Business Loan Rejection Without Collateral: Complete Guide for Indian Businesses

In today’s competitive market, businesses often require quick financial support to manage operations, expand services, purchase inventory, or stabilize cash flow. Many entrepreneurs prefer unsecured funding because they do not want to risk valuable assets. However, Business Loan Rejection Without Collateral has become a common challenge for startups, MSMEs, traders, and even established companies in India.

Banks and NBFCs carefully evaluate repayment capacity before approving collateral-free funding. Since there is no asset security involved, lenders consider unsecured lending riskier. As a result, many applications are rejected due to poor financial documentation, low credit scores, unstable cash flow, or inadequate business history.

Understanding the reasons behind loan rejection can help businesses prepare stronger applications and improve approval chances. This guide explains the major causes of unsecured business loan rejection, practical solutions, eligibility improvement strategies, and expert tips to secure funding successfully in 2026.

What Is a Collateral-Free Business Loan?

A collateral-free business loan is a type of unsecured financing where businesses can borrow funds without pledging property, machinery, inventory, or other assets as security.

These loans are commonly used for:

- Working capital requirements

- Business expansion

- Inventory purchases

- Marketing and advertising

- Machinery upgrades

- Staff salaries

- Debt consolidation

- Emergency business expenses

Most unsecured loans are approved based on:

- Creditworthiness

- Business turnover

- Banking history

- Profitability

- GST returns

- Income tax filings

- Cash flow stability

Although collateral-free loans offer convenience and faster processing, lenders follow stricter eligibility checks, increasing the possibility of rejection.

