Inference Chip (Edge AI) Market, Trends, Business Strategies 2026-2034

The global Inference Chip (Edge AI) Market is experiencing a rapid surge as enterprises worldwide prioritize low‑latency, on‑device artificial intelligence to meet the growing demand for real‑time analytics. The expansion is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the pivotal role of edge inference chips in enabling a new generation of smart devices, from autonomous vehicles to industrial robots, by delivering high‑performance AI workloads while preserving power efficiency.

Inference chips, designed to execute neural network models directly at the edge, are becoming indispensable for reducing data‑transfer costs, enhancing privacy, and meeting stringent latency requirements. Their integration across a breadth of industries is accelerating digital transformation, allowing manufacturers to shift from cloud‑centralized models to decentralized, responsive architectures that improve operational agility and customer experience.

Download FREE Sample Report:

Inference Chip (Edge AI) Market - View in Detailed Research Report

Semiconductor Industry Expansion: The Primary Growth Engine

The report identifies the exploding growth of the global semiconductor industry as the foremost catalyst for inference‑chip demand. As semiconductor manufacturers scale advanced process nodes and integrate AI‑centric design kits, the need for dedicated inference silicon to offload compute from general‑purpose cores becomes ever more pronounced. The proliferation of AI‑enabled sensors, cameras, and edge gateways drives a virtuous cycle in which higher‑density chips enable richer AI models, which in turn stimulate further semiconductor innovation.

“The concentration of AI‑focused fab capacity in the Asia‑Pacific region, complemented by substantial R&D investments in the United States and Europe, creates a globally distributed supply chain that fuels the edge AI market,” the report notes. With cumulative semiconductor capital expenditures projected to exceed $600 billion through 2034, the demand for inference‑chip solutions that can operate within tight power and thermal envelopes will only intensify.

Read Full Report: https://semiconductorinsight.com/report/inference-chip-edge-ai-market/

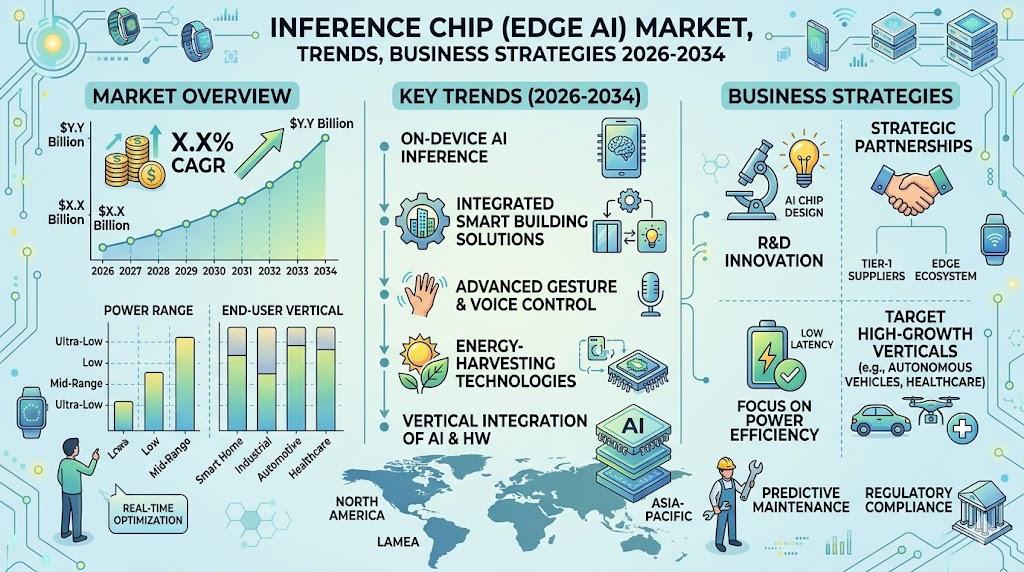

Market Segmentation: ASIC‑Based Solutions and Industrial Automation Lead

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Type

- ASIC (Application‑Specific Integrated Circuit)

- FPGA (Field‑Programmable Gate Array)

- Embedded GPU

By Application

- Autonomous Vehicles

- Smart Surveillance

- Industrial Automation

- Others

By End User

- Automotive OEMs

- System Integrators

- Consumer Electronics

By Architecture

- Neuromorphic

- Heterogeneous Multi‑Core

- Traditional Von Neumann

By Power Profile

- Ultra Low Power

- Mid‑Range Power

- High Performance

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=142471

Competitive Landscape: Key Players and Strategic Focus

Inference Chip (Edge AI) Competitive Landscape Overview

The Edge AI inference chip market is currently dominated by a handful of vertically integrated technology giants that couple mature semiconductor design capabilities with extensive software ecosystems. NVIDIA leads the segment with its Jetson family, offering high‑performance GPUs and dedicated Tensor cores for vision‑based workloads, while Qualcomm leverages its Snapdragon Neural Processing Engine to embed AI acceleration across a broad portfolio of mobile and IoT devices. Intel’s acquisition of Movidius and its subsequent VPU line provides low‑power inference for edge cameras, and Google’s Edge TPU delivers a tightly coupled ASIC solution focused on ultra‑low latency in smart home and industrial sensors. These leaders benefit from deep R&D resources, extensive developer tools, and strategic partnerships that reinforce a tiered market structure: premium performance tiers commanded by NVIDIA and Intel, mid‑range solutions anchored by Qualcomm and Google, and emerging opportunities in consumer wearables and automotive ADAS where cost efficiency drives adoption.

