C/C Composite Brake Disc Market to Reach USD 612.3M by 2034 at 8.0% CAGR

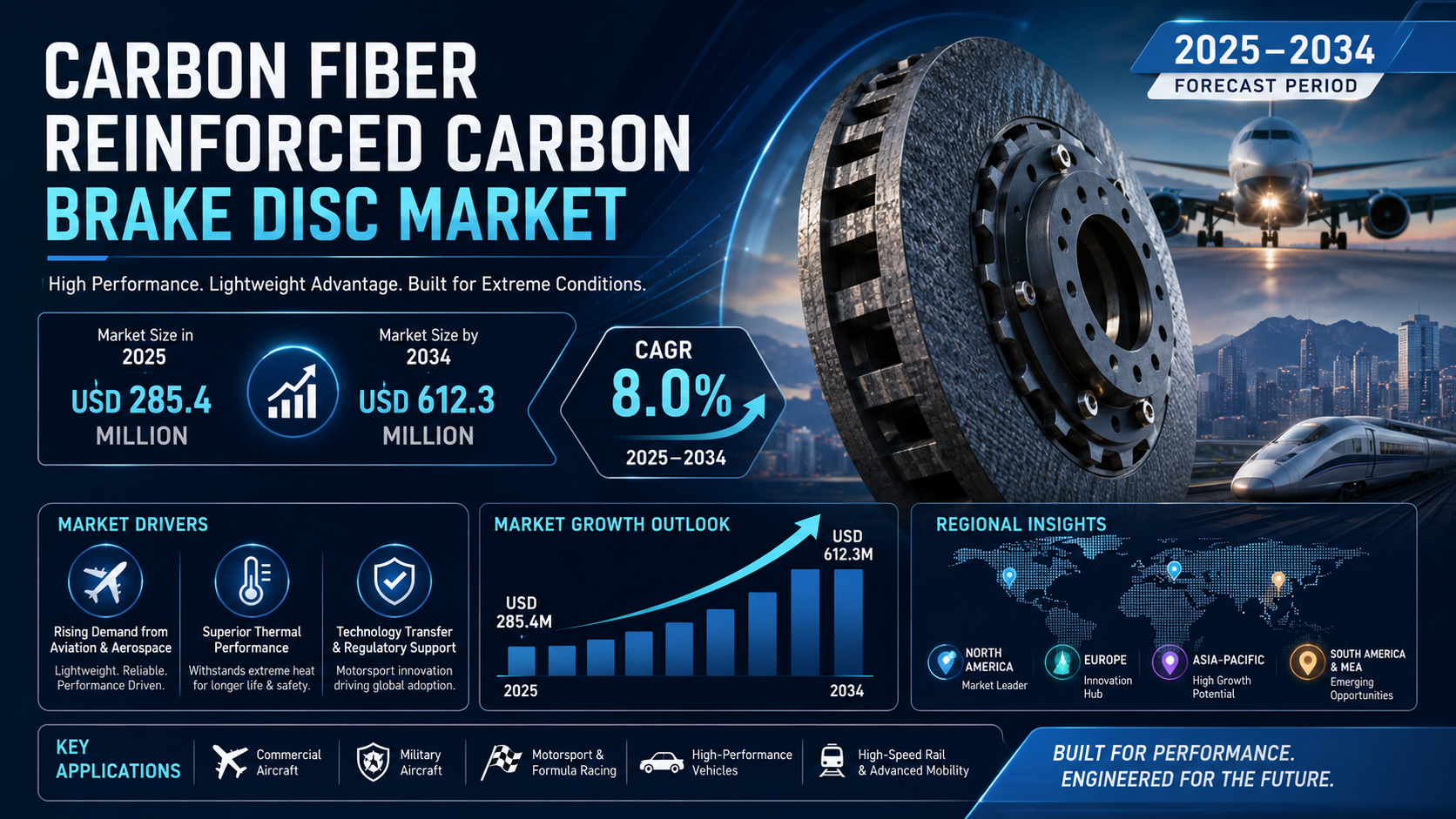

Global Carbon Fiber Reinforced Carbon (C/C Composite) Brake Disc market was valued at USD 285.4 million in 2025 and is projected to reach USD 612.3 million by 2034, exhibiting a remarkable CAGR of 8.0% during the forecast period.