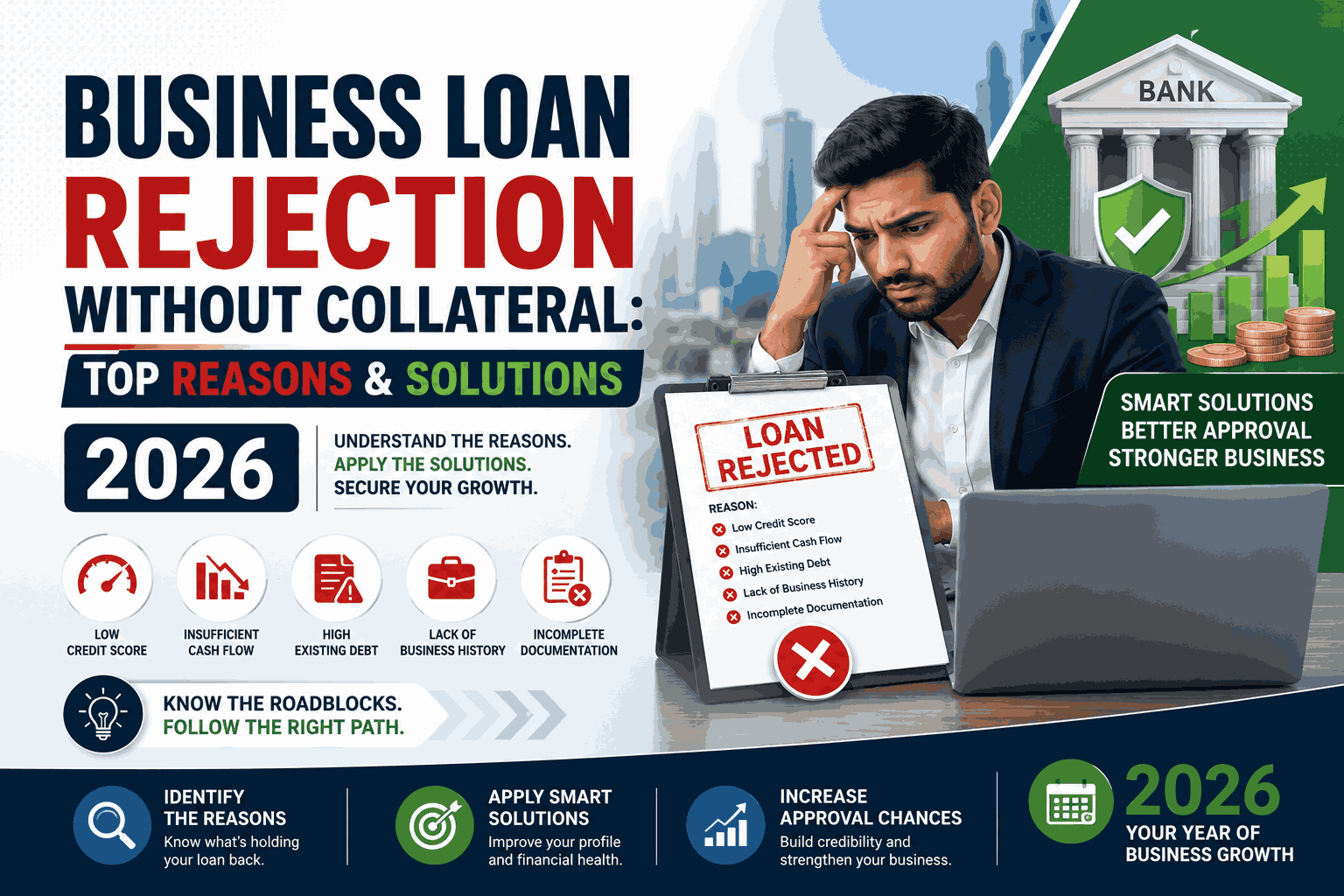

Why Does Business Loan Rejection Without Collateral Happen?

There are several reasons why lenders reject unsecured business financing applications. Understanding these issues is the first step toward improving approval chances.

1. Low Credit Score

A poor CIBIL score is one of the biggest reasons for loan rejection. Most lenders prefer a business owner’s credit score above 700 for unsecured funding.

Low scores usually indicate:

- Delayed EMI payments

- Credit card defaults

- Loan settlements

- Excessive borrowing

- High credit utilization

Since no collateral is available, lenders rely heavily on credit behavior to assess repayment capability.

Solution

- Clear outstanding dues

- Avoid EMI delays

- Reduce credit utilization ratio

- Monitor credit reports regularly

- Correct credit report errors immediately

Improving your credit profile significantly increases loan eligibility.

2. Inconsistent Cash Flow

Lenders evaluate whether the business generates enough revenue to repay the loan comfortably. Businesses with unstable income patterns often face rejection.

Common red flags include:

- Frequent negative bank balances

- Declining revenue trends

- Irregular customer payments

- Seasonal income instability

- Low profit margins

Solution

Maintain healthy banking transactions and improve financial management. Businesses should demonstrate stable monthly income and proper working capital planning before applying.

3. Insufficient Business Vintage

New businesses often struggle to obtain unsecured financing because lenders prefer operational stability.

Many financial institutions require:

- Minimum 1–3 years of business operations

- Consistent turnover history

- GST compliance

- Tax filing records

Startups without adequate operational history are considered high-risk borrowers.

Solution

If the business is new:

- Start with smaller funding products

- Build banking relationships

- Maintain GST compliance

- Use secured credit products initially

- Improve financial records over time

Alternative financing options like invoice financing or private funding may also help early-stage businesses.

4. Poor Financial Documentation

Incomplete or inaccurate documentation frequently causes Business Loan Rejection Without Collateral.

Typical missing documents include:

- GST returns

- Income tax returns

- Bank statements

- Balance sheets

- Profit & loss statements

- Business registration proof

Lenders require complete financial transparency before approving unsecured loans.

Solution

Prepare organized financial records before applying. Businesses should ensure:

- Updated bookkeeping

- Accurate tax filings

- Proper audit reports

- Consistent bank transactions

Well-maintained documentation creates lender confidence.

5. High Existing Debt Obligations

If the business already has multiple loans or high EMI burdens, lenders may reject new applications due to increased repayment risk.

High debt-to-income ratios indicate overleveraging.

Solution

- Repay smaller existing debts first

- Consolidate liabilities where possible

- Avoid multiple simultaneous loan applications

- Improve debt servicing capability

Reducing financial burden improves borrowing capacity.

6. Frequent Loan Applications

Submitting loan applications to multiple lenders within a short period negatively impacts credit profiles.

Every lender inquiry gets recorded in credit reports, which may signal financial distress.

Solution

Research eligibility carefully before applying. Apply only with lenders whose criteria match your business profile.

7. Unstable Industry or Business Category

Certain industries are considered high-risk due to market volatility.

Examples may include:

- Speculative trading

- Seasonal businesses

- Businesses with irregular income cycles

- Highly affected sectors during economic downturns

Lenders may hesitate to provide unsecured financing in such cases.

Solution

Businesses should showcase:

- Stable contracts

- Consistent revenue

- Diversified customer base

- Strong financial projections

Risk mitigation improves lender confidence.

How to Improve Approval Chances for Collateral-Free Business Loans

Businesses can take proactive measures to improve loan approval possibilities.

