GaN Fast Charger (Consumer) Market, Trends, Business Strategies 2026-2034

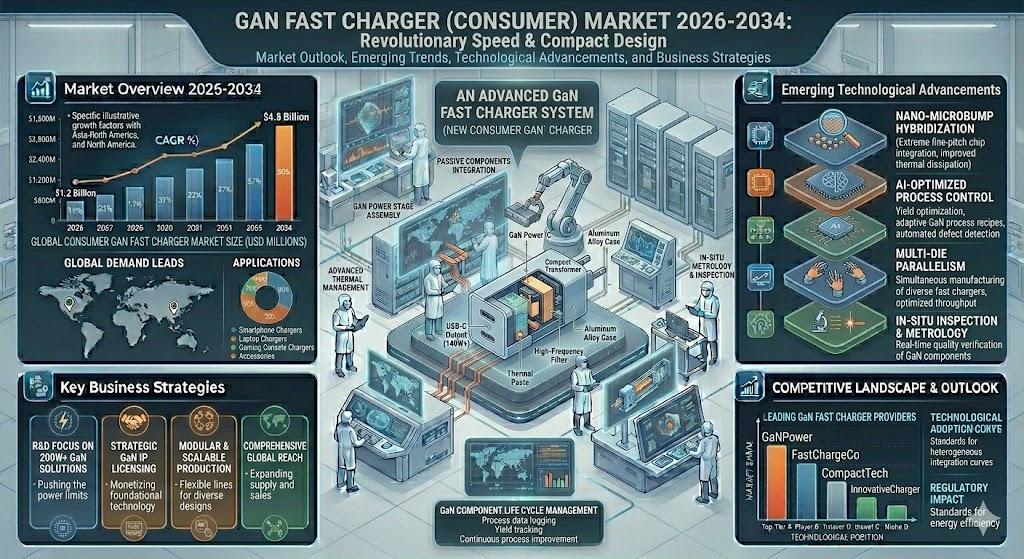

The global GaN Fast Charger (Consumer) Market is witnessing rapid adoption driven by the convergence of high‑performance power delivery and ultra‑compact form‑factors, with analysts forecasting a compound annual growth rate (CAGR) of 8.2% through 2034.

Gallium‑Nitride (GaN) technology enables chargers that are up to 70% smaller, up to 50% more efficient, and capable of delivering power levels that traditional silicon‑based chargers cannot match. For end‑users, this translates into lighter travel companions, reduced heat generation, and faster charging cycles for smartphones, laptops, wearables, and emerging categories such as AR/VR head‑sets. Manufacturers are leveraging these advantages to differentiate product portfolios, while retailers promote the eco‑friendly narrative of lower energy consumption.

Download FREE Sample Report:

GaN Fast Charger (Consumer) Market - View in Detailed Research Report

Market Drivers and Growth Catalysts

Escalating Consumer Expectation for Speed and Portability

The proliferation of high‑capacity batteries in flagship smartphones and ultraportable laptops has intensified demand for chargers that can replenish 50% of capacity within 15‑30 minutes. Consumers are increasingly unwilling to tolerate long charging times, especially in a mobile‑first world where work, entertainment, and connectivity converge on a single handheld device. GaN chargers, with their ability to push 65 W–100 W over a USB‑PD interface while remaining pocket‑size, directly satisfy this demand, prompting rapid market uptake across both premium and mainstream segments.

Regulatory Push Toward Energy Efficiency

Governments in the European Union, United States, and several Asia‑Pacific economies have introduced stricter efficiency standards for power adapters, aiming to cut global electricity consumption and reduce electronic waste. These regulations favor GaN‑based solutions because of their superior conversion efficiency, often exceeding 95% compared with 80%‑85% for conventional silicon chargers. As compliance deadlines approach, OEMs are accelerating the integration of GaN modules into their product lines, creating a trickle‑down effect that expands the consumer charger market.

Rise of Multi‑Device Ecosystems

Modern households and workplaces now contain an ecosystem of devices-smartphones, tablets, laptops, wireless earbuds, smartwatches, gaming controllers, and even portable projectors. Users prefer a single charger that can safely and simultaneously power multiple gadgets. Multi‑port GaN chargers, which combine several USB‑PD outputs with intelligent power distribution algorithms, are gaining traction because they reduce cable clutter and improve user convenience without compromising speed.

Technology Trends Shaping the Landscape

Beyond raw power output, manufacturers are embedding advanced thermal‑management sensors, AI‑driven power‑allocation software, and robust safety protocols (over‑voltage, over‑current, temperature protection) into GaN chargers. The convergence of GaN with USB‑PD 3.1, which supports up to 240 W, is already being explored for high‑performance laptops and mini‑desktop PCs. Additionally, the emergence of wireless GaN chargers-where the high efficiency of GaN helps mitigate the typical losses associated with inductive charging-suggests a future where cord‑free fast charging becomes mainstream.

