CIS Probe Card Market, Trends, Business Strategies 2026-2034

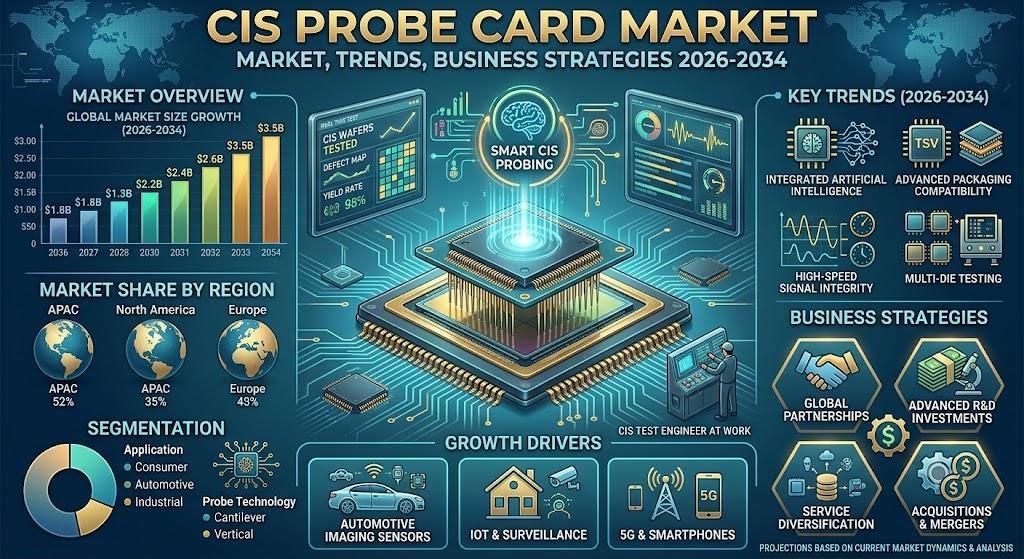

CIS Probe Card Market, valued at approximately USD 269 million in 2025, is on a robust growth trajectory and is projected to reach USD 434 million by 2032, representing a compound annual growth rate (CAGR) of 7.3%. This upward momentum is captured in a newly released comprehensive report by Semiconductor Insight. The study illuminates the pivotal role of CIS probe cards in enabling high‑precision wafer‑level testing of CMOS image sensors (CIS) that power smartphones, automotive cameras, medical imaging devices, and a growing suite of AI‑enabled vision systems.

CIS probe cards serve as the critical interface between test equipment and the delicate pads of an image sensor wafer. By delivering reliable electrical contact across thousands of micro‑pins, they ensure that each die meets stringent performance specifications before it proceeds to packaging. Their ability to support high‑pin‑count configurations, maintain planarity under thermal cycling, and accommodate emerging substrate materials such as ceramic and silicon makes them indispensable for modern semiconductor fab lines. As sensor resolution climbs and node geometries shrink, the demand for probe cards that can guarantee repeatable, low‑defect testing grows in lock‑step.

Download FREE Sample Report:

CIS Probe Card Market - View in Detailed Research Report

Semiconductor Industry Expansion: The Primary Growth Engine

The report identifies the explosive expansion of the global semiconductor ecosystem as the foremost catalyst for CIS probe card demand. CMOS image sensors now account for more than 70 % of the total camera market, and the semiconductor equipment sector is forecast to surpass USD 130 billion annually by 2030. This expansion fuels a surge in wafer‑testing throughput, prompting fabs to invest heavily in next‑generation probe card solutions that can keep pace with higher pin densities and tighter tolerances. The United States, South Korea, Japan, Taiwan, and China together host over 80 % of the world’s CIS production capacity, creating a concentrated demand base that directly influences probe‑card purchasing patterns.

“The concentration of CIS fab facilities in the Asia‑Pacific corridor, which alone consumes roughly three‑quarters of global probe‑card volumes, is a decisive factor behind the market’s rapid acceleration,” the report notes. With cumulative semiconductor fab investments projected to exceed USD 600 billion through 2030, the need for advanced testing infrastructure-including MEMS‑based probe cards capable of sub‑micron pitch alignment-will intensify, especially as automotive ADAS and 8K‑resolution imaging push sensor designs toward multi‑stacked architectures.

Read Full Report: https://semiconductorinsight.com/report/cis-probe-card-market/

Market Segmentation: Type, Application, End‑User, Substrate and Pin‑Count

The report delivers a granular segmentation that clarifies the market’s structural composition and highlights the most promising growth vectors. Detailed tables illustrate the distribution of probe‑card types, end‑user categories, substrate choices, and pin‑count classifications, enabling stakeholders to pinpoint strategic investment opportunities.