Maintain Strong Financial Discipline

Financial discipline remains the most important factor in unsecured lending.

Key practices include:

- Timely EMI payments

- Proper bookkeeping

- GST compliance

- Tax return filing

- Healthy bank balance maintenance

Strong financial management builds credibility.

Improve Business Banking Profile

Lenders analyze banking behavior carefully.

To strengthen your profile:

- Maintain regular transactions

- Avoid cheque bounces

- Ensure stable average monthly balance

- Deposit business revenues consistently

Healthy banking activity increases trust.

Build a Positive Credit History

A strong repayment track record significantly improves unsecured funding eligibility.

Helpful steps include:

- Using business credit responsibly

- Paying credit card dues on time

- Avoiding settlements and defaults

- Monitoring CIBIL reports regularly

Apply for the Right Loan Amount

Applying for excessively high loan amounts often results in rejection.

Businesses should apply based on:

- Actual turnover

- Repayment capacity

- Business profitability

- Existing liabilities

Realistic loan requests improve approval chances.

Prepare a Strong Business Plan

Lenders may ask for business expansion plans, especially for higher-value unsecured loans.

A good business plan should include:

- Revenue projections

- Growth strategy

- Market analysis

- Expense planning

- Repayment strategy

This demonstrates business seriousness and repayment capability.

Alternative Funding Solutions After Loan Rejection

If traditional lenders reject your application, several alternative financing options are available.

NBFC Financing

NBFCs often have flexible eligibility compared to banks. They may consider alternative income assessments and business potential.

Invoice Financing

Businesses with unpaid invoices can obtain short-term funding against receivables.

This is useful for:

- Manufacturing businesses

- Traders

- Service providers

- B2B companies

Merchant Cash Advances

Businesses with digital payment inflows can obtain funding based on future sales projections.

Equipment Financing

Machinery or equipment purchases can sometimes be financed separately with partial asset backing.

Working Capital Partnerships

Some funding institutions offer customized structured financing solutions for businesses with temporary financial challenges.

Government Schemes Supporting MSMEs

The Indian government supports MSMEs through several financing schemes.

Popular programs include:

CGTMSE Scheme

The Credit Guarantee Fund Trust for Micro and Small Enterprises helps businesses obtain collateral-free loans with government-backed guarantees.

Mudra Loans

Pradhan Mantri Mudra Yojana supports small businesses and startups with collateral-free funding options.

Stand-Up India Scheme

This scheme encourages entrepreneurship among women and SC/ST business owners.

Government-backed schemes may improve funding accessibility for eligible businesses.

Common Mistakes Businesses Must Avoid

To reduce the risk of Business Loan Rejection Without Collateral, businesses should avoid these common errors:

- Submitting incomplete documents

- Hiding financial liabilities

- Applying for unrealistic loan amounts

- Ignoring tax compliance

- Maintaining irregular bank transactions

- Defaulting on existing obligations

- Applying with poor credit scores

- Using multiple lenders simultaneously

Careful preparation can prevent rejection.

Importance of Professional Financial Guidance

Many businesses fail to structure their loan applications properly. Professional financial consultants can help improve approval possibilities through:

- Financial profile analysis

- Loan eligibility assessment

- Debt restructuring

- Credit improvement planning

- Documentation preparation

- Lender selection guidance

Expert assistance often reduces rejection risk significantly.

Future of Unsecured Business Financing in India

The Indian lending ecosystem is rapidly evolving due to digital banking, fintech innovations, and alternative credit assessment models.

In 2026, lenders increasingly evaluate:

- GST data

- Digital transactions

- Cash flow analytics

- AI-driven risk assessments

- Real-time banking behavior

Businesses with strong digital financial records are likely to receive faster approvals.

Fintech lenders are also expanding access to unsecured working capital solutions for MSMEs and startups.

Final Thoughts

Facing Business Loan Rejection Without Collateral can be frustrating, but rejection does not mean financing opportunities are over. Most rejections occur due to solvable issues such as poor documentation, weak credit profiles, unstable cash flow, or excessive liabilities.

Businesses that maintain financial discipline, improve banking behavior, strengthen credit history, and prepare organized documentation can significantly improve their approval chances.

Before applying for unsecured funding, companies should evaluate their financial readiness, choose suitable lenders, and seek professional guidance if necessary. With proper planning and financial management, businesses can successfully secure the funding needed for growth and operational stability in 2026.

For businesses looking to overcome financing challenges, structured funding solutions and strategic financial planning remain key to long-term success.