DDR5 RDIMM Memory Module Market, Trends, Business Strategies 2026-2034

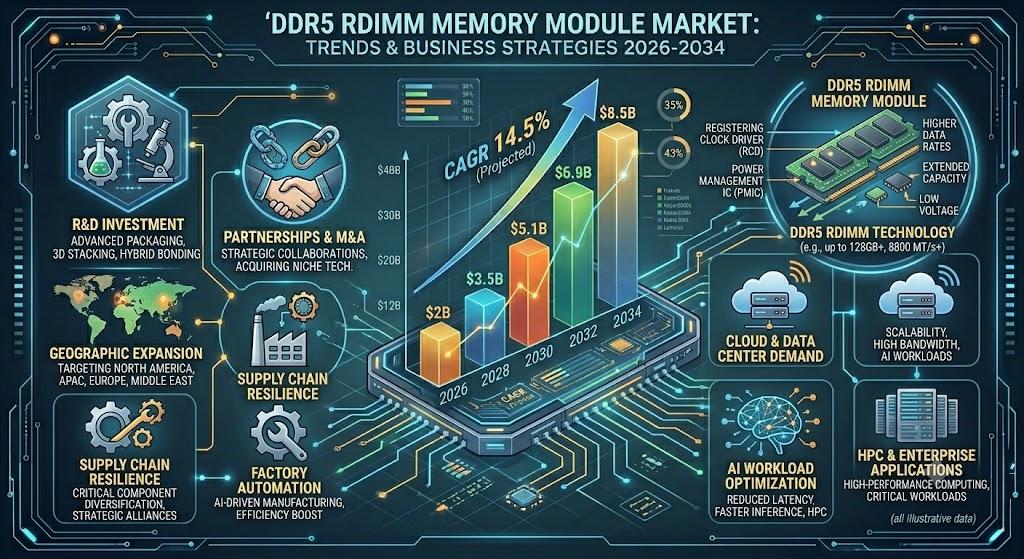

DDR5 RDIMM Memory Module market is experiencing a pronounced acceleration as enterprise and hyperscale data‑center operators replace legacy DDR4 platforms with DDR5‑enabled server architectures. Although precise monetary valuations remain proprietary, the consensus among industry analysts points to a sustained multi‑year expansion fueled by the convergence of artificial‑intelligence (AI) workloads, high‑performance computing (HPC) demands, and the rollout of next‑generation processor families such as Intel Sapphire Rapids and AMD EPYC Genoa, both of which mandate DDR5 memory.

DDR5 RDIMMs differentiate themselves through a suite of technical enhancements, including higher prefetch buffers, on‑module error‑correction codes (ECC), and the capability to support substantially larger capacities-typically 64 GB, 96 GB and 128 GB per module. These attributes translate into greater memory bandwidth, lower power consumption per gigabyte, and an improved capacity‑to‑density ratio, enabling server manufacturers and cloud service providers to achieve higher consolidation ratios within the same rack footprint while simultaneously curbing operational expenditures.

Download FREE Sample Report:

DDR5 RDIMM Memory Module Market - View in Detailed Research Report

Data‑Center & AI Workload Expansion: The Primary Growth Engine

The report identifies the explosive growth of AI‑driven services, generative‑AI platforms, real‑time analytics, and large‑scale model training as the dominant catalyst propelling DDR5 RDIMM demand. AI inference engines and in‑memory databases require sustained high‑throughput memory channels; DDR5 RDIMMs, with their native 4800 MT/s‑7200 MT/s speed grades, satisfy these requirements far better than DDR4 predecessors. Moreover, the migration to cloud‑native architectures has amplified the need for modular, scalable memory solutions that can be provisioned rapidly across geographically dispersed hyperscale facilities.

Base‑station communications for 5G networks are emerging as a noteworthy growth avenue. Telecommunications equipment-especially those supporting massive MIMO and edge‑computing functions-relies on server‑class compute nodes where DDR5 RDIMMs provide the deterministic latency and reliability needed for handling concurrent data streams.

Automotive and security‑monitoring segments, while currently representing niche volumes, are expected to gain traction as vehicles become increasingly autonomous and surveillance systems adopt AI‑enabled analytics at the edge. These markets demand ruggedized, extended‑temperature DDR5 RDIMMs that can endure harsh operating environments, a need already being addressed by specialized module manufacturers.

