Elevator Seismic Sensor Market, Trends, Business Strategies 2026-2034

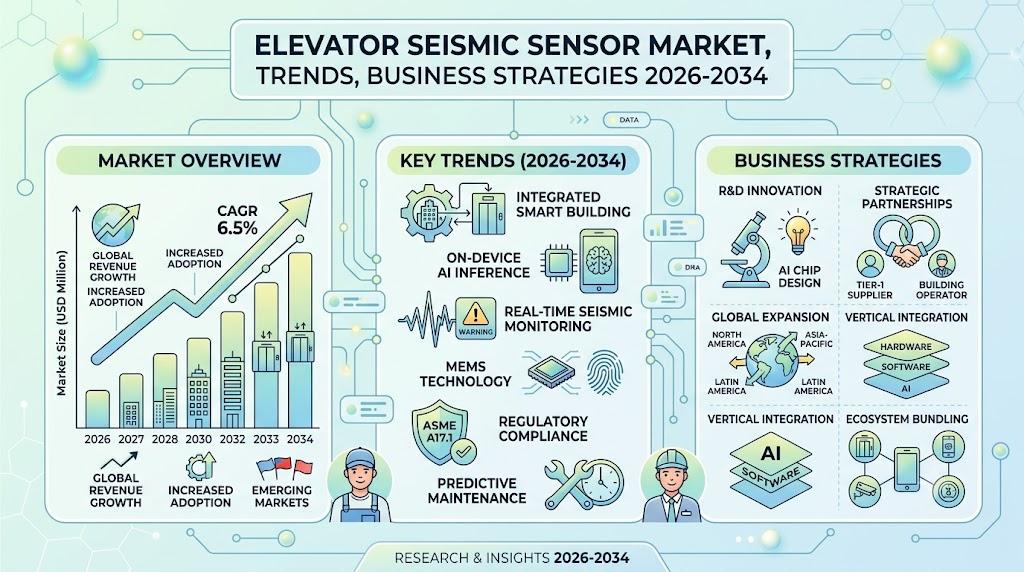

The global Elevator Seismic Sensor Market, projected to reach **US$ 150 million** by 2034, is on a clear trajectory of growth as vertical transportation systems worldwide confront the twin pressures of rapid urbanisation and heightened seismic safety expectations. This expansion is detailed in a newly released research report published by Semiconductor Insight. The study underscores the essential role of advanced seismic detection devices in protecting passengers, safeguarding critical building infrastructure, and ensuring uninterrupted operation of elevators during and after an earthquake.

Elevator seismic sensors are specialised devices that continuously monitor ground motion and automatically trigger emergency shutdown or safe‑stop protocols when seismic activity exceeds predefined thresholds. By detecting the early‑arriving S‑waves and the more destructive P‑waves, these sensors prevent elevators from operating in unsafe conditions, thereby averting entrapment, equipment damage, and potential loss of life. Their integration into modern elevator control systems has become a standard safety requirement in many high‑rise buildings, especially in regions with significant seismic risk.

Download FREE Sample Report:

Elevator Seismic Sensor Market - View in Detailed Research Report

Regulatory Momentum: The Principal Growth Engine

The report identifies tightening building codes and mandatory safety regulations as the primary catalyst for market expansion. In seismically active nations such as Japan, New Zealand, and parts of China, legislation explicitly mandates the installation of seismic sensors in new elevators and often requires retro‑fitting of older lifts to comply with updated standards. These regulations are not advisory; they are enforceable conditions for project approval, building permits, and insurance coverage. As a result, manufacturers and system integrators are experiencing a sustained pipeline of orders from commercial developers, residential tower projects, and public‑sector infrastructure initiatives.

“The concentration of high‑rise construction in the Asia‑Pacific, combined with rigorous seismic safety codes, creates a non‑negotiable market driver for elevator seismic sensor providers,” the report notes. The growing emphasis on resilient urban design, coupled with government incentives for disaster‑ready infrastructure, fuels demand across all elevator segments.

Urbanisation and High‑Rise Construction: A Secondary Growth Pillar

The relentless pace of vertical development in emerging economies adds a powerful secondary thrust to the market. Southeast Asian megacities such as Jakarta, Manila, and Ho Chi Minh City are witnessing unprecedented skyscraper construction, each requiring sophisticated elevator safety solutions. Developers increasingly view seismic sensor integration as a value‑adding feature that not only meets code compliance but also enhances marketability, particularly for luxury residential and premium office towers that promote safety as a core selling point.

