PCIe SSD for AI Market, Trends, Business Strategies 2026-2034

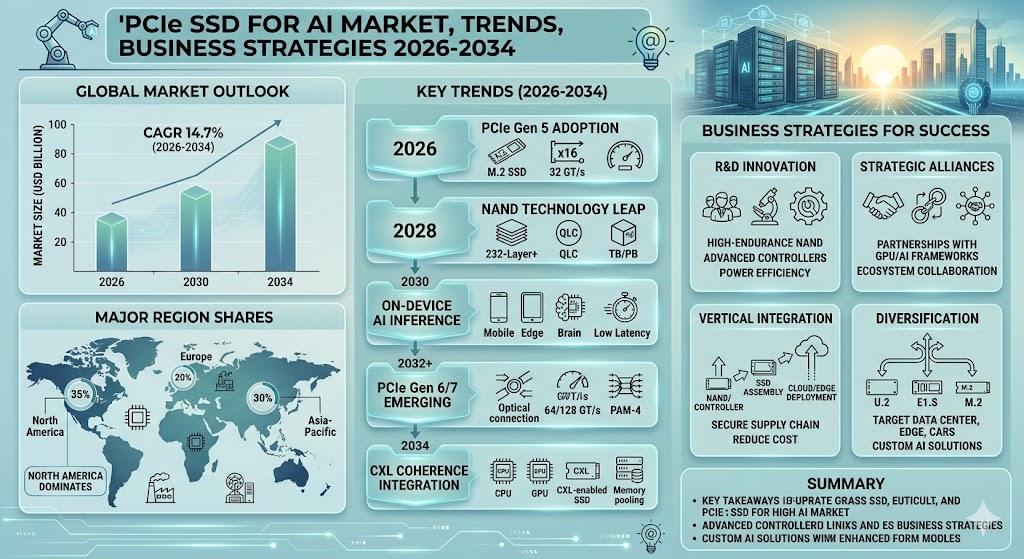

The global PCIe SSD for AI Market, valued at a robust US$ 527 million in 2025, is on a trajectory of significant expansion, projected to reach US$ 1,086 million by 2034. This growth, representing a compound annual growth rate (CAGR) of 11.2%, is detailed in a comprehensive new report published by Semiconductor Insight. The study highlights the pivotal role of high‑performance PCIe solid‑state drives (SSDs) in powering the next generation of artificial‑intelligence (AI) and machine‑learning (ML) workloads across hyperscale data centers, edge compute nodes, and emerging autonomous systems.

PCIe SSDs, engineered for ultra‑low latency, high IOPS, and sustained multi‑gigabyte‑per‑second data throughput, have become the de‑facto storage substrate for AI inference and training pipelines. Their ability to keep pace with the explosive bandwidth demands of modern GPUs, TPUs, and custom AI accelerators guarantees that data‑starved models can be fed continuously, eliminating the I/O bottlenecks that once limited scaling of large language models, computer‑vision networks, and reinforcement‑learning systems.

Download FREE Sample Report:

PCIe SSD for AI Market - View in Detailed Research Report

The acceleration of AI deployments is being driven by several converging forces. First, the relentless advancement of AI algorithms has expanded model sizes dramatically, creating a direct need for storage that can deliver terabytes of data with sub‑millisecond access times. Second, the proliferation of generative‑AI services, autonomous‑vehicle perception stacks, and real‑time video analytics is pushing cloud providers and enterprises to redesign their storage hierarchies around PCIe‑native flash. Third, emerging standards such as PCIe 5.0 and the upcoming PCIe 6.0 specification are unlocking further bandwidth headroom, making next‑generation SSDs a strategic differentiator for organizations seeking to maintain competitive AI compute efficiency.

AI Infrastructure Expansion: The Primary Growth Engine

The report identifies the explosive growth of AI‑centric compute infrastructure as the paramount driver for PCIe SSD for AI demand. With hyperscale data‑center operators allocating increasingly larger portions of their capital expenditure to AI‑optimized storage, the correlation between AI workload intensity and SSD adoption is direct and substantial. The AI‑driven storage market is projected to outpace traditional enterprise flash, reinforcing the importance of PCIe‑based solutions in the broader semiconductor ecosystem.

“The concentration of AI‑focused cloud platforms and on‑premise AI labs in North America and Asia‑Pacific, which together account for roughly 70 % of global AI‑related storage spend, is a key factor in the market’s dynamism,” the report notes. With global investments in AI compute infrastructure exceeding $300 billion through 2030, the demand for PCIe SSDs that can sustain massive data ingestion rates is set to intensify, especially as generative‑AI models transition from research prototypes to production services.

