SiC Diodes Market, Trends, Business Strategies 2026-2034

The global SiC Diodes Market is witnessing robust expansion as designers across automotive, renewable energy, data‑center, and industrial sectors increasingly adopt wide‑bandgap technology to meet ever‑tighter efficiency and reliability requirements. The transition to electric mobility, the scaling of grid‑scale storage, and the push for higher power density in modern power converters are collectively accelerating demand for high‑performance silicon‑carbide (SiC) diodes.

SiC diodes are distinguished by their exceptional breakdown voltage, low forward voltage drop, and ability to operate at temperatures exceeding 200 °C. These characteristics enable designers to produce lighter, smaller, and more reliable power modules, reducing bill‑of‑materials costs and simplifying thermal management. As a result, SiC diodes have become a critical enabler for next‑generation electric‑vehicle (EV) onboard chargers, fast‑charging stations, renewable‑energy inverters, and high‑efficiency industrial motor drives.

Download FREE Sample Report:

SiC Diodes Market - View in Detailed Research Report

Automotive Industry Expansion: The Primary Growth Engine

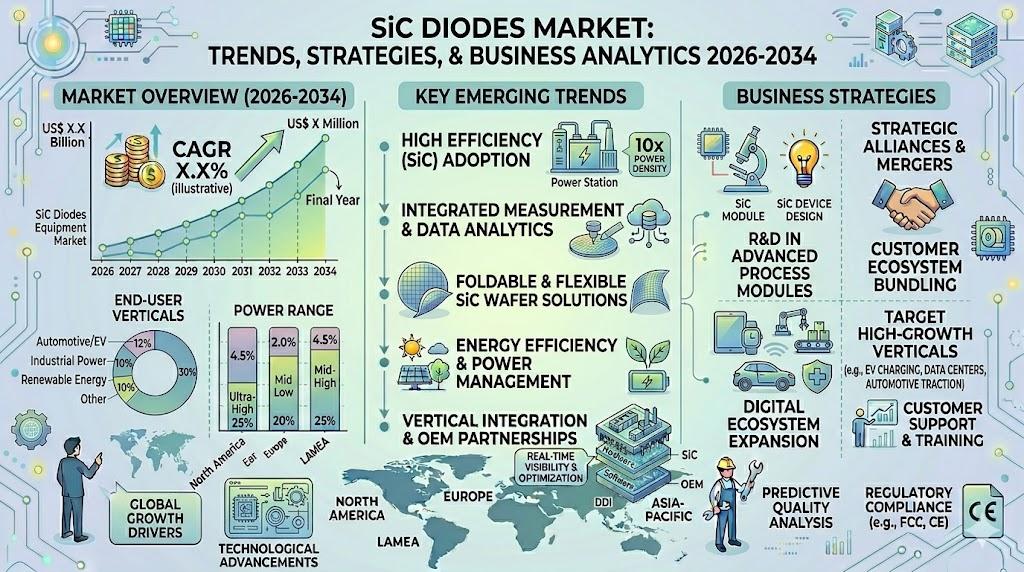

The report identifies the explosive growth of the global automotive sector-particularly the electric‑vehicle (EV) and hybrid‑electric‑vehicle (HEV) segments-as the paramount driver for SiC diode adoption. Automotive applications currently account for roughly two‑thirds of the total SiC diode demand, with vehicle manufacturers seeking to improve drivetrain efficiency, extend driving range, and meet stringent global emission standards. The shift toward 800 V and higher voltage architectures in EVs further amplifies the need for SiC devices that can handle higher power levels while maintaining compact form factors.

Beyond passenger cars, commercial EVs, electric buses, and two‑wheelers are also contributing to a diversified demand base. Tier‑one suppliers are actively collaborating with semiconductor manufacturers to co‑develop application‑specific SiC diode solutions, resulting in longer product lifecycles and more predictable supply chains.

In parallel, the renewable‑energy sector is propelling SiC diode growth. Grid‑connected photovoltaic (PV) inverters, energy‑storage systems, and wind‑turbine converters increasingly rely on SiC diodes to achieve higher conversion efficiencies, lower losses, and reduced cooling requirements. The convergence of automotive and renewable‑energy demand creates a synergistic effect, encouraging manufacturers to scale production capacities and drive down unit costs.

Industrial motor drives, data‑center power supplies, and rail‑transport traction systems also represent significant and growing end‑uses. These applications benefit from the fast switching speeds and thermal robustness of SiC diodes, which translate into higher system reliability and lower total cost of ownership.