Carbon Fiber Reinforced Carbon (C/C Composite) brake discs represent an advanced class of friction materials consisting of carbon fiber reinforcements embedded within a carbon matrix. These components have transitioned from specialized applications in high-stakes environments to become essential solutions where superior thermal management, lightweight construction, and consistent braking performance are non-negotiable. Their ability to maintain structural integrity at temperatures exceeding 1,000°C distinguishes them from traditional metallic or ceramic alternatives, enabling reliable operation in extreme conditions across demanding sectors.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308677/carbon-fiber-reinforced-carbon-brake-disc-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Rising Demand from Aviation and Aerospace Sector: The aviation industry remains the dominant force behind C/C composite brake disc adoption. Aircraft manufacturers and operators continuously seek weight reduction to enhance fuel efficiency and increase payload capacity. C/C composite brake discs deliver up to 40% weight savings compared to equivalent steel assemblies while providing exceptional performance under repeated high-energy braking cycles typical in commercial and military operations. As global air passenger traffic recovers and fleets expand, particularly across Asia-Pacific, the Middle East, and North America, this driver continues to accelerate market momentum.

- Superior Thermal Performance and Extended Service Life: C/C composite brake discs excel in extreme thermal environments, reliably withstanding temperatures exceeding 2,000°C during intense braking events. Their stable coefficient of friction across wide temperature ranges ensures consistent braking performance and enhanced safety. Furthermore, these discs often provide two to three times longer service life than conventional alternatives, reducing maintenance requirements, lowering lifecycle costs, and minimizing operational downtime for aircraft and high-performance vehicles.

- Technology Transfer from Motorsport and Regulatory Support: Motorsport applications, especially in Formula 1 and endurance racing, have proven the capabilities of C/C composites under the most demanding conditions. This heritage facilitates adoption in high-performance automotive segments. At the same time, stringent aviation safety standards and evolving regulations addressing brake emissions and fuel efficiency reinforce the shift toward lightweight, high-performance materials like C/C composites across aerospace and select automotive platforms.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308677/carbon-fiber-reinforced-carbon-brake-disc-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve broader adoption.

- High Production Costs and Complex Manufacturing: The manufacturing of C/C composite brake discs requires highly specialized, time-intensive processes such as chemical vapor infiltration or liquid phase impregnation followed by pyrolysis. These multi-week or multi-month densification cycles result in substantially higher unit costs compared to conventional brake discs, limiting adoption primarily to performance-critical applications where total cost of ownership justifies the premium.

- Lengthy Certification and Qualification Processes: In aviation, the dominant application segment, new components must undergo exhaustive testing and regulatory certification by authorities such as the FAA and EASA. These processes can extend over several years, creating significant barriers for new entrants and slowing the pace of innovation and market expansion even for established suppliers introducing improved variants.

Critical Market Challenges Requiring Innovation

The transition from laboratory success to industrial-scale manufacturing presents its own set of challenges. The production process demands precise control to achieve consistent material properties, with complex densification steps that are sensitive to variations in raw materials and process conditions. This creates high barriers to entry and limits supply chain scalability. Furthermore, the concentrated nature of specialized manufacturing expertise and capital equipment requirements results in a limited supplier base, introducing potential vulnerabilities in meeting sudden demand increases from major aerospace programs.

Additionally, the market contends with raw material supply dynamics. High-quality carbon fiber feedstock faces competing demand from other advanced composite applications, contributing to price volatility and capacity planning difficulties. Performance characteristics such as reduced friction effectiveness at low temperatures also require careful operational procedures in certain environments, adding layers of complexity for end-users.

Vast Market Opportunities on the Horizon

- Emerging Electric and Hybrid Aircraft Platforms: The development of electric vertical takeoff and landing vehicles, eVTOLs, and hybrid-electric regional aircraft creates strong demand for lightweight braking solutions. Weight savings directly translate to improved range and payload in battery-constrained electric platforms, positioning C/C composite brake discs as an enabling technology for this rapidly advancing sector.