Beyond the dominant players, a vibrant ecosystem of niche innovators is reshaping the competitive dynamics by targeting specialized form factors, power envelopes, or novel architectural approaches. Graphcore’s Intelligence Processing Unit (IPU) emphasizes fine‑grained parallelism for transformer models, while Cerebras Systems offers wafer‑scale engines that collapse thousands of cores onto a single substrate. Companies such as Mythic and Syntiant focus on analog–digital hybrid chips that dramatically reduce energy per inference, making them attractive for battery‑constrained wearables. Hailo’s low‑latency, high‑throughput processors target automotive edge compute, and Israel‑based Kneron provides AI‑centric MCUs for smart appliances. These challengers, though smaller in revenue, inject differentiated capabilities that compel the incumbents to accelerate feature rollouts and price competitiveness across the broader Edge AI landscape.

List of Key Inference Chip (Edge AI) Companies Profiled

-

NVIDIA

-

Intel

-

AMD

-

Apple

-

MediaTek

-

Samsung Electronics

-

Huawei (HiSilicon)

-

Texas Instruments

-

Mythic

-

Syntiant

-

Hailo

-

Kneron

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC‑Based Solutions dominate the type segment because they deliver the highest inference efficiency and deterministic power consumption. Key qualitative observations include:

|

| By Application |

|

Industrial Automation emerges as the leading application tier, driven by the need for real‑time defect detection and predictive maintenance. Qualitative drivers include:

|

| By End User |

|

Automotive OEMs constitute the primary end‑user group, primarily because edge inference chips underpin safety‑critical functions such as driver monitoring and advanced driver‑assistance systems. Notable qualitative insights:

|

| By Architecture |

|

Heterogeneous Multi‑Core architectures are gaining prominence as they allow simultaneous execution of diverse AI workloads while balancing power budgets. Qualitative observations:

|

| By Power Profile |

|

Mid‑Range Power solutions are the sweet spot for most edge deployments, offering a balance between energy consumption and inference throughput. Illustrative qualitative points:

|

Regional Analysis: North America

The automotive sector in North America is witnessing a significant shift towards autonomous driving and advanced driver‑assistance systems (ADAS). This demand is directly driving the adoption of inference chips for real‑time sensor fusion and decision‑making.

Edge AI and inference chips are being leveraged for medical imaging analytics, remote patient monitoring, and personalized treatment planning, reducing latency and protecting patient data.

Predictive maintenance, quality inspection, and process optimization are increasingly powered by edge inference, delivering measurable efficiency gains across manufacturing plants.

Edge AI enables real‑time inventory tracking, smart checkout experiences, and dynamic routing, fostering a competitive edge for retailers and logistics providers.

North America

The North American market is characterized by a strong focus on innovation, rapid adoption of 5G, and a collaborative ecosystem that brings together chip designers, system integrators, and end‑user industries. While competition intensifies, the region’s established supply chain and robust demand for high‑performance AI at the edge create a solid foundation for sustained growth.

Europe

Europe represents a significant and steadily growing market for inference chips. Stringent data‑privacy regulations, such as GDPR, and a strong emphasis on energy‑efficient industrial automation drive the adoption of secure, low‑power edge AI solutions. Automotive hubs in Germany and the UK, alongside a thriving healthcare sector focused on personalized medicine, further accelerate demand.

Asia‑Pacific

Asia‑Pacific is projected to be the fastest‑growing region. Massive AI R&D spend in China, Japan, and South Korea, coupled with a dense IoT device ecosystem and cost‑effective manufacturing, fuels rapid market expansion. The Chinese automotive industry, in particular, is a major consumer of edge inference chips for smart vehicle platforms.

South America

South America is an emerging market where increasing connectivity in agriculture, mining, and logistics is driving early adoption of edge AI. While infrastructure challenges remain, government‑backed digital transformation programs are laying the groundwork for broader deployment.

Middle East & Africa

The Middle East and Africa present nascent opportunities. Investments in smart infrastructure, oil‑and‑gas automation, and healthcare digitization are creating initial demand for inference chips that can operate under harsh environmental conditions while maintaining low power consumption.

Get Full Report Here:

Inference Chip (Edge AI) Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us