Key market dynamics shaping the SiC diodes landscape include:

- Technology Innovation: Continuous improvements in planar, trench, and junction‑barrier Schottky architectures are delivering lower forward voltage drops and higher surge current capabilities.

- Supply‑Chain Consolidation: The top five players command over 70 % of market share, fostering stability but also prompting strategic M&A activity among niche innovators.

- Policy Support: Government incentives for EV adoption, renewable‑energy integration, and domestic semiconductor development are particularly pronounced in the Asia‑Pacific region, accelerating regional demand.

- Cost‑Reduction Pressure: As volume ramps up, manufacturers are focusing on wafer‑scale cost efficiencies, advanced packaging, and economies of scale to make SiC solutions price‑competitive with traditional silicon.

Segment Analysis

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

650V SiC SBD is the predominant category. This leadership is driven by its widespread adoption in mainstream consumer and industrial power applications, particularly within onboard chargers and power supplies for the electric vehicle and renewable energy sectors. Its optimal balance of performance and cost for mid‑voltage requirements makes it a go‑to solution for efficiency‑focused designs. The proliferation of 650V SiC SBDs is further propelled by their ability to enable smaller heat sinks and passive components, offering manufacturers significant advantages in product miniaturization and thermal management. |

| By Application |

|

Automotive & EV/HEV is the dominant application fueling market expansion. This segment's leadership is underpinned by the global transition to electric mobility, where SiC diodes are critical for enhancing power conversion efficiency in traction inverters, onboard chargers, and DC‑DC converters, directly extending vehicle range and reducing charging times. Major automotive OEMs are actively integrating SiC technology to gain a competitive performance edge, which in turn creates a substantial and sustained demand pipeline from tier‑one suppliers and semiconductor manufacturers. |

| By End User |

|

Automotive OEMs & Tier‑1 Suppliers represent the most influential and fast‑growing end‑user group. Their drive to innovate and meet stringent efficiency and emission regulations compels the adoption of SiC diodes, which are seen as enabling technology for next‑generation electric powertrains. This user base fosters a highly collaborative development environment with semiconductor companies to co‑create application‑specific solutions. The significant R&D budgets and long‑term supply agreements typical of this segment provide stability and direction for the entire SiC diodes supply chain. |

| By Voltage Class |

|

Low & Medium Voltage (Up to 1200V) is the leading segment, encompassing the most commercially active and volume‑driven part of the market. This dominance is linked to its synergy with the leading 650V and 1200V product types, which serve core applications in automotive and industrial systems. The technological maturity, broader supplier base, and ongoing cost‑reduction efforts for these voltage classes make them more accessible to a wider range of system designers. The segment benefits from continuous innovation aimed at improving switching speeds and thermal performance for even greater efficiency gains. |

| By Manufacturing Technology |

|

Planar Schottky Barrier Diodes currently hold a leading position due to their manufacturing simplicity and proven reliability in early‑generation SiC devices. They are the workhorse technology for many established applications. However, the competitive landscape is evolving as Trench and JBS architectures gain prominence, offering superior performance characteristics like lower forward voltage drops and enhanced surge current capability. This drives a dynamic technological race, with leading manufacturers investing heavily to refine these newer processes for volume production. |

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidating Market Fueled by Automotive and Energy Transition Demand

The global SiC diodes market is characterized by a high degree of consolidation, with the top five players commanding over 70% of the market share. STMicroelectronics, Infineon Technologies, and Wolfspeed are the clear frontrunners, leveraging their vertical integration capabilities, extensive R&D investments, and established relationships with major automotive and industrial customers to dominate the landscape. This leadership is anchored in the surging demand from the Automotive & EV/HEV segment, which accounts for approximately 67% of the application share. The race for higher power density and efficiency in electric vehicles, charging infrastructure, and renewable energy systems like PV and energy storage is the primary competitive battleground, pushing continuous innovation in diode performance and cost reduction.

The competitive field extends beyond the absolute leaders to include several significant players that hold critical positions in specific regions or application niches. Companies like Rohm Semiconductor, onsemi, and Microchip Technology (through its Microsemi acquisition) are formidable contenders with comprehensive SiC portfolios. Concurrently, the market sees dynamic activity from specialized pure‑play and fabless firms such as Navitas (GeneSiC), Qorvo (UnitedSiC), and BASiC Semiconductor, which compete on technological agility. In the crucial Asia‑Pacific region, which holds about a 60% market share, domestic players like San'an Optoelectronics, WeEn Semiconductors, and CETC 55 are increasingly influential, supported by regional supply chain development and strong governmental support for the new energy sector.