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

PCIe SSD for AI Market - Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

The global PCIe SSD for AI market is characterized by intense competition among a handful of technologically advanced semiconductor and storage solution providers. Samsung Electronics maintains its position as the dominant force in this space, leveraging its vertically integrated NAND flash manufacturing capabilities and extensive R&D investments to deliver high-performance PCIe 4.0 and PCIe 5.0 SSDs tailored for AI and machine learning workloads. The South Korean giant's enterprise‑grade SSD portfolio - engineered for ultra‑low latency, exceptional IOPS, and sustained data throughput - makes it the preferred supplier for hyperscale data centers and AI infrastructure deployments globally. Western Digital and Micron Technology closely follow, each bringing formidable NAND fabrication expertise and robust product roadmaps focused on next‑generation PCIe interfaces. SK Hynix, buoyed by its acquisition of Intel's NAND and SSD business, has significantly strengthened its competitive standing, offering storage solutions optimized for high‑performance computing (HPC) and AI training environments. The top five players collectively commanded a substantial share of global market revenue in 2025, underscoring the oligopolistic nature of this high‑barrier industry, which was valued at approximately USD 527 million in 2025 and is projected to reach USD 1,086 million by 2034, growing at a CAGR of 11.2%.

Beyond the leading incumbents, several niche and emerging players are actively carving out competitive positions within the PCIe SSD for AI ecosystem. KIOXIA (formerly Toshiba Memory) continues to leverage its deep NAND flash heritage to deliver enterprise SSDs with strong endurance characteristics suited to continuous AI inference workloads. Intel, through its Optane and QLC NAND SSD lines, targets latency‑sensitive AI applications in data centers and edge computing environments. Seagate Technology, traditionally a hard‑disk‑drive leader, has strategically expanded its SSD portfolio to address AI and HPC storage demands. Kingston Technology and ADATA serve as competitive mid‑market players, offering cost‑effective PCIe SSD solutions for industrial AI and automotive applications. Gigabyte Technology, primarily known for its motherboards and PC components, also participates in this market with PCIe SSD offerings targeting workstation‑class AI development use cases. Collectively, these players are driving innovation across PCIe 4.0 and PCIe 5.0 SSD segments, intensifying competition on performance benchmarks, power efficiency, and total cost of ownership for AI‑driven enterprise customers worldwide.

List of Key PCIe SSD for AI Companies Profiled

-

Seagate Technology

-

ADATA Technology

-

Gigabyte Technology

-

Intel Corporation

-

Sabrent

-

Corsair Components

-

Solidigm (formerly Intel NAND Business)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

PCIe 5.0 SSD is rapidly emerging as the leading segment, driven by the exponentially growing bandwidth demands of modern AI and machine learning workloads.

|

| By Application |

|

High Performance Computing (HPC) stands as the dominant application segment, underpinned by the insatiable data processing requirements of AI‑driven scientific research and enterprise analytics.

|

| By End User |

|

Hyperscale Data Centers & Cloud Providers represent the most influential end‑user segment, as these organizations are at the forefront of deploying AI infrastructure at massive scale.

|

| By Form Factor |

|

EDSFF (Enterprise and Datacenter Standard Form Factor) is gaining strong momentum as the preferred form factor for next‑generation AI data‑center deployments.

|

| By Deployment Mode |

|

Cloud‑Based Deployment leads the market as the preferred mode for large‑scale AI model development and training, offering organizations the flexibility to scale storage resources dynamically in alignment with fluctuating AI workload demands.

|

Regional Analysis: PCIe SSD for AI Market

The region benefits from a well‑established supply chain, favorable regulatory frameworks encouraging digital transformation, and strong collaboration between academic institutions and private technology sectors. Canada complements this leadership by positioning itself as an emerging AI hub, with government‑backed programs nurturing next‑generation computing infrastructure. Enterprises across financial services, healthcare, and autonomous systems are increasingly integrating PCIe SSD for AI applications to manage expanding datasets and reduce latency in real‑time decision‑making environments. North America's early adoption advantage, combined with continuous capital deployment toward AI infrastructure upgrades, firmly cements its position as the leading region in the PCIe SSD for AI market landscape through the forecast period extending to 2034.

North America's hyperscale data center footprint is expanding rapidly to accommodate surging AI workloads. Major cloud and technology operators are commissioning next‑generation facilities optimized for PCIe SSD for AI deployments, prioritizing ultra‑low latency storage access. This infrastructure buildout directly accelerates regional demand, as AI training pipelines require sustained high‑bandwidth storage performance that only advanced PCIe SSD architectures can reliably deliver at scale.