Supply‑chain innovations are also critical. The maturation of GaN substrate manufacturing, driven by investments from semiconductor foundries in Taiwan, South Korea, and the United States, is lowering unit costs and improving yield. This trend enables mid‑tier brands to offer GaN chargers at price points previously reserved for silicon‑based alternatives, intensifying competition and expanding market reach.

Emerging Opportunities in Adjacent Segments

Gaming, AR/VR, and High‑Performance Computing

The surge in portable gaming laptops, cloud‑gaming handhelds, and immersive AR/VR headsets demands power solutions that can sustain high‑draw devices for extended sessions. GaN chargers, with their high power density and low thermal footprint, are uniquely positioned to become the standard accessory for these emerging product categories.

Electric Vehicle (EV) Owner Accessories

While EVs rely on high‑voltage DC fast‑charging infrastructure, the ancillary market for personal devices inside vehicles-infotainment systems, smartphones, and portable workstations-is expanding. Automotive OEMs are beginning to certify GaN chargers for in‑car use, leveraging the technology’s ability to operate efficiently across a wide temperature range and its compact size, which suits limited dashboard space.

Sustainability and Circular Economy Initiatives

Corporate sustainability programs increasingly scrutinize the lifecycle impact of peripheral accessories. GaN chargers, by virtue of higher efficiency and longer operational life, support corporate ESG goals. Some manufacturers are adopting modular designs that allow end‑of‑life recycling of the GaN die and driver circuitry, aligning product strategy with circular‑economy principles.

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

GaN Fast Charger Market Dynamics and Leading Competitors Overview

The consumer GaN fast charger market features a competitive and evolving landscape dominated by technologically advanced companies emphasizing innovation in power delivery and compact design. Leading players like Anker Innovations and Belkin International have leveraged extensive research and development to yield efficient, lightweight chargers that align with growing consumer demand for rapid and reliable charging solutions. These companies benefit from established distribution channels and strong brand presence, which underpin their market share in an industry experiencing an anticipated CAGR of 8.2% through 2034.

In addition to dominant players, several niche manufacturers such as GaNPro Technology and Aukey Innovations are carving out significant market segments by focusing on specialized device compatibility and cost‑competitive models. Other notable contributors include RAVPower, Hyper, Baseus, and Zendure, who collectively drive the diversification of GaN charger offerings. Strategic partnerships and continuous innovation in thermal management and power efficiency are critical competitive factors enabling these players to maintain relevancy within this rapidly expanding market.

List of Key GaN Fast Charger Companies Profiled

-

Anker Innovations

-

Aukey Innovations

-

GaNPro Technology

-

Baseus

-

Zendure

-

CHOETECH

-

Nekteck

-

Satechi

-

AUKEY

Segment Analysis

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi-Port Chargers are increasingly preferred due to their ability to simultaneously charge multiple devices, aligning with the growing consumer demand for versatile charging solutions. These chargers emphasize rapid power delivery and ease of use, while compact chargers appeal due to portability and form factor innovations enabled by GaN technology. Across both types, improvement in thermal management and efficiency remains a key focus, offering enhanced user experience through faster charging times and reduced device overheating. |

| By Application |

|

Smartphones remain the primary application driving market demand, fueled by user expectations for faster, more reliable charging and increased device usage. Laptops & Tablets benefit significantly from GaN fast chargers due to their higher power requirements and increased mobility trends. Wearable devices, while smaller in power needs, increasingly adopt GaN chargers for their efficiency and compactness, illustrating the technology's adaptability across diverse consumer electronics. |

| By End User |

|

Individual Consumers dominate the market, driven by rising usage of portable electronic devices and an increasing awareness of the benefits offered by GaN technology such as compactness and efficiency. Commercial establishments are also progressively adopting GaN chargers to enhance customer experience and support workplace device ecosystems. OEMs & Distributors focus on incorporating GaN technology into products to stay competitive, emphasizing quality improvement and cost reduction in manufacturing processes. |

| By Charging Interface |

|

USB Power Delivery (USB PD) is the leading charging interface segment as it supports rapid charging and universal compatibility across multiple device types. The adoption of USB PD is critical for consumer convenience and interoperability, fueling demand for GaN fast chargers. Proprietary charging interfaces offer optimized performance for specific device brands, catering to brand‑loyal user bases. Wireless charging, while still evolving, integrates with GaN technology to promise enhanced efficiency and convenience in charging workflows. |

| By Product Portability |

|

Travel Chargers benefit greatly from GaN's compact and lightweight design, meeting consumer needs for mobility and convenience during travel. Desktop chargers remain relevant for users prioritizing stable power sources at home or office, often integrating multiple ports for diverse device support. Car chargers represent a growth frontier as reliance on mobile devices in vehicles increases, with GaN fast chargers enabling quicker charging without compromising space or heat dissipation. |

Regional Analysis: Global GaN Fast Charger (Consumer) Market

Regional Analysis: Global GaN Fast Charger (Consumer) Market

Asia‑Pacific’s well‑established electronics manufacturing infrastructure supports the rapid production and deployment of GaN Fast Chargers (Consumer), reducing lead times and fostering the availability of cost‑effective solutions without compromising quality. This environment enables quick adaptation to changing consumer preferences.