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

DDR5 RDIMM Memory Module Market - Competitive Dynamics and Leading Manufacturer Profiles

The global DDR5 RDIMM Memory Module market is characterized by intense competition among a select group of vertically integrated semiconductor giants and specialized memory module manufacturers. Samsung, SK Hynix, and Micron collectively dominate the market, leveraging their proprietary DRAM fabrication capabilities to maintain significant cost advantages and supply chain control. These three IDMs (Integrated Device Manufacturers) are the primary suppliers of DDR5 DRAM dies, which underpin virtually all DDR5 RDIMM production globally. Their technological leadership is evident in the rapid commercialization of high‑density DDR5 RDIMMs - particularly in the 64 GB, 96 GB, and 128 GB capacity segments - catering to the surging demand from hyperscale data centers, cloud service providers, and AI/ML workload infrastructure. The adoption of DDR5 RDIMM across servers and data centers remains the dominant application segment, driven by the platform transition to Intel Sapphire Rapids and AMD EPYC Genoa processor ecosystems, both of which mandate DDR5 memory architectures for next‑generation server deployments.

Beyond the top‑tier DRAM manufacturers, a robust ecosystem of specialized module makers and value‑added resellers competes vigorously in enterprise, embedded, industrial, and ruggedized application segments. Companies such as Kingston Technology, CORSAIR, and Adata serve high‑performance computing and workstation markets, while ATP Electronics, Innodisk, and SMART Modular Technologies focus on industrial‑grade, extended‑temperature, and mission‑critical deployments requiring stringent qualification standards. Netlist has carved a differentiated position through its patented memory technologies and licensing portfolio, while Apacer, Silicon Power, and Longsys compete primarily across Asia‑Pacific markets with cost‑competitive offerings. Emerging players such as Wuxi HippStor Technology are gaining traction in China’s rapidly expanding domestic server memory supply chain, reflecting broader industry trends toward regional supply diversification. Overall, the competitive landscape continues to evolve as manufacturers invest in RCD (Registering Clock Driver) design advancements, on‑module error correction, and power‑efficiency improvements to meet the escalating performance demands of modern server and data‑center infrastructur

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Higher‑Capacity Modules (64G and Above) are rapidly emerging as the dominant force in the DDR5 RDIMM Memory Module market, driven by the intensifying demands of modern enterprise computing environments.

|

| By Application |

|

Servers and Data Centers represent the most prominent and strategically critical application segment for DDR5 RDIMM Memory Modules, underpinned by a confluence of transformative technological and infrastructure trends.

|

| By End User |

|

Cloud Service Providers and Hyperscalers constitute the most influential end‑user segment, consistently driving large‑volume procurement of DDR5 RDIMM modules to support their ever‑expanding global infrastructure.

|

| By Speed Grade |

|

DDR5-4800 and DDR5-5600 currently serve as the foundational speed grades commanding the broadest installed base, while higher‑performance grades are gaining decisive momentum as platform and workload requirements evolve.

|

| By Channel |

|

OEM and Direct Enterprise Sales Channels dominate the DDR5 RDIMM distribution landscape, reflecting the highly specialized and volume‑intensive nature of memory module procurement in enterprise markets.

|

Regional Analysis: DDR5 RDIMM Memory Module Market

South Korea, home to global memory giants, plays a pivotal role in advancing DDR5 RDIMM technology innovation, while Taiwan’s robust motherboard and server OEM ecosystem ensures consistent downstream adoption. China’s expanding domestic data‑center build‑out, fueled by government‑backed digitalization initiatives and the growth of indigenous cloud service providers, further amplifies regional consumption. India is emerging as a noteworthy contributor as its IT infrastructure modernization accelerates. Collectively, Asia‑Pacific’s integrated supply‑chain advantages, cost competitiveness, and technology leadership position it as the most critical and fastest‑evolving geography in the global DDR5 RDIMM memory module market landscape through the 2026–2034 forecast period.

Asia‑Pacific’s vertically integrated semiconductor supply chain gives the region an unmatched competitive edge in the DDR5 RDIMM memory module market. From wafer fabrication to module assembly and testing, key regional players maintain tight control over production quality and cost efficiency. This integration minimizes lead times and supports rapid scalability in response to fluctuating global server demand cycles.