List of Key SiC Diodes Companies Profiled

-

STMicroelectronics

-

Wolfspeed, Inc.

-

Rohm Semiconductor

-

onsemi

-

Fuji Electric Co., Ltd.

-

Navitas Semiconductor (GeneSiC)

-

Toshiba Electronic Devices & Storage Corporation

-

San'an Optoelectronics Co., Ltd.

-

Littelfuse, Inc. (IXYS)

-

CETC 55

-

WeEn Semiconductors Co., Ltd.

-

BASiC Semiconductor

-

SemiQ

-

Diodes Incorporated

Regional Analysis: SiC Diodes Market

The region's control over the SiC Diodes Market supply chain is paramount. It hosts key players across the value chain, from substrate growers to advanced packaging facilities. This vertical integration reduces logistical complexities and costs, enabling rapid scalability in production to meet global demand surges, particularly for automotive‑grade components.

Explosive growth in electric vehicle production is the single largest driver for SiC diodes in Asia‑Pacific. Local OEMs are leading the adoption of 800V architectures, which require high‑performance SiC solutions. Simultaneously, the massive consumer electronics sector demands efficient power supplies, further propelling the SiC Diodes Market.

National strategies in China, Japan, and South Korea explicitly prioritize wide‑bandgap semiconductors like SiC. Substantial state funding, subsidies for EV adoption, and targets for renewable energy integration create a powerful policy‑led tailwind for the SiC Diodes Market, encouraging both R&D and large‑scale manufacturing investments.

Asia‑Pacific is a central arena for innovation in the SiC Diodes Market, with continuous advancements in diode design for higher current density and reliability. Regional companies are at the forefront of developing novel packaging techniques to better manage heat dissipation, which is critical for performance in automotive and industrial applications.

North America

North America holds a strong position in the SiC Diodes Market, characterized by high‑value innovation and early adoption in premium applications. The region benefits from advanced research institutions and the presence of leading SiC material and device innovators. Demand is heavily driven by the automotive sector, where premium EV manufacturers are integrating SiC‑based powertrains for superior performance, and by the data center industry's relentless pursuit of energy efficiency in power supplies. The defense and aerospace sectors also provide a stable, high‑reliability demand stream for radiation‑hardened SiC diode components. Strategic collaborations between material suppliers, fabless chip designers, and automotive OEMs are common, creating a vibrant ecosystem focused on next‑generation SiC diode technology for the global market.

Europe

Europe is a significant and maturing region in the SiC Diodes Market, with demand anchored by its strong automotive industry and ambitious green energy targets. European automakers are aggressively transitioning to electric mobility, creating substantial demand for SiC diodes in onboard chargers, traction inverters, and DC‑DC converters. The region's focus on industrial automation and high‑quality manufacturing drives adoption in motor drives and robust power supplies. Furthermore, Europe's commitment to renewable energy, especially solar and wind, fuels the need for efficient SiC‑based power conversion in inverters and grid infrastructure. Collaborative projects between academia, research institutes, and industry, often supported by EU funding, are pivotal in advancing SiC diode technology and manufacturing capabilities within the region.

South America

The SiC Diodes Market in South America is in a nascent but developing stage, with growth potential linked to infrastructure modernization and regional economic trends. Primary interest is emerging in the renewable energy sector, particularly in Brazil and Chile, where solar and wind projects are creating demand for more efficient power electronics. The gradual adoption of electric buses and vehicles in urban centers also presents a future growth avenue. However, market penetration faces challenges, including reliance on imported components, currency volatility, and a less established local semiconductor ecosystem compared to global leaders. Growth is expected to be steady, driven by specific industrial upgrades and the gradual trickle‑down of global SiC diode technology into cost‑sensitive applications.

Middle East & Africa

The Middle East & Africa region represents an emerging opportunity within the SiC Diodes Market, with dynamics split between energy diversification and infrastructure development. In the Middle East, nations are investing heavily in diversifying their energy mix beyond oil, leading to major solar and wind projects that require advanced power conversion equipment incorporating SiC technology. The region's focus on smart cities and data center construction also generates niche demand. In Africa, growth is more gradual, linked to electrification projects, telecommunications infrastructure expansion, and mining operations where efficiency gains are critical. The overall market is characterized by strategic project‑based adoption rather than broad‑based consumption, with significant potential in the long term as technology costs decrease.

Get Full Report Here:

SiC Diodes Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us