- High-Speed Rail and Defense Expansion: Global investments in high-speed rail networks across Asia and Europe offer significant potential for C/C composites in managing braking energy at speeds exceeding 300 km/h. Similarly, ongoing modernization of military aircraft fleets and interest in advanced defense platforms continue to drive steady, high-value demand for proven C/C braking technologies.

- Process Innovations and Strategic Partnerships: Advances in manufacturing techniques aimed at reducing densification times and costs are opening pathways to greater market accessibility. Increasing collaboration between material specialists, aircraft manufacturers, and tier-one suppliers helps bridge technical gaps and accelerate qualification of next-generation solutions, shortening commercialization timelines.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Chemical Vapor Infiltration (CVI) C/C Composite Brake Disc, Liquid Phase Impregnation (LPI) C/C Composite Brake Disc, and Hybrid Process variants. Chemical Vapor Infiltration (CVI) C/C Composite Brake Disc currently leads the market, favored for its superior microstructural uniformity, outstanding oxidation resistance, and proven track record in the most demanding aerospace and motorsport applications. LPI variants appeal to manufacturers seeking improved production efficiency while hybrid approaches combine advantages of both processes for balanced performance and scalability.

By Application:

Application segments include Commercial Aircraft, Military Aircraft, Formula Racing & Motorsport, High-Performance Passenger Vehicles, and others. The Commercial Aircraft segment currently dominates, driven by the need for reliable, lightweight braking systems that enhance safety and operational efficiency across expanding global airline fleets. Motorsport and military applications also represent critical high-performance segments, while high-performance automotive adoption continues to grow steadily.

By End-User Industry:

The end-user landscape includes Original Equipment Manufacturers (OEMs), Aftermarket Service Providers, and Defense & Government Agencies. The OEM segment accounts for the major share, as major aircraft and high-performance vehicle manufacturers integrate C/C composite brake discs directly into new platforms to meet stringent performance and certification requirements from the design stage. Aftermarket and defense sectors provide additional stable demand streams through replacement and specialized procurement programs.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308677/carbon-fiber-reinforced-carbon-brake-disc-market

Competitive Landscape:

The global Carbon Fiber Reinforced Carbon (C/C Composite) Brake Disc market is highly specialized and characterized by intense competition and technological innovation. The top three companies—Safran Landing Systems (France), Honeywell Aerospace (United States), and Brembo S.p.A. (Italy)—collectively command a significant portion of the market share. Their dominance stems from deep aerospace expertise, extensive certification portfolios, advanced manufacturing capabilities, and long-standing relationships with major OEMs and operators worldwide.

List of Key Carbon Fiber Reinforced Carbon (C/C Composite) Brake Disc Companies Profiled:

● Safran Landing Systems (France)

● Honeywell Aerospace (United States)

● Brembo S.p.A. (Italy)

● SGL Carbon SE (Germany)

● Mersen (France)

● Surface Transforms plc (United Kingdom)

● Toyo Tanso Co., Ltd. (Japan)

● Graphtek LLC (United States)

● Fiber Materials Inc. (United States)

The competitive strategy is overwhelmingly focused on R&D to enhance material properties and reduce production costs, alongside forming strategic partnerships with end-user companies to co-develop and validate application-specific solutions, thereby securing long-term demand and accelerating qualification processes.

Regional Analysis: A Global Footprint with Distinct Leaders

● North America: Holds a leading position in the global market. This strength is supported by a robust aerospace industry, significant defense spending, and strong demand from commercial aviation and high-performance sectors. The United States serves as the primary growth engine through major aircraft manufacturers and extensive MRO networks.

● Europe: Forms a powerful hub for both innovation and consumption. The region benefits from leading aircraft programs, a rich motorsport heritage, and advanced manufacturing capabilities in countries such as France, Germany, the United Kingdom, and Italy. Strong regulatory frameworks and collaborative R&D initiatives further support market leadership.

● Asia-Pacific, South America, and MEA: These regions represent emerging frontiers with substantial long-term potential. Rapid fleet expansion in commercial aviation, defense modernization programs, and growing high-speed rail investments drive increasing adoption. While currently smaller in scale relative to mature markets, rising industrialization and infrastructure development create meaningful growth opportunities.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308677/carbon-fiber-reinforced-carbon-brake-disc-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308677/carbon-fiber-reinforced-carbon-brake-disc-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/