dynamics, Leading Vendors, and Strategic Positioning

The global Internet Access Gateway (IAG) market is characterized by intense competition among a mix of established networking giants and specialized technology providers. Cisco continues to assert its dominance as the foremost player in this space, leveraging its comprehensive portfolio of enterprise‑grade gateway solutions, deep‑rooted channel partnerships, and sustained investment in secure access and SD‑WAN capabilities. Huawei and ZTE similarly command significant market presence, particularly across Asia‑Pacific and emerging economies, offering cost‑competitive yet feature‑rich IAG platforms tailored to both cellular and wireless access environments. Dell reinforces its competitive standing through integrated infrastructure offerings that bundle gateway functionality with broader enterprise IT ecosystems, while Siemens and Schneider Electric differentiate themselves by targeting industrial and operational technology (OT) segments, addressing the growing convergence of IT and OT networks. Together, the top five global players accounted for a substantial share of the market revenue in 2025, underscoring the oligopolistic nature of the upper tier of this industry.

Beyond the market leaders, a robust cohort of niche and regional players contributes meaningfully to the competitive fabric of the Internet Access Gateway market. Ubiquiti has carved out a loyal customer base among SMEs and value‑conscious enterprises by delivering scalable wireless access gateway solutions at accessible price points. Sangfor Technologies is gaining traction in the Asia‑Pacific region with its cybersecurity‑integrated gateway offerings. Advantech and ADLINK Technology serve industrial IoT and edge computing segments with ruggedized, application‑specific gateway hardware. Moxa is recognized for its reliable industrial networking devices, while Fujitsu brings enterprise‑class reliability and managed service capabilities to the market. Obvius (Leviton) and Alotcer address specialized verticals including energy management and remote IoT connectivity respectively. ABB rounds out the competitive landscape with its focus on smart infrastructure and industrial automation‑centric connectivity solutions. As the global IAG market is projected to grow from USD 3,762 million in 2025 to USD 5,793 million by 2034 at a CAGR of 6.5%, competition is expected to intensify, with vendors increasingly differentiating through security integration, cloud management, and edge intelligence capabilities.

List of Key Internet Access Gateway Companies Profiled

-

Huawei

-

Advantech

-

Siemens

-

Schneider Electric

-

Fujitsu

-

ZTE

-

ABB

-

ADLINK Technology

-

Moxa

-

Obvius (Leviton)

-

Alotcer

Get Full Report Here:

Internet Access Gateway Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

Regional Analysis: Internet Access Gateway Market

North American enterprises are aggressively modernising their IT infrastructure, driving sustained demand for advanced internet access gateway solutions. The proliferation of hybrid work models and multi‑cloud environments has made secure, scalable gateway deployments a strategic imperative. Organizations are prioritising platforms that offer seamless integration with existing security stacks, enabling more resilient and flexible network perimeters across distributed workforces.

Stringent data privacy regulations and sector‑specific compliance mandates in the United States and Canada are compelling organisations to invest in gateway technologies capable of enforcing policy‑driven access controls and comprehensive traffic inspection. Frameworks such as CMMC for defence contractors and HIPAA for healthcare providers are directly influencing purchasing decisions, with compliance readiness becoming a core feature criterion for internet access gateway platforms.

The region hosts a concentration of the world’s most influential internet access gateway vendors, fostering a competitive innovation environment. Ongoing research into AI‑driven threat detection, SASE architecture, and SD‑WAN integration is yielding next‑generation gateway solutions. Strategic acquisitions and partnerships among North American technology firms are accelerating product roadmaps and enabling vendors to deliver more comprehensive, end‑to‑end connectivity and security offerings to enterprise clients.

Beyond large enterprises, the small and medium‑sized business segment in North America is increasingly recognising the value of managed internet access gateway services. The expansion of managed service provider channels and cloud‑delivered gateway offerings has lowered the barrier to entry for SMBs, enabling them to access enterprise‑grade connectivity and security capabilities without the complexity of on‑premises hardware deployment or large in‑house IT teams.

Europe

Europe represents a highly significant and rapidly evolving market for internet access gateway solutions, characterised by a unique interplay of stringent regulatory requirements and accelerating enterprise digitalisation. The General Data Protection Regulation continues to exert considerable influence over how organisations design and deploy gateway architectures, particularly with respect to data residency, cross‑border traffic management, and user privacy. Western European nations including Germany, France, and the United Kingdom are at the forefront of adopting software‑defined gateway models, while Central and Eastern European markets are experiencing growing momentum driven by expanding digital economies and EU‑funded connectivity initiatives. The region's strong emphasis on sovereign cloud infrastructure and data localisation is shaping gateway procurement strategies, with many organisations favouring solutions that offer granular control over traffic routing and policy enforcement. European telecom operators are also playing an increasingly active role in bundling gateway functionality within broader managed network service portfolios, offering enterprises a more integrated path to secure internet access.

Asia‑Pacific

Asia‑Pacific is emerging as one of the fastest‑growing regions in the global internet access gateway market, propelled by explosive growth in digital connectivity, surging enterprise cloud adoption, and large‑scale government‑backed broadband infrastructure programmes. Countries such as China, India, Japan, South Korea, and Australia are each contributing distinct demand dynamics to the regional landscape. China's massive domestic technology ecosystem and stringent national cybersecurity regulations are driving the development of indigenously designed gateway solutions tailored to local compliance requirements. India's rapidly expanding digital economy, fueled by a burgeoning startup ecosystem and widespread mobile internet penetration, is creating robust demand for scalable and cost‑effective gateway platforms. Japan and South Korea, with their advanced industrial bases and early adoption of next‑generation networking technologies, continue to invest in high‑performance gateway infrastructure to support smart manufacturing and connected enterprise environments. Southeast Asia also presents compelling growth opportunities as digital transformation accelerates across financial services, retail, and public‑sector verticals.

South America

South America occupies a developing yet increasingly promising position within the global internet access gateway market. Brazil dominates regional demand, driven by its large enterprise base, expanding fintech sector, and ongoing efforts to modernise public‑sector IT infrastructure. The country's growing awareness of cybersecurity risks, amplified by a series of high‑profile data breaches, has prompted organisations to reassess their network perimeter strategies and invest in more robust gateway solutions. Other markets including Argentina, Chile, and Colombia are also witnessing gradual adoption of cloud‑delivered internet access gateway platforms, particularly among mid‑sized enterprises seeking to balance cost efficiency with improved security posture. However, economic volatility, currency fluctuations, and inconsistent regulatory frameworks continue to temper the pace of market expansion across parts of the region. Vendors that can offer flexible pricing models and localized support capabilities are best positioned to capture emerging opportunities as South American enterprises prioritise digital resilience.

Middle East & Africa

The Middle East and Africa region presents a nuanced and evolving landscape for the internet access gateway market, with considerable variation in market maturity across sub‑regions. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are leading regional adoption through ambitious smart‑city initiatives, large‑scale digital government programmes, and substantial investment in cybersecurity infrastructure. These markets are increasingly deploying advanced gateway solutions as part of broader national digitalisation strategies that emphasise secure and high‑performance connectivity. In contrast, Sub‑Saharan Africa, while earlier in its digital transformation journey, is experiencing growing momentum as mobile broadband penetration expands and enterprise connectivity needs intensify. The rollout of terrestrial fibre networks and the increasing availability of satellite‑based internet services are progressively creating the foundational connectivity layer necessary to support gateway solution adoption. Public‑sector investment and multilateral development funding are expected to play a catalytic role in accelerating market development across underserved African markets through the forecast period.

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us