Optical-Based Turbidity Sensor Market, Trends, Business Strategies 2026-2034

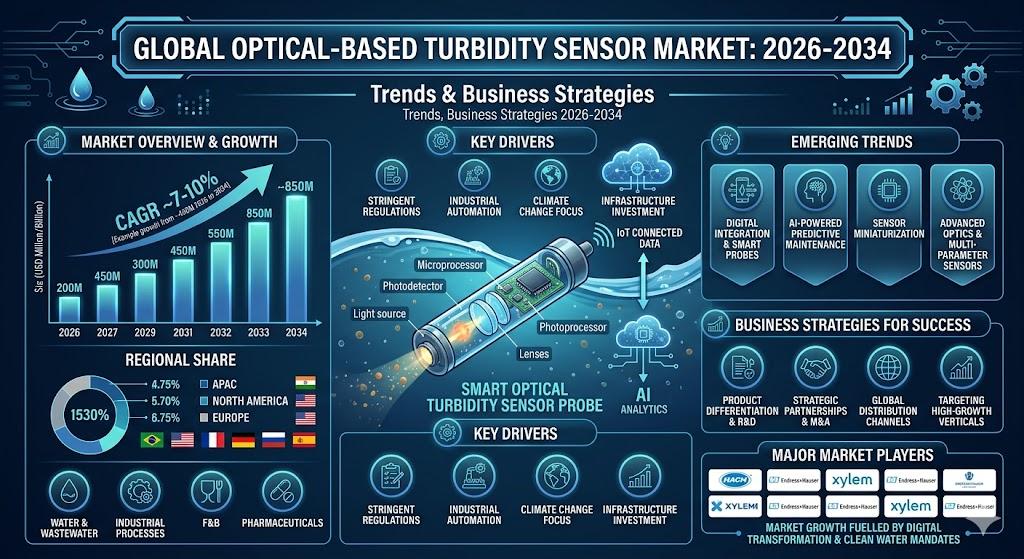

The global Optical-Based Turbidity Sensor Market is experiencing robust momentum as water quality regulations tighten and automation accelerates across industrial sectors. While the precise monetary valuation is evolving alongside rapid technology adoption, market observers consistently highlight a strong upward trajectory driven by the convergence of environmental compliance, digitalization, and the expanding footprint of water‑intensive processes worldwide.

Optical‑based turbidity sensors, which measure the scattering of light to determine the concentration of suspended particles in liquids, have become indispensable tools for maintaining product quality, safeguarding public health, and optimizing operational efficiency. Their non‑contact measurement principle, high repeatability, and compatibility with modern IoT platforms enable real‑time monitoring in applications ranging from municipal water treatment to high‑purity pharmaceutical manufacturing.

Download FREE Sample Report:

Optical-Based Turbidity Sensor Market - View in Detailed Research Report

Key Growth Drivers

Regulatory pressure remains the primary catalyst. Governments and agencies such as the U.S. Environmental Protection Agency (EPA), the European Union Water Framework Directive, and emerging standards in Asia‑Pacific mandate strict turbidity limits for drinking water and effluent discharge. Compliance requires continuous, accurate monitoring, pushing utilities and industrial operators toward optical solutions that can deliver reliable data with minimal maintenance.

Simultaneously, the digital transformation of water infrastructure is reshaping how data is collected and acted upon. Sensors equipped with built‑in diagnostics, wireless connectivity, and cloud‑ready interfaces enable predictive maintenance and advanced analytics. Operators can now anticipate fouling events, schedule cleaning cycles, and integrate turbidity data into broader process control loops, driving cost savings and sustainability outcomes.

Industrial demand is also on the rise. Sectors such as food & beverage, pharmaceuticals, chemicals, and power generation rely on precise turbidity control to meet product specifications and protect equipment from fouling. The growth of advanced manufacturing techniques, including continuous flow reactors and high‑purity crystallization, further amplifies the need for real‑time clarity assessment.

Emerging Opportunities

Beyond traditional applications, new markets are emerging. The rapid expansion of renewable energy facilities-particularly solar farms and biofuel plants-requires high‑quality water for cleaning photovoltaic panels and processing bio‑derived liquids. Likewise, the burgeoning electric‑vehicle battery supply chain utilizes large volumes of ultra‑pure water during electrode manufacturing, creating fresh demand for high‑precision turbidity monitoring.

Environmental monitoring in aquaculture, stormwater management, and coastal restoration projects is gaining traction as countries invest in ecosystem resilience. Rugged, submersible optical sensors equipped with anti‑biofouling coatings are proving especially valuable in these harsh, variable conditions.