In parallel, retro‑fit projects for ageing elevator fleets in mature markets (e.g., Japan, Australia, and the United States) generate a continuous demand stream. Building owners seeking to extend the service life of existing vertical transport systems must upgrade to the latest sensor technologies to remain compliant and competitive.

Technological Convergence: Smart Buildings and IoT Integration

Advancements in the Internet of Things (IoT), cloud‑based analytics, and artificial intelligence are reshaping the functional envelope of elevator seismic sensors. Modern sensor packages now include wireless communication modules that feed real‑time vibration data to building management systems (BMS) and cloud dashboards. Predictive maintenance algorithms analyse this data to differentiate between genuine seismic events and routine building vibrations, reducing false alarms by up to 40 % in test environments.

Networked sensor architectures enable centralized monitoring of multiple elevators across a single high‑rise or an entire portfolio of properties. This capability is especially valuable for facilities managers who must coordinate emergency response, conduct post‑event diagnostics, and generate compliance reports for regulatory bodies.

Market Segmentation: Sensors, Applications and Integration Pathways

The report provides a granular segmentation analysis that illuminates the market’s structural composition and highlights the most lucrative sub‑segments.

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

S Wave Seismic Sensor remains the cornerstone technology for rapid earthquake response because it captures the high‑energy shear waves that cause the most severe ground motion. Ongoing R&D focuses on improving sensor sensitivity while eliminating spurious triggers from nearby construction or traffic vibrations.

|

| By Application |

|

Commercial Elevator applications drive the bulk of demand, given the large passenger volumes and strict safety codes in office towers, hotels, and shopping centres. Retrofit programmes for legacy shafts, especially in densely built city centres, add a persistent secondary market.

|

| By End User |

|

Elevator Manufacturers (OEMs) are the primary demand generators, embedding sensors directly into new lift designs. Their specifications often dictate sensor performance thresholds, driving supplier innovation.

|

| By Technology Integration |

|

Networked & Smart Building Integrated Systems are emerging as the dominant growth segment. They enable centralized monitoring, real‑time alerts, and data‑driven maintenance scheduling, aligning with broader smart‑city initiatives.

|

| By Detection Methodology |

|

Advanced Signal Analysis & Pattern Recognition is gaining prominence as it dramatically reduces false positives. Machine‑learning models are trained on local vibrational signatures to discriminate earthquakes from routine mechanical noise.

|

Competitive Landscape: Key Industry Players

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Led by Specialized Safety Technology Providers

The global elevator seismic sensor market exhibits a semi‑consolidated competitive structure, anchored by a core group of established players specializing in elevator safety components and seismic detection technology. Meisei Electric is recognised as a leading global manufacturer, leveraging its strong reputation and technological expertise in seismic detection, with notable market share concentrated in seismically active regions like Japan and the broader Asia‑Pacific market. The competitive landscape is further characterised by companies like Sanjin Elevator Parts and WECO, which have successfully integrated seismic sensors into their broader portfolios of elevator components, securing their positions through established distribution channels and relationships with major elevator OEMs and maintenance providers. The market’s projected growth to US$ 150 million by 2034 is intensifying competition, driving innovation in sensor accuracy, particularly for P‑wave detection, and integration with smart building systems.

Beyond the dominant players, several significant niche companies are carving out specialised positions. Firms such as Seismic Switch and ADAMS focus primarily on advanced seismic safety devices, bringing dedicated R&D to enhance sensor sensitivity and reliability. Regional specialists like PROSPECT Photoelectric Tech and E‑Feng Machinery command strong domestic presence in the significant Chinese market, which is a key consumption region. Other players, including Toyo Automation, compete through cost‑competitive manufacturing and tailored solutions for specific elevator types, such as those used in commercial high‑rises versus residential buildings. This tiered market dynamic ensures that while technological leadership from top firms sets standards, competitive pressures on price and regional service continue to influence market share distribution globally.

List of Key Elevator Seismic Sensor Companies Profiled

-

Seismic Switch Corp.

-

WECO

-

ADAMS Elevator Equipment Ltd.