The region emphasizes research and development in GaN technology, improving charger efficiency, thermal management, and shrinking device footprints, contributing to its position as a front‑runner in introducing advanced charging technologies to consumers.

Rapid adoption is seen across urban areas due to consumers’ growing preference for fast, portable charging devices integrated with multiple protections against overheating and overcurrent, enhancing user safety and convenience.

Collaborations between startups, tech giants, and material suppliers in Asia‑Pacific accelerate innovation cycles and facilitate cost reduction, enabling the introduction of competitive GaN chargers worldwide while meeting environmental and efficiency standards.

North America

North America remains a crucial market for GaN Fast Charger (Consumer) technology, driven by early adoption and significant consumer awareness about energy efficiency and compact design. The presence of key technology companies fosters continuous innovation, and consumers exhibit strong preferences for chargers compatible with multiple device types. Market strategies focus on premium product segments, with a growing trend toward wireless and multi‑port GaN chargers.

Europe

Europe’s GaN Fast Charger (Consumer) Market is shaped by stringent energy efficiency regulations and environmental policies, driving manufacturers to prioritize sustainable technologies. Consumers are increasingly inclined toward chargers that combine fast charging features with eco‑friendly materials. Regional focus on interoperability and safety standards further fosters trust and widespread acceptance of GaN technology in consumer electronics.

South America

South America presents emerging opportunities for GaN Fast Charger (Consumer) deployment, marked by increasing smartphone usage and slow but steady infrastructure improvements. The market growth hinges on affordability, with consumer demand centered on efficient yet cost‑effective chargers. International brands are exploring strategic partnerships to penetrate local markets and tailor products that address regional power supply inconsistencies.

Middle East & Africa

In the Middle East & Africa region, the GaN Fast Charger (Consumer) Market growth is supported by heightened mobile device penetration and the region’s focus on modernizing its technological landscape. Consumers increasingly seek high‑performance charging solutions compatible with their portable devices. However, market expansion faces challenges linked to infrastructure gaps and price sensitivity, prompting a focus on durable, reliable GaN fast chargers that balance cost and performance.

Future Outlook (2026‑2034)

Looking ahead, the convergence of GaN with emerging wide‑bandgap materials such as Silicon‑Carbide (SiC) may unlock chargers capable of delivering even higher power levels while maintaining the ultra‑compact footprint that defines the category today. Analysts anticipate that as device manufacturers standardize on higher power envelopes (120 W‑240 W), the ecosystem of accessories will evolve to include docking stations and power‑banks built on GaN platforms, further blurring the line between traditional chargers and full‑featured power hubs.

Investment activity is expected to intensify, with venture capital funds earmarking capital for start‑ups that can deliver breakthrough GaN substrates at lower cost. Concurrently, major semiconductor fabs are expanding capacity to meet the anticipated surge in demand for GaN devices across automotive, data‑center, and consumer domains. This dual‑track investment pipeline will likely drive price compression, making GaN chargers accessible to price‑sensitive segments while preserving premium margins for differentiated features such as AI‑driven power optimization.

Regulatory bodies are also poised to introduce tighter efficiency thresholds for standby power consumption, a move that will further cement GaN’s competitive advantage over legacy silicon adapters. Brands that proactively align product roadmaps with these upcoming standards are expected to capture a larger share of the market and benefit from early‑adopter goodwill.

Analyst Commentary

“The rapid migration from silicon to GaN in the consumer charger space is one of the clearest examples of a technology leap that simultaneously addresses user experience, sustainability, and supply‑chain efficiency,” says Dr. Maya Patel, Senior Analyst at Semiconductor Insight. “Companies that invest in integrated thermal‑management solutions and robust firmware that can intelligently balance power across multiple devices will dominate the next wave of growth, especially as the ecosystem expands into automotive and IoT edge devices.”

“We also foresee a strategic inflection point around 2029 where the majority of flagship smartphones and laptops will natively support 100 W+ USB‑PD via GaN‑based accessories, making the distinction between ‘fast charger’ and ‘power hub’ increasingly blurry,” adds Thomas Liu, Market Research Lead, Semiconductor Insight.

Access the Full Report

Get Full Report Here:

GaN Fast Charger (Consumer) Market, Trends, Business Strategies 2026‑2034 - View in Detailed Research Report

About Semiconductorinsight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us