Market Segmentation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Digital Turbidity Sensor

|

| By Application |

|

Water Treatment

|

| By End User |

|

Municipal Water Utilities

|

| By Installation Type |

|

Submersible Sensors

|

| By Optical Method |

|

Nephelometric

|

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

Dominant Manufacturers in the Optical-Based Turbidity Sensor Market

The Optical-Based Turbidity Sensor market features a competitive landscape led by established global instrumentation leaders such as Endress+Hauser and Mettler Toledo, which leverage advanced optical technologies for precise light scattering measurements in liquids. These top players command a significant revenue share, with the global top five manufacturers collectively holding a substantial portion of the market in 2025. The structure is moderately concentrated, characterized by innovation in digital and analog sensors tailored for water treatment, pharmaceuticals, and food & beverage applications, supported by robust R&D and integrated process automation solutions.

Beyond the frontrunners, niche and specialized firms like Aanderaa, OTT HydroMet, and KROHNE Group target environmental monitoring, hydrography, and industrial process control segments with rugged, high‑reliability sensors. Players such as Process Instruments (PI), Optek, and Willow Technologies offer cost‑competitive alternatives, focusing on customization and integration for chemistry and other niche uses. Educational and research‑oriented companies including Campbell Scientific and PASCO contribute to market diversity, while ongoing mergers and technological advancements intensify competition across regions like North America and Europe.

Regional Analysis: Optical-Based Turbidity Sensor Market

Regional Analysis: Optical-Based Turbidity Sensor Market

Stringent EPA guidelines mandate continuous turbidity monitoring, spurring adoption of optical‑based sensors across water utilities and industrial facilities for accurate compliance reporting.

Advanced IoT and AI synergies enhance sensor performance, allowing for automated alerts and data analytics in smart water networks prevalent in urban centers.

Food processing, pharmaceuticals, and power generation sectors prioritize reliable optical sensors to maintain process efficiency and product quality standards.

Strong R&D collaborations yield next‑generation features like self‑cleaning optics and wireless connectivity, solidifying regional market leadership.

Europe

Europe exhibits a strong presence in the Optical-Based Turbidity Sensor Market, underpinned by the EU Water Framework Directive that emphasizes comprehensive river basin management and pollution control. Countries like Germany and France lead with widespread sensor installations in wastewater treatment plants and surface water monitoring networks. The focus on circular‑economy principles drives adoption in industrial recycling processes, where optical sensors provide essential data for optimizing clarification stages. Regional strengths include a dense cluster of sensor specialists and environmental consultancies, promoting hybrid systems combining turbidity with other parameters. Challenges such as aging infrastructure are addressed through retrofit solutions, enhancing municipal capabilities. Sustainability initiatives further propel demand in agriculture for irrigation quality checks and coastal monitoring. Europe's collaborative regulatory environment ensures harmonized standards, facilitating cross‑border technology transfers and market expansion.

Asia‑Pacific

The Asia‑Pacific region emerges as a high‑growth area in the Optical-Based Turbidity Sensor Market amid rapid urbanization and industrial expansion in China, India, and Southeast Asia. Escalating water pollution from manufacturing and agriculture necessitates robust monitoring solutions, with optical sensors gaining traction for their reliability in turbid environments. Government‑led smart‑city projects integrate these devices into urban water grids, supporting real‑time quality assessments. Local manufacturers innovate cost‑effective models suited to diverse climates, while multinational players establish production bases to meet surging demand. River restoration efforts and coastal protection programs boost deployments, particularly in flood‑prone zones. Despite infrastructure variances, rising environmental awareness and policy shifts toward sustainable development position Asia‑Pacific for accelerated market penetration.

South America

South America shows promising dynamics in the Optical-Based Turbidity Sensor Market, particularly in Brazil and Chile, where water scarcity and mining activities heighten the need for precise monitoring. Optical sensors are increasingly vital in reservoirs and treatment facilities to combat sedimentation issues exacerbated by deforestation. Regional emphasis on biodiversity conservation drives their use in Amazon basin surveillance and aquaculture farms. Emerging regulations align with international standards, encouraging adoption among utilities and agribusinesses. Partnerships with global firms introduce advanced analytics, bridging technology gaps. Economic diversification efforts further embed sensors in oil and gas wastewater management, fostering gradual market maturation.

Middle East & Africa

In the Middle East & Africa, the Optical-Based Turbidity Sensor Market gains momentum through desalination plants and oilfield operations, where water purity is paramount. Gulf nations invest in sensor technologies to optimize reverse osmosis processes, reducing operational costs. Africa's focus on rural electrification and sanitation projects incorporates portable optical units for groundwater assessment. Harsh desert conditions spur ruggedized designs, with regional hubs in South Africa leading local adaptations. International aid and public‑private partnerships accelerate deployments in contaminated river systems, addressing public health concerns. Progressive water‑security strategies enhance prospects for sustained growth.

Get Full Report Here:

Optical-Based Turbidity Sensor Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us