The explosive growth of hyperscale and colocation data centers across China, India, and Southeast Asia is a primary demand driver for DDR5 RDIMM modules in the region. Major cloud service providers are aggressively upgrading server infrastructure to accommodate AI inference, big data analytics, and enterprise workloads, each requiring the enhanced bandwidth and reliability that DDR5 RDIMM technology delivers.

Leading memory manufacturers headquartered in South Korea and Taiwan are channeling significant resources into next‑generation DDR5 RDIMM research and development. Innovations in die‑stacking, error correction, and power efficiency are being pioneered in the region, ensuring Asia‑Pacific maintains its technological leadership and shapes global product roadmaps in the DDR5 RDIMM memory module market well into the next decade.

Supportive government frameworks across Asia‑Pacific are accelerating DDR5 RDIMM adoption. China’s national semiconductor self‑sufficiency drive, India’s Digital India initiative, and South Korea’s strategic investment in advanced memory technology collectively create a favorable policy environment. These initiatives stimulate domestic procurement of high‑performance memory solutions and reduce reliance on external supply chains, reinforcing regional market momentum.

North America

North America represents a critically important geography in the DDR5 RDIMM memory module market, distinguished by its concentration of world‑leading hyperscale cloud operators, enterprise IT powerhouses, and cutting‑edge research institutions. The United States, in particular, is a major consumption hub, with hyperscalers and large enterprises rapidly transitioning server fleets to DDR5‑compatible platforms to support AI model training, high‑performance computing, and mission‑critical workloads. The region’s strong culture of early technology adoption ensures that DDR5 RDIMM modules achieve faster penetration into commercial data centers compared to many other markets. Canada also contributes through its growing data‑center corridor and expanding AI research ecosystem. While North America depends heavily on Asia‑Pacific for memory module manufacturing, its role as a technology standard‑setter and primary demand generator keeps it at the strategic forefront of the global DDR5 RDIMM memory module market through the forecast period.

Europe

Europe occupies a significant position in the DDR5 RDIMM memory module market, propelled by the region’s ambitious digital transformation agenda, expanding cloud infrastructure investments, and stringent data‑sovereignty regulations that incentivize domestic data‑center build‑outs. Germany, the United Kingdom, France, and the Netherlands serve as the primary hubs of enterprise server deployment and data‑center growth, each driving consistent demand for advanced DDR5 RDIMM solutions. The European Union’s focus on technological resilience and reducing dependency on non‑European supply chains has begun encouraging regional semiconductor ecosystem development, which may gradually influence the memory module supply landscape. Additionally, Europe’s robust automotive and industrial sectors are increasingly exploring high‑performance computing platforms that leverage DDR5 RDIMM technology for embedded and edge applications. Regulatory compliance requirements further reinforce demand for reliable, enterprise‑grade memory solutions across the continent’s diverse vertical markets.

South America

South America represents an emerging but steadily developing segment of the global DDR5 RDIMM memory module market. Brazil leads the regional landscape as the largest economy and most active technology adopter, supported by a growing data‑center sector and increasing cloud service penetration among enterprises and government institutions. While the pace of DDR5 RDIMM adoption in South America remains more measured compared to North America or Asia‑Pacific, rising digital infrastructure investments and the modernization of financial, telecommunications, and public‑sector IT environments are gradually creating organic demand. Argentina, Chile, and Colombia also contribute incrementally as their digital economies mature. Cost sensitivity among regional buyers and currency volatility present adoption challenges, but improving broadband connectivity, increasing hyperscaler presence, and ongoing enterprise server refresh cycles position South America as a market with meaningful long‑term growth potential in the DDR5 RDIMM memory module market.

Middle East & Africa

The Middle East and Africa region is at an early but increasingly active stage of engagement with the DDR5 RDIMM memory module market. The Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are spearheading ambitious smart‑city, artificial‑intelligence, and national cloud infrastructure projects that necessitate high‑performance server memory solutions. Saudi Arabia’s Vision 2030 and the UAE’s AI national strategy are catalyzing substantial data‑center investments, creating nascent but growing demand for DDR5 RDIMM modules in the sub‑region. South Africa serves as the primary technology adoption hub on the African continent, with increasing interest from regional enterprises and telecoms operators in upgrading aging server infrastructure. While the broader Middle East and Africa market faces challenges including limited local distribution networks and procurement budget constraints, the strategic nature of ongoing digital infrastructure programs ensures the region will play a progressively larger role in the global DDR5 RDIMM memory module market through 2034.

Get Full Report Here:

DDR5 RDIMM Memory Module Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us