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

CIS MEMS Probe Card is the leading and fastest‑advancing segment within the type category, driven by its superior ability to meet the increasingly stringent demands of next‑generation CIS testing.

|

| By Application |

|

Consumer Electronics remains the dominant application segment for CIS probe cards, anchored by pervasive integration of image sensors across smartphones, tablets, laptops, and wearables.

|

| By End User |

|

Wafer Foundries and Semiconductor Manufacturers represent the primary end‑user base for CIS probe cards, given their central role in wafer‑level testing.

|

| By Substrate Material |

|

Ceramic‑Substrate CIS Probe Card holds the leading position within the substrate material segment, owing to its well‑established reliability and thermal performance in high‑precision testing.

|

| By Pin Count |

|

High‑Pin‑Count CIS Probe Card is the most strategically significant and technically demanding segment, reflecting the industry trend toward testing increasingly complex, high‑resolution sensors.

|

Competitive Landscape: Key Players and Strategic Focus

COMPETITIVE LANDSCAPE

Key Industry Players

CIS Probe Card Market – Competitive Dynamics, Key Manufacturers, and Strategic Positioning

The global CIS Probe Card market, valued at approximately USD 269 million in 2025 and projected to reach USD 434 million by 2032 at a CAGR of 7.3%, is characterized by a moderately consolidated competitive landscape dominated by a handful of technologically advanced players. FormFactor stands out as the leading global manufacturer, commanding a significant share of the market through its robust R&D capabilities, extensive product portfolio spanning cantilever and MEMS‑based probe card technologies, and deep integration with major semiconductor foundries and chip designers worldwide. Technoprobe S.p.A., headquartered in Italy, represents another dominant force, leveraging its precision engineering expertise and strong foothold in both European and Asia‑Pacific markets. Japanese firms such as Micronics Japan (MJC) and Japan Electronic Materials (JEM) continue to play a critical role in advancing probe card miniaturization and high‑density pin configurations, catering to the increasingly stringent testing requirements driven by shrinking semiconductor process nodes. These top‑tier players collectively benefit from economies of scale, proprietary manufacturing processes including photolithography and MEMS fabrication, and long‑term supply agreements with major CIS chipmakers, creating substantial barriers to entry for emerging competitors.

Beyond the market leaders, a dynamic tier of niche and regionally significant players is intensifying competition across specific application segments including consumer electronics, automotive imaging, medical imaging, and security and surveillance. MPI Corporation and Korea Instrument are recognized for their tailored solutions addressing medium‑ and high‑pin‑count probe card requirements, while Will Technology and STAr Technologies, Inc. have carved out strong positions in the Asia‑Pacific region with cost‑competitive offerings. Chinese manufacturers, including Shenzhen DGT, Sinowin, Suzhou Maxone Semiconductor, ZENFOCUS, Hongyi Advanced Technology, and ProbeLeader, are rapidly scaling their capabilities, driven by domestic semiconductor demand and government‑backed industrial development initiatives. Nidec SV Probe brings additional competitive pressure through its vertically integrated manufacturing model, and MemsFlex is gaining attention for its innovations in MEMS‑based probe card design. The competitive intensity is further amplified by the industry’s push toward ceramic and silicon substrate probe cards capable of supporting advanced wafer‑level testing, with average gross profit margins in the 26–29 % range reflecting the premium placed on precision, reliability, and customization across the supply chain.

List of Key CIS Probe Card Companies Profiled

-

MPI Corporation

-

Korea Instrument

-

Will Technology

-

STAr Technologies, Inc.

-

Shenzhen DGT

-

Sinowin

-

Nidec SV Probe

-

Su Zhou Maxone Semiconductor

-

ZENFOCUS

-

Hongyi Advanced Technology

-

ProbeLeader

-

MemsFlex

Emerging Opportunities in AI‑Vision, Automotive and Edge Computing

Beyond the traditional consumer‑electronics driver, the report highlights several high‑growth avenues that are reshaping the probe‑card landscape. The rapid rise of AI‑enabled vision systems in autonomous vehicles, smart cities, and industrial robotics is driving demand for ultra‑high‑resolution CIS that operate at multi‑megapixel scales. Such sensors require sophisticated wafer‑testing regimes capable of validating high‑speed data streams, low‑light performance, and on‑chip AI accelerators-an area where MEMS‑based probe cards have a distinct advantage.

In parallel, the automotive sector’s transition toward sensor‑centric ADAS and Level‑3/4 autonomous functions is expanding the addressable market for high‑pin‑count, high‑reliability probe cards. OEMs and Tier‑1 suppliers are investing heavily in in‑house testing capabilities, fostering partnerships with probe‑card vendors that can co‑develop customized solutions for rugged automotive‑grade CIS devices.

Edge‑computing deployments, especially in retail analytics, security surveillance, and smart‑home appliances, are also fueling demand for compact yet powerful image sensors. The proliferation of these edge devices accelerates the need for cost‑effective, medium‑pin‑count probe cards that can sustain large‑volume production while meeting strict quality standards.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional CIS Probe Card markets from 2025–2032. It provides detailed segmentation, market‑size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics, enabling readers to formulate informed strategic decisions.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Get Full Report Here:

CIS Probe Card Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us