Across healthcare, financial services, and autonomous‑vehicle industries, North American enterprises are embedding AI capabilities into core operations. This broad sectoral adoption is fueling procurement of PCIe SSD for AI solutions that can handle complex inference tasks and large‑scale data pipelines. Decision‑makers are prioritizing storage solutions that complement GPU clusters, driving sustained regional investment in high‑performance PCIe SSD technologies.

The United States hosts a highly concentrated semiconductor research ecosystem, with leading fabless designers and storage solution innovators continuously advancing PCIe SSD for AI architectures. Collaborative partnerships between universities, national laboratories, and private technology companies are accelerating next‑generation PCIe SSD development. This innovation pipeline ensures North America remains at the forefront of performance breakthroughs relevant to AI storage infrastructure demands.

Supportive government policies, including strategic federal investment in domestic semiconductor manufacturing and AI research, are reinforcing North America's competitive position in the PCIe SSD for AI market. Favorable regulatory frameworks reduce market entry barriers for innovative storage solution providers, while public‑private partnerships ensure the region maintains a technology leadership posture critical to sustaining AI infrastructure competitiveness well into the 2030s.

Europe

Europe represents a strategically significant and steadily maturing region within the global PCIe SSD for AI market. Nations such as Germany, France, the United Kingdom, and the Netherlands are driving regional momentum through coordinated investment in AI research programs and digital infrastructure modernization initiatives. The European Union's comprehensive AI strategy and data governance frameworks are prompting enterprises and public‑sector organizations to invest in compliant, high‑performance storage solutions. PCIe SSD for AI technologies are increasingly deployed across automotive AI research, industrial automation, and smart manufacturing environments, sectors where Europe holds established global competitiveness. Regional data sovereignty requirements are further encouraging local data‑center operators to upgrade storage infrastructures with advanced PCIe SSD solutions capable of supporting sensitive AI workloads. While Europe's pace of adoption is somewhat moderated by regulatory compliance complexity, the region's long‑term trajectory remains robustly positive as AI integration deepens across critical industries.

Asia‑Pacific

Asia‑Pacific is emerging as one of the fastest‑evolving regions in the global PCIe SSD for AI market, underpinned by aggressive government‑led AI development programs and rapid expansion of digital infrastructure across China, Japan, South Korea, and India. China's national AI strategy has catalyzed enormous investment in indigenous AI computing infrastructure, creating substantial demand for high‑performance PCIe SSD for AI applications within cloud platforms and research institutions. South Korea and Japan contribute through advanced semiconductor manufacturing capabilities and strong enterprise adoption of AI‑powered industrial systems. India is experiencing accelerating momentum as a growing AI services hub, prompting increased procurement of PCIe SSD for AI workloads across cloud and enterprise environments. The region's combination of manufacturing scale, government policy support, and expanding AI application breadth positions Asia‑Pacific as a critical growth engine for the PCIe SSD for AI market through 2034.

South America

South America occupies an emerging position within the global PCIe SSD for AI market, with Brazil serving as the primary growth driver alongside growing interest from Argentina and Chile. The region is in relatively early stages of enterprise AI adoption; however, expanding cloud infrastructure investments and increasing digitalization across financial services, agriculture technology, and telecommunications sectors are gradually stimulating demand for PCIe SSD for AI solutions. Multinational technology companies are extending data‑center footprints into South America to serve growing regional cloud consumption, which indirectly accelerates PCIe SSD for AI procurement. Economic variability and infrastructure development gaps present challenges to uniform regional growth, but the long‑term outlook remains cautiously optimistic as regional governments increasingly recognize AI infrastructure as a strategic national priority and allocate resources accordingly toward advancing digital capabilities.

Middle East & Africa

The Middle East and Africa region represents a nascent but increasingly strategic segment of the global PCIe SSD for AI market. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are spearheading AI‑driven national transformation agendas supported by sovereign wealth fund investments in smart city projects, AI research centers, and next‑generation data‑center facilities. These initiatives are generating early but meaningful demand for high‑performance PCIe SSD for AI infrastructure. South Africa and select East African economies are beginning to experience digital infrastructure expansion driven by mobile connectivity growth and emerging cloud service adoption. While the broader African continent remains in nascent stages relative to global counterparts, targeted investment in technology parks and AI capacity‑building programs signals a constructive long‑term trajectory for PCIe SSD for AI market development across the region through the forecast horizon.

Get Full Report Here:

PCIe SSD for AI Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us