-

E‑Feng Machinery & Electric Co., Ltd.

-

Toyo Automation Co., Ltd.

-

FUKUDA DENSHI CO., LTD

-

Mitsubishi Electric Corporation

-

Kone Oyj

-

SICK AG

-

Hansford Sensors Ltd.

-

Omron Corporation

These companies are concentrating on technological advancement-particularly the integration of IoT for predictive safety, AI‑driven signal analysis, and the development of compact, low‑power sensor modules. Geographic expansion into high‑growth regions such as Southeast Asia, the Middle East, and Latin America forms a key pillar of their growth strategies.

Regional Analysis: Elevator Seismic Sensor Market

Regional Analysis: Elevator Seismic Sensor Market

Building codes in Japan, New Zealand, and parts of China set stringent global benchmarks for elevator seismic performance, directly accelerating sensor adoption. These are not mere guidelines but enforceable standards critical for project approval, creating a non‑negotiable market driver for elevator seismic sensor manufacturers and integrators.

The unprecedented rate of high‑rise construction across Southeast Asia and India establishes a vast greenfield market for modern elevator systems. Developers increasingly view integrated seismic safety, powered by sophisticated sensors, as a premium feature and a key component for sustainable, resilient urban infrastructure.

The region is a global centre for electronics manufacturing and IoT innovation, facilitating the development of cost‑effective and smart sensor solutions. This ecosystem allows for seamless integration of elevator seismic sensor data into broader building management and smart city platforms, enhancing overall operational resilience.

Beyond new construction, a significant market segment involves upgrading existing elevator infrastructure in older buildings to meet contemporary safety codes. This creates a continuous, secondary demand stream for retrofit‑compatible elevator seismic sensor systems throughout mature markets like Japan and Australia.

North America

The North American market for elevator seismic sensors is mature and technologically advanced, primarily driven by stringent seismic building codes in high‑risk zones such as California, British Columbia, and Alaska. The market is characterised by a focus on high‑performance, reliable systems that integrate with complex Building Management Systems (BMS) and adhere to strict certification standards from bodies like the California Division of the State Architect (DSA). Demand is fueled by both commercial real‑estate in major cities and critical infrastructure projects, including hospitals and government buildings, where operational continuity post‑event is paramount. A growing emphasis on smart buildings and predictive maintenance is pushing the adoption of next‑generation elevator seismic sensor solutions that offer remote diagnostics and real‑time data analytics.

Europe

The European elevator seismic sensor market is defined by a diverse regulatory landscape and varying levels of seismic activity. Southern European nations, particularly Italy, Greece, and Turkey, represent the core demand centres due to their higher seismic risk, prompting rigorous national safety directives for elevator installations. In contrast, Western and Northern European markets focus more on modernisation and the adoption of overarching EU machinery safety standards, which increasingly account for seismic resilience in critical lifts. The market sees steady growth from the retrofit of historical buildings and the expansion of urban transit systems, where integrating advanced seismic monitoring in elevator shafts is part of broader infrastructure resilience planning.

South America

The South American elevator seismic sensor market is concentrated in seismically active countries along the Pacific Ring of Fire, notably Chile and Peru. These regions have developed highly specialised building codes informed by significant historical seismic events, creating a mandatory and sophisticated market for safety equipment, including elevator sensors. Growth is tied to mining, commercial and residential high‑rise construction in urban centres. A key regional challenge and opportunity lie in elevating safety standards and sensor adoption in other developing nations with seismic risk, where economic factors and enforcement capabilities directly influence market penetration for elevator seismic sensor technologies.

Middle East & Africa

The market dynamics in the Middle East & Africa region are bifurcated. The Gulf Cooperation Council (GCC) countries, while largely aseismic, are global leaders in super‑tall construction and luxury real‑estate, driving demand for state‑of‑the‑art elevator safety systems, including seismic sensors, as part of premium, globally compliant building packages. In contrast, parts of North Africa and East Africa face genuine seismic hazards but have nascent markets constrained by economic development priorities and evolving regulatory frameworks. The regional elevator seismic sensor market’s long‑term growth hinges on infrastructure investment and the gradual formalisation of building safety codes that mandate such advanced protective technologies.

Get Full Report Here:

Elevator Seismic Sensor Market, Trends, Business Strategies 